Kalman Filtering Tutorial

Kalman Filtering Tutorial

Kalman Filtering Tutorial

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

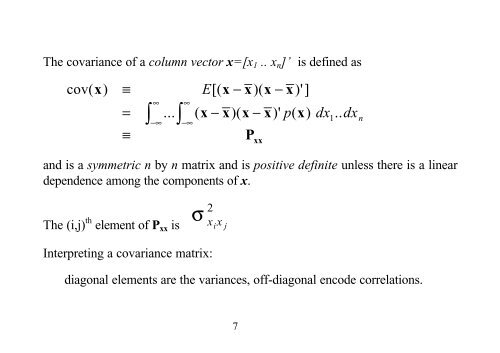

The covariance of a column vector x=[x1 .. xn]’ is defined as<br />

cov( x) ≡ E[(<br />

x − x)( x − x)']<br />

∞<br />

∞<br />

= ∫ ... ∫ ( x − x)( x − x)' p( x)<br />

dx1.. dxn −∞ −∞<br />

≡<br />

7<br />

P xx<br />

and is a symmetric n by n matrix and is positive definite unless there is a linear<br />

dependence among the components of x.<br />

The (i,j) th element of Pxx is σ 2<br />

xi x j<br />

Interpreting a covariance matrix:<br />

diagonal elements are the variances, off-diagonal encode correlations.