Strengths, Weaknesses and Evolution of the Peace Corps' 11-Year ...

Strengths, Weaknesses and Evolution of the Peace Corps' 11-Year ...

Strengths, Weaknesses and Evolution of the Peace Corps' 11-Year ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Despite this recommendation, some community banks allow <strong>the</strong>ir members to save different<br />

amounts. As indicated in <strong>the</strong> table below, it was more common in Bahía than in Loja for members<br />

in <strong>the</strong> same community bank to save different amounts. Ninety-two percent <strong>of</strong> <strong>the</strong> community<br />

banks in <strong>the</strong> Bahía sample allowed its members to save different amounts compared to only 36% in<br />

<strong>the</strong> Loja sample. Groups in Bahía may save varying amounts because <strong>the</strong>y are older <strong>and</strong> have had<br />

less direct training on <strong>the</strong> PAC methodology, as <strong>the</strong>y were formed by untrained community<br />

members.<br />

Percentage <strong>of</strong> groups that allow <strong>the</strong>ir<br />

members to save different amounts<br />

Bahía Loja<br />

92%<br />

(<strong>11</strong>/12)<br />

36%<br />

(4/<strong>11</strong>)<br />

Bahía/Loja<br />

Combined Range<br />

65%<br />

(15/23) N/A<br />

The 2002 Community Banking Evaluation found that less than one-half (43%) <strong>of</strong> community banks<br />

had extra shares or <strong>the</strong>ir members saved different amounts. While this is similar to <strong>the</strong> findings for<br />

Loja in <strong>the</strong> 2010 study, it is significantly different for Bahía, where <strong>the</strong> majority <strong>of</strong> members<br />

save different amounts. Despite <strong>the</strong> complications <strong>of</strong> saving different amounts, <strong>the</strong> members in<br />

Bahía seem to prefer this more flexible arrangement <strong>and</strong> manage to adapt <strong>the</strong> accounting to<br />

accommodate <strong>the</strong> different savings amounts.<br />

3.4.2 Interest Rate<br />

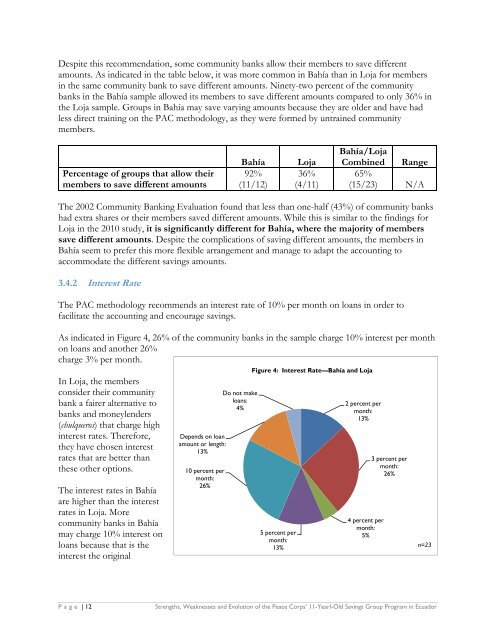

The PAC methodology recommends an interest rate <strong>of</strong> 10% per month on loans in order to<br />

facilitate <strong>the</strong> accounting <strong>and</strong> encourage savings.<br />

As indicated in Figure 4, 26% <strong>of</strong> <strong>the</strong> community banks in <strong>the</strong> sample charge 10% interest per month<br />

on loans <strong>and</strong> ano<strong>the</strong>r 26%<br />

charge 3% per month.<br />

In Loja, <strong>the</strong> members<br />

consider <strong>the</strong>ir community<br />

bank a fairer alternative to<br />

banks <strong>and</strong> moneylenders<br />

(chulqueros) that charge high<br />

interest rates. Therefore,<br />

<strong>the</strong>y have chosen interest<br />

rates that are better than<br />

<strong>the</strong>se o<strong>the</strong>r options.<br />

The interest rates in Bahía<br />

are higher than <strong>the</strong> interest<br />

rates in Loja. More<br />

community banks in Bahía<br />

may charge 10% interest on<br />

loans because that is <strong>the</strong><br />

interest <strong>the</strong> original<br />

Depends on loan<br />

amount or length:<br />

13%<br />

10 percent per<br />

month:<br />

26%<br />

Do not make<br />

loans:<br />

4%<br />

Figure 4: Interest Rate—Bahía <strong>and</strong> Loja<br />

5 percent per<br />

month:<br />

13%<br />

2 percent per<br />

month:<br />

13%<br />

4 percent per<br />

month:<br />

5%<br />

3 percent per<br />

month:<br />

26%<br />

Page | 12 <strong>Strengths</strong>, <strong>Weaknesses</strong> <strong>and</strong> <strong>Evolution</strong> <strong>of</strong> <strong>the</strong> <strong>Peace</strong> Corps’ <strong>11</strong>-<strong>Year</strong>l-Old Savings Group Program in Ecuador<br />

n=23