Introduction to Local Level Model and Kalman Filter

Introduction to Local Level Model and Kalman Filter

Introduction to Local Level Model and Kalman Filter

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

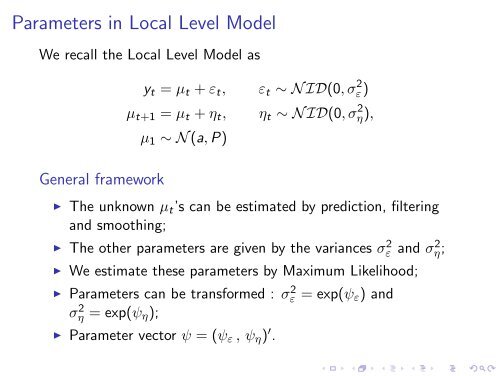

Parameters in <strong>Local</strong> <strong>Level</strong> <strong>Model</strong><br />

We recall the <strong>Local</strong> <strong>Level</strong> <strong>Model</strong> as<br />

General framework<br />

yt = µt + εt, εt ∼ N ID(0, σ 2 ε)<br />

µt+1 = µt + ηt, ηt ∼ N ID(0, σ 2 η),<br />

µ1 ∼ N (a, P)<br />

◮ The unknown µt’s can be estimated by prediction, filtering<br />

<strong>and</strong> smoothing;<br />

◮ The other parameters are given by the variances σ 2 ε <strong>and</strong> σ 2 η;<br />

◮ We estimate these parameters by Maximum Likelihood;<br />

◮ Parameters can be transformed : σ 2 ε = exp(ψε) <strong>and</strong><br />

σ 2 η = exp(ψη);<br />

◮ Parameter vec<strong>to</strong>r ψ = (ψε , ψη) ′ .