Chapter Nine- Activity-Based Costing

Chapter Nine- Activity-Based Costing

Chapter Nine- Activity-Based Costing

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

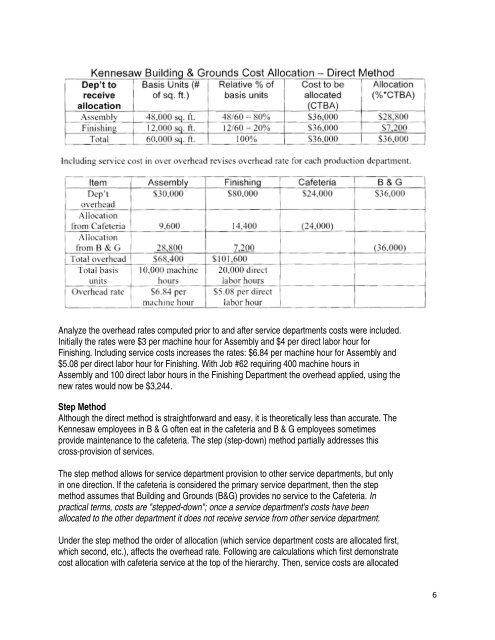

Analyze the overhead rates computed prior to and after service departments costs were included.<br />

Initially the rates were $3 per machine hour for Assembly and $4 per direct labor hour for<br />

Finishing. Including service costs increases the rates: $6.84 per machine hour for Assembly and<br />

$5.08 per direct labor hour for Finishing. With Job #62 requiring 400 machine hours in<br />

Assembly and 100 direct labor hours in the Finishing Department the overhead applied, using the<br />

new rates would now be $3,244.<br />

Step Method<br />

Although the direct method is straightforward and easy, it is theoretically less than accurate. The<br />

Kennesaw employees in B & G often eat in the cafeteria and B & G employees sometimes<br />

provide maintenance to the cafeteria. The step (step-down) method partially addresses this<br />

cross-provision of services.<br />

The step method allows for service department provision to other service departments, but only<br />

in one direction. If the cafeteria is considered the primary service department, then the step<br />

method assumes that Building and Grounds (B&G) provides no service to the Cafeteria. In<br />

practical terms, costs are "stepped-down"; once a service department's costs have been<br />

allocated to the other department it does not receive service from other service department.<br />

Under the step method the order of allocation (which service department costs are allocated first,<br />

which second, etc.), affects the overhead rate. Following are calculations which first demonstrate<br />

cost allocation with cafeteria service at the top of the hierarchy. Then, service costs are allocated<br />

6