- Page 1 and 2:

EQUI-VEST ® COMBINATION VARIABLE A

- Page 3 and 4:

EQUI-VEST SM A combination variable

- Page 5 and 6:

Contents of this prospectus EQUI-VE

- Page 7 and 8:

Index of key words and phrases This

- Page 9 and 10:

How to reach us Please communicate

- Page 11 and 12:

EQUI-VEST SM at a glance — key fe

- Page 13 and 14:

Other contracts We offer a variety

- Page 15 and 16:

This table shows the fees and expen

- Page 17 and 18:

Portfolio Name: EQ/AllianceBernstei

- Page 19 and 20:

EQ ADVISORS TRUST: If you surrender

- Page 21 and 22:

1. Contract features and benefits H

- Page 23 and 24:

Owner and annuitant requirements Un

- Page 25 and 26:

AXA Premier VIP Trust Portfolio Nam

- Page 27 and 28:

EQ Advisors Trust Portfolio Name EQ

- Page 29 and 30:

Guaranteed interest option The guar

- Page 31 and 32:

Allocating your contributions Once

- Page 33 and 34:

owner’s original IRA. You should

- Page 35 and 36:

3. Transferring your money among in

- Page 37 and 38:

• Under the interest sweep, when

- Page 39 and 40:

Currently, we do not impose a withd

- Page 41 and 42:

in general, the longer the period o

- Page 43 and 44:

owned EQUI-VEST SM contract/certifi

- Page 45 and 46:

The charge is deducted pro rata fro

- Page 47 and 48:

Single sum payments generally are p

- Page 49 and 50:

7. Tax information Overview In this

- Page 51 and 52:

The circumstances that would lead t

- Page 53 and 54:

which you make the contribution inc

- Page 55 and 56:

plan, 403(b) plan or governmental e

- Page 57 and 58:

Roth individual retirement annuitie

- Page 59 and 60:

SEP-IRA or SIMPLE IRA). You cannot

- Page 61 and 62:

Table I at the guaranteed minimum r

- Page 63 and 64:

8. More information About our Separ

- Page 65 and 66:

We have been advised that the staff

- Page 67 and 68:

on the basis of contributions alone

- Page 69 and 70:

Appendix I: QP IRA contracts The fo

- Page 71 and 72:

Unit values and number of units out

- Page 73 and 74:

Unit values and number of units out

- Page 75 and 76:

Appendix III: Market value adjustme

- Page 77 and 78:

Appendix V: State contract availabi

- Page 79 and 80:

State Features / benefits / charges

- Page 81:

AXA Equitable Life Insurance Compan

- Page 85 and 86:

INTRODUCTION AXA Premier VIP Trust

- Page 87 and 88:

THE AXA ALLOCATION PORTFOLIOS AT A

- Page 89 and 90:

AXA CONSERVATIVE ALLOCATION PORTFOL

- Page 91 and 92:

AXA CONSERVATIVE-PLUS ALLOCATION PO

- Page 93 and 94:

AXA MODERATE ALLOCATION PORTFOLIO M

- Page 95 and 96:

AXA MODERATE-PLUS ALLOCATION PORTFO

- Page 97 and 98:

AXA AGGRESSIVE ALLOCATION PORTFOLIO

- Page 99 and 100:

FEES AND EXPENSES OF THE AXA ALLOCA

- Page 101 and 102:

MORE ABOUT INVESTMENT STRATEGIES &

- Page 103 and 104:

MORE ABOUT INVESTMENT STRATEGIES &

- Page 105 and 106:

MORE ABOUT INVESTMENT STRATEGIES &

- Page 107 and 108:

MORE ABOUT INVESTMENT STRATEGIES &

- Page 109 and 110:

INFORMATION REGARDING THE UNDERLYIN

- Page 111 and 112:

INFORMATION REGARDING THE UNDERLYIN

- Page 113 and 114:

INFORMATION REGARDING THE UNDERLYIN

- Page 115 and 116:

INFORMATION REGARDING THE UNDERLYIN

- Page 117 and 118:

INFORMATION REGARDING THE UNDERLYIN

- Page 119 and 120:

INFORMATION REGARDING THE UNDERLYIN

- Page 121 and 122:

INFORMATION REGARDING THE UNDERLYIN

- Page 123 and 124:

INFORMATION REGARDING THE UNDERLYIN

- Page 125 and 126:

INFORMATION REGARDING THE UNDERLYIN

- Page 127 and 128:

INFORMATION REGARDING THE UNDERLYIN

- Page 129 and 130:

MANAGEMENT TEAM The Manager The Man

- Page 131 and 132:

