Introduction to Local Level Model and Kalman Filter

Introduction to Local Level Model and Kalman Filter

Introduction to Local Level Model and Kalman Filter

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

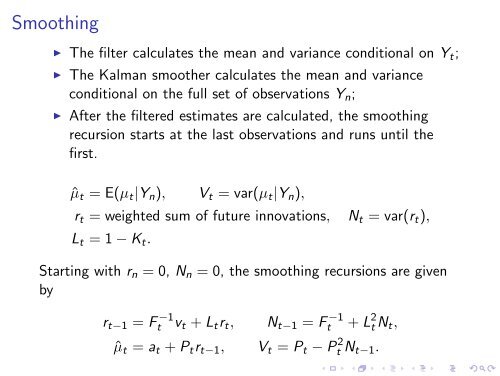

Smoothing<br />

◮ The filter calculates the mean <strong>and</strong> variance conditional on Yt;<br />

◮ The <strong>Kalman</strong> smoother calculates the mean <strong>and</strong> variance<br />

conditional on the full set of observations Yn;<br />

◮ After the filtered estimates are calculated, the smoothing<br />

recursion starts at the last observations <strong>and</strong> runs until the<br />

first.<br />

ˆµt = E(µt|Yn), Vt = var(µt|Yn),<br />

rt = weighted sum of future innovations, Nt = var(rt),<br />

Lt = 1 − Kt.<br />

Starting with rn = 0, Nn = 0, the smoothing recursions are given<br />

by<br />

rt−1 = F −1<br />

t vt + Ltrt, Nt−1 = F −1<br />

t + L 2 t Nt,<br />

ˆµt = at + Ptrt−1, Vt = Pt − P 2 t Nt−1.