2 Financial Markets and Transformation Functions

2 Financial Markets and Transformation Functions

2 Financial Markets and Transformation Functions

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Prof. Dr. Hans-Peter Burghof, University of Hohenheim, Bank Management<br />

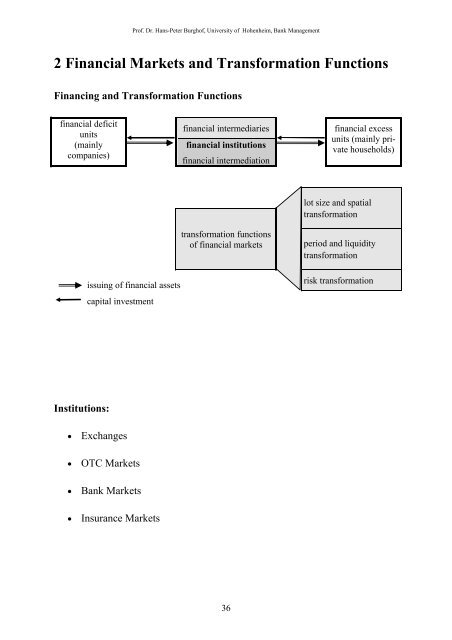

2 <strong>Financial</strong> <strong>Markets</strong> <strong>and</strong> <strong>Transformation</strong> <strong>Functions</strong><br />

Financing <strong>and</strong> <strong>Transformation</strong> <strong>Functions</strong><br />

financial deficit<br />

units<br />

(mainly<br />

companies)<br />

Institutions:<br />

issuing of financial assets<br />

capital investment<br />

Exchanges<br />

OTC <strong>Markets</strong><br />

Bank <strong>Markets</strong><br />

Insurance <strong>Markets</strong><br />

financial intermediaries<br />

financial institutions<br />

financial intermediation<br />

transformation functions<br />

of financial markets<br />

36<br />

financial excess<br />

units (mainly private<br />

households)<br />

lot size <strong>and</strong> spatial<br />

transformation<br />

period <strong>and</strong> liquidity<br />

transformation<br />

risk transformation

Prof. Dr. Hans-Peter Burghof, University of Hohenheim, Bank Management<br />

a) Lot Size <strong>and</strong> Spatial <strong>Transformation</strong><br />

Spatial transformation:<br />

- Solvency at different places (monetary transactions, loans)<br />

- Capital transfers between regions financial balancing<br />

Effects of the failure of a banking system?<br />

Lot size transformation:<br />

- Matching investments of a different size<br />

- Pooling small deposits<br />

- Splitting large deposits<br />

37

Prof. Dr. Hans-Peter Burghof, University of Hohenheim, Bank Management<br />

b) Period <strong>and</strong> Liquidity <strong>Transformation</strong><br />

- Financing long-term investments with short-term funds (positive period<br />

transformation) <strong>and</strong> vice versa (negative period transformation)<br />

- Option to withdraw financial resources out of long-term projects prior to<br />

maturity<br />

Enabled by:<br />

Secondary markets<br />

Price <strong>and</strong> liquidity risks<br />

Possibility of hedging with particular financial products<br />

Intermediation<br />

Counter party risk for the investor<br />

Limited default risk of the financial intermediary by setting financing<br />

rules<br />

38

Prof. Dr. Hans-Peter Burghof, University of Hohenheim, Bank Management<br />

<strong>Financial</strong> Rules to Limit the Risks that Arise from Period <strong>and</strong> Liquidity Trans-<br />

formation<br />

Golden Banking Rule/Golden Rule of Finance:<br />

Total maturity matching<br />

Golden Rule of Balance Sheet<br />

Basis: “Schichtenbilanz”<br />

assets liabilities<br />

A1: Assets with a capital commitment of over<br />

4 years<br />

A2: Assets with a capital commitment of 3<br />

months to 4 years<br />

A3: Assets with a capital commitment up to 3<br />

months<br />

A1 ≤ F1 <strong>and</strong> A1+A2 ≤ F1+F2<br />

“Bodensatzregel” (Principles II <strong>and</strong> III of BAKred)<br />

Rule 1: A1 ≤ F1 + 0,6 F2 + 0,1 F3<br />

39<br />

F1: <strong>Financial</strong> resources invested longer than 4<br />

years<br />

F2: : <strong>Financial</strong> resources invested 3 months to<br />

4 years<br />

F3: : <strong>Financial</strong> resources invested less than 3<br />

months<br />

Rule 2: A2 ≤ (F1 + 0,6 F2 + 0,1 F3 - A1) + 0,4 F2 + 0,2 F3

c) Risk <strong>Transformation</strong><br />

Via secondary markets:<br />

Prof. Dr. Hans-Peter Burghof, University of Hohenheim, Bank Management<br />

Portfolio diversification: (stock) exchange or funds<br />

Limiting risk by using financial derivates<br />

Via financial intermediaries:<br />

Portfolio diversification <strong>and</strong> available net equity of a bank or insurance<br />