PORTFOLIO SERVICES Buying and Selli

- Page 133 and 134:

PORTFOLIO SERVICES (cont’d) • T

- Page 135 and 136:

DESCRIPTION OF BENCHMARKS Broad-bas

- Page 137 and 138:

FINANCIAL HIGHLIGHTS The following

- Page 139 and 140:

FINANCIAL HIGHLIGHTS (cont’d) AXA

- Page 141 and 142:

FINANCIAL HIGHLIGHTS (cont’d) AXA

- Page 143 and 144:

FINANCIAL HIGHLIGHTS (cont’d) AXA

- Page 145 and 146:

FINANCIAL HIGHLIGHTS (cont’d) AXA

- Page 147 and 148:

FINANCIAL HIGHLIGHTS (cont’d) * C

- Page 149 and 150:

EQ Advisors Trust SM Prospectus dat

- Page 151 and 152:

Table of contents 1. About the Inve

- Page 153 and 154:

Equity Portfolios EQ/AllianceBernst

- Page 155 and 156:

EQ/AllianceBernstein International

- Page 157 and 158:

coordinating the portfolio’s inve

- Page 159 and 160:

Average Annual Total Returns One Ye

- Page 161 and 162:

EQ/AllianceBernstein Small Cap Grow

- Page 163 and 164:

EQ/AllianceBernstein Value Portfoli

- Page 165 and 166:

John Phillips is a Senior Portfolio

- Page 167 and 168:

Annual Portfolio Operating Expenses

- Page 169 and 170:

Trust) advised by the same Adviser

- Page 171 and 172:

EQ/BlackRock Basic Value Equity Por

- Page 173 and 174:

and Portfolio Manager with BlackRoc

- Page 175 and 176:

Calendar Year Annual Total Returns

- Page 177 and 178:

EQ/Boston Advisors Equity Income Po

- Page 179 and 180:

EQ/Calvert Socially Responsible Por

- Page 181 and 182:

† The maximum annual distribution

- Page 183 and 184:

Annual Portfolio Operating Expenses

- Page 185 and 186:

EQ/Capital Guardian Research Portfo

- Page 187 and 188:

EQ/Davis New York Venture Portfolio

- Page 189 and 190:

EQ/Equity 500 Index Portfolio INVES

- Page 191 and 192:

EQ/Evergreen Omega Portfolio INVEST

- Page 193 and 194:

EQ/FI Mid Cap Portfolio INVESTMENT

- Page 195 and 196:

EQ/Franklin Income Portfolio INVEST

- Page 197 and 198:

assessment, and the management of d

- Page 199 and 200:

Average Annual Total Returns Since

- Page 201 and 202:

EQ/GAMCO Mergers and Acquisitions P

- Page 203 and 204:

WHO MANAGES THE PORTFOLIO GAMCO Ass

- Page 205 and 206:

There are no fees or charges to buy

- Page 207 and 208:

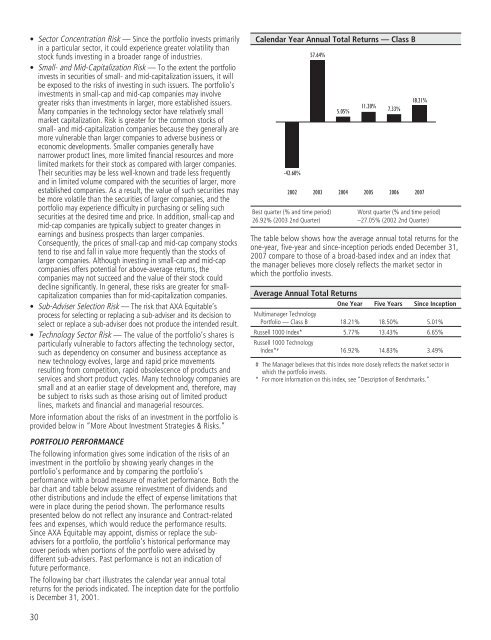

PORTFOLIO PERFORMANCE The bar chart

- Page 209 and 210:

EQ/International Growth Portfolio I

- Page 211 and 212:

EQ/JPMorgan Value Opportunities Por

- Page 213 and 214:

EQ/Large Cap Core PLUS Portfolio IN

- Page 215 and 216:

management fees, bear its pro rata

- Page 217 and 218:

EQ/Large Cap Growth PLUS Portfolio

- Page 219 and 220:

*** A portion of the brokerage comm

- Page 221 and 222:

† For more information on this in

- Page 223 and 224:

PORTFOLIO FEES AND EXPENSES The fol

- Page 225 and 226:

