Time Series - Data and Statistical Services - Princeton University

Time Series - Data and Statistical Services - Princeton University

Time Series - Data and Statistical Services - Princeton University

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

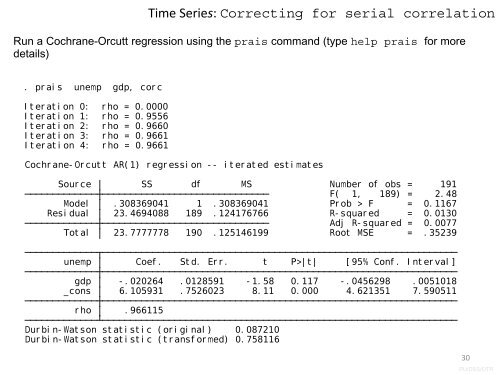

Run a Cochrane-Orcutt regression using the prais comm<strong>and</strong> (type help prais for more<br />

details)<br />

. prais unemp gdp, corc<br />

Iteration 0: rho = 0.0000<br />

Iteration 1: rho = 0.9556<br />

Iteration 2: rho = 0.9660<br />

Iteration 3: rho = 0.9661<br />

Iteration 4: rho = 0.9661<br />

<strong>Time</strong> <strong>Series</strong>: Correcting for serial correlation<br />

Cochrane-Orcutt AR(1) regression -- iterated estimates<br />

Source SS df MS Number of obs = 191<br />

F( 1, 189) = 2.48<br />

Model .308369041 1 .308369041 Prob > F = 0.1167<br />

Residual 23.4694088 189 .124176766 R-squared = 0.0130<br />

Adj R-squared = 0.0077<br />

Total 23.7777778 190 .125146199 Root MSE = .35239<br />

unemp Coef. Std. Err. t P>|t| [95% Conf. Interval]<br />

gdp -.020264 .0128591 -1.58 0.117 -.0456298 .0051018<br />

_cons 6.105931 .7526023 8.11 0.000 4.621351 7.590511<br />

rho .966115<br />

Durbin-Watson statistic (original) 0.087210<br />

Durbin-Watson statistic (transformed) 0.758116<br />

30<br />

PU/DSS/OTR