company<br />

Banks as “delegated monitor“ <strong>and</strong> “delegated contractor“<br />

Implementation by banks: Risk management<br />

40

Model Calculation<br />

Arrow-Debreu-Model:<br />

Prof. Dr. Hans-Peter Burghof, University of Hohenheim, Bank Management<br />

- 4 states with identical probability<br />

- 2 financial assets (A1 <strong>and</strong> A2)<br />

- Utility functions U or V<br />

- Amount of investment: 100<br />

state: s1 s2 s3 s4<br />

A1 x11 = 130 x12 = 130 x13 = 90 x14 = 90<br />

A2 x21 = 160 x22 = 60 x21 = 160 x22 = 60<br />

U <br />

x<br />

U(Al) 11,40 11,40 9,49 9,49<br />

U(A2) 12,65 7,75 12,65 7,75<br />

E(U(A1)) = 10,44 E(U(A2)) = 10,20<br />

<br />

V <br />

<br />

x<br />

x 5<br />

x 100<br />

otherwise<br />

V(A1) 11,40 11,40 4,49 4,49<br />

V(A2) 12,65 2,75 12,65 2,75<br />

E(V(A1)) = 7,94 E(V(A2)) = 7,70<br />

41

Prof. Dr. Hans-Peter Burghof, University of Hohenheim, Bank Management<br />

Risk <strong>Transformation</strong> by Diversification:<br />

state: s1 s2 s3 s4<br />

A1 x11 = 130 x12 = 130 x13 = 90 x14 = 90<br />

A2 x21 = 160 x22 = 60 x21 = 160 x22 = 60<br />

Portfolio formation: Purchase α = 50% of A1 <strong>and</strong> (1 – α) = 50% of A2<br />

½ A1 + ½ A2 xd1 = 145 xd2 = 95 xd3 = 125 xd4 = 75<br />

U(α = 50%) 12.04 9.75 11.18 8.66<br />

V(α = 50%) 12.04 4.75 11.18 3.66<br />

E(U(α = 50%)) = 10,40 E(V(α = 50%)) = 7,90<br />

(“naive” diversification, without success in this case)<br />

Portfolio formation:<br />

Purchase α = 86.52% of A1 <strong>and</strong> (1 - α) = 13.48% of A2<br />

xd1 = 134,04 xd2 = 120.56 xd3 = 99.44 xd4 = 85.96<br />

U(α = 86,52%) 11.58 10.98 9,97 9.27<br />

V(α = 86,52%) 11.58 10.98 4.97 4.27<br />

E(U(α = 86.52%)) = 10.45 E(V(α = 86.52%)) = 7.95<br />

(optimal diversification for utility function U)<br />

Instruments:<br />

Diversification via portfolio formation<br />

Buying shares in a fund<br />

Buying bank or insurance shares<br />

42

Prof. Dr. Hans-Peter Burghof, University of Hohenheim, Bank Management<br />

Risk <strong>Transformation</strong> by Risk Splitting:<br />

state: s1 s2 s3 s4<br />

A1 x11 = 130 x12 = 130 x13 = 90 x14 = 90<br />

A2 x21 = 160 x22 = 60 x21 = 160 x22 = 60<br />

“No-loss“ contract (e.g. on A1):<br />

xsl1 = 120 xsl2 = 120 xsl3 = 100 xsl4 = 100<br />

U(SL) = V(SL) 10,95 10,95 10 10<br />

Risk free asset:<br />

E(U(x)) = E(V(x)) = 10,47<br />

xrl1 = 110 xsl2 = 110 xsl3 = 110 xsl4 = 110<br />

U(RF) = V(RF) 10,49 10,49 10,49 10,49<br />

E(U(x)) = E(V(x)) = 10,49<br />

Hedging or financial engineering by:<br />

Contracting with a bank<br />

A particular fund construction<br />

Buying financial assets on the capital market<br />

43

Prof. Dr. Hans-Peter Burghof, University of Hohenheim, Bank Management<br />

<strong>Financial</strong> Engineering on the Capital Market:<br />

E.g.: Combination of shares in A1 <strong>and</strong> a (long) put option<br />

Wealth of the investor<br />

in T<br />

State: s1 s2 s3 s4<br />

A1 (α of 100) α130 α130 α90 α90<br />

Put option with<br />

strike P on α A1<br />

0 0 α(P – 90) α(P – 90)<br />

Desired cash flow xsl1 = 120 xsl2 = 120 xsl3 = 100 Xsl4 = 100<br />

130<br />

120 <br />

90<br />

<br />

Costs:<br />

Desired<br />

Minimum Wealth<br />

in T<br />

(e.g. 100)<br />

12<br />

13<br />

100<br />

<br />

100 13<br />

12<br />

P90100 P 108,<br />

3<br />

(risk free interest rate i = 10% <strong>and</strong> risk neutral valuation of the option)<br />

Buying shares of the asset A1:<br />

Buying a put option 1<br />

<br />

on share α of the asset : 2<br />

Total costs :<br />

Portfolio<br />

A1<br />

1 1 12<br />

108, 3 90<br />

108, 3 90<br />

92,<br />

31<br />

Put Option<br />

<br />

7,<br />

69<br />

100<br />

<br />

100<br />

44<br />

1<br />

i<br />

92,<br />

31<br />

Value of the Asset in T<br />

2 13<br />

1<br />

1,<br />

1<br />

<br />

7,<br />

69