Introduction to Local Level Model and Kalman Filter

Introduction to Local Level Model and Kalman Filter

Introduction to Local Level Model and Kalman Filter

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

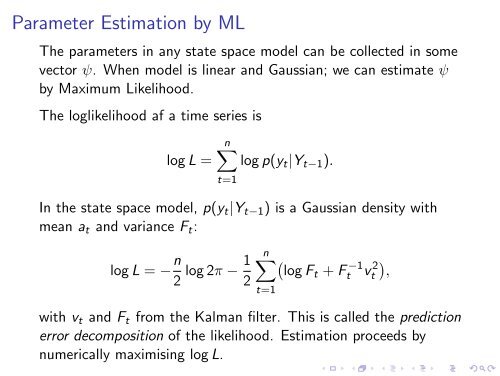

Parameter Estimation by ML<br />

The parameters in any state space model can be collected in some<br />

vec<strong>to</strong>r ψ. When model is linear <strong>and</strong> Gaussian; we can estimate ψ<br />

by Maximum Likelihood.<br />

The loglikelihood af a time series is<br />

log L =<br />

n<br />

log p(yt|Yt−1).<br />

t=1<br />

In the state space model, p(yt|Yt−1) is a Gaussian density with<br />

mean at <strong>and</strong> variance Ft:<br />

log L = − n 1<br />

log 2π −<br />

2 2<br />

n<br />

t=1<br />

log Ft + F −1<br />

t v 2 t<br />

with vt <strong>and</strong> Ft from the <strong>Kalman</strong> filter. This is called the prediction<br />

error decomposition of the likelihood. Estimation proceeds by<br />

numerically maximising log L.<br />

,