Entropy Coherent and Entropy Convex Measures of Risk - Eurandom

Entropy Coherent and Entropy Convex Measures of Risk - Eurandom

Entropy Coherent and Entropy Convex Measures of Risk - Eurandom

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

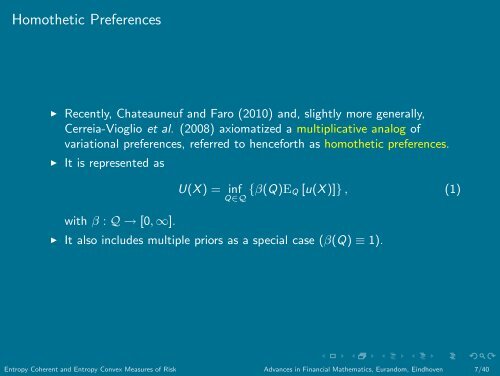

Homothetic Preferences<br />

◮ Recently, Chateauneuf <strong>and</strong> Faro (2010) <strong>and</strong>, slightly more generally,<br />

Cerreia-Vioglio et al. (2008) axiomatized a multiplicative analog <strong>of</strong><br />

variational preferences, referred to henceforth as homothetic preferences.<br />

◮ It is represented as<br />

with β : Q → [0, ∞].<br />

U(X) = inf<br />

Q∈Q {β(Q)EQ [u(X)]} , (1)<br />

◮ It also includes multiple priors as a special case (β(Q) ≡ 1).<br />

<strong>Entropy</strong> <strong>Coherent</strong> <strong>and</strong> <strong>Entropy</strong> <strong>Convex</strong> <strong>Measures</strong> <strong>of</strong> <strong>Risk</strong> Advances in Financial Mathematics, Eur<strong>and</strong>om, Eindhoven 7/40

![The Contraction Method on C([0,1]) and Donsker's ... - Eurandom](https://img.yumpu.com/19554492/1/190x143/the-contraction-method-on-c01-and-donskers-eurandom.jpg?quality=85)