Average Annual Total Returns Since

- Page 227 and 228:

Average Annual Total Returns Since

- Page 229 and 230:

PORTFOLIO PERFORMANCE The bar chart

- Page 231 and 232:

EQ/Mid Cap Value PLUS Portfolio INV

- Page 233 and 234:

that the Portfolio’s operating ex

- Page 235 and 236:

PORTFOLIO FEES AND EXPENSES The fol

- Page 237 and 238:

for this Portfolio is September 15,

- Page 239 and 240:

EQ/Oppenheimer Global Portfolio INV

- Page 241 and 242:

EQ/Oppenheimer Main Street Opportun

- Page 243 and 244:

EQ/Oppenheimer Main Street Small Ca

- Page 245 and 246:

Class IB Shares 1 Year $ 133 3 Year

- Page 247 and 248:

PORTFOLIO FEES AND EXPENSES The fol

- Page 249 and 250:

† For more information on this in

- Page 251 and 252:

Annual Portfolio Operating Expenses

- Page 253 and 254:

PORTFOLIO FEES AND EXPENSES The fol

- Page 255 and 256:

Annual Portfolio Operating Expenses

- Page 257 and 258:

Average Annual Total Returns One Ye

- Page 259 and 260:

EQ/Van Kampen Mid Cap Growth Portfo

- Page 261 and 262:

EQ/Van Kampen Real Estate Portfolio

- Page 263 and 264:

Fixed Income Portfolios EQ/Alliance

- Page 265 and 266:

Annual Portfolio Operating Expenses

- Page 267 and 268:

esults of the Portfolio (to which t

- Page 269 and 270:

EQ/Bond Index Portfolio INVESTMENT

- Page 271 and 272:

EQ/Caywood-Scholl High Yield Bond P

- Page 273 and 274:

EQ/Evergreen International Bond Por

- Page 275 and 276:

EQ/JPMorgan Core Bond Portfolio INV

- Page 277 and 278:

EQ/Long Term Bond Portfolio INVESTM

- Page 279 and 280:

EQ/Money Market Portfolio INVESTMEN

- Page 281 and 282:

EQ/PIMCO Real Return Portfolio INVE

- Page 283 and 284:

EQ/Short Duration Bond Portfolio IN

- Page 285 and 286:

The Statement of Additional Informa

- Page 287 and 288:

significant impact on a Portfolio

- Page 289 and 290:

ability to make payments of princip

- Page 291 and 292:

Portfolio may have to hold these se

- Page 293 and 294:

Benchmarks The performance of each

- Page 295 and 296:

3. More information on investing in

- Page 297 and 298:

Information Regarding the Underlyin

- Page 299 and 300:

Information Regarding the Underlyin

- Page 301 and 302:

Information Regarding the Underlyin

- Page 303 and 304:

Information Regarding the Underlyin

- Page 305 and 306:

Information Regarding the Underlyin

- Page 307 and 308:

Information Regarding the Underlyin

- Page 309 and 310:

Information Regarding the Underlyin

- Page 311 and 312:

4. Management of the Trust This sec

- Page 313 and 314:

Cap Core PLUS Portfolio and the inv

- Page 315 and 316:

eached an agreement in principle wi

- Page 317 and 318:

plan to be developed by an independ

- Page 319 and 320:

5. Fund distribution arrangements T

- Page 321 and 322:

net inflows and outflows exceed an

- Page 323 and 324:

8. Dividends and other distribution

- Page 325 and 326:

10. Financial Highlights The financ

- Page 327 and 328:

Financial Highlights (cont’d) EQ/

- Page 329 and 330:

Financial Highlights (cont’d) EQ/

- Page 331 and 332:

Financial Highlights (cont’d) EQ/

- Page 333 and 334:

Financial Highlights (cont’d) EQ/

- Page 335 and 336:

Financial Highlights (cont’d) EQ/

- Page 337 and 338:

Financial Highlights (cont’d) EQ/

- Page 339 and 340:

Financial Highlights (cont’d) EQ/

- Page 341 and 342:

Financial Highlights (cont’d) EQ/

- Page 343 and 344:

Financial Highlights (cont’d) EQ/

- Page 345 and 346:

Financial Highlights (cont’d) EQ/

- Page 347 and 348:

Financial Highlights (cont’d) EQ/

- Page 349 and 350:

Financial Highlights (cont’d) EQ/

- Page 351 and 352:

Financial Highlights (cont’d) EQ/

- Page 353 and 354:

Financial Highlights (cont’d) EQ/

- Page 355 and 356:

Financial Highlights (cont’d) EQ/

- Page 357 and 358:

Financial Highlights (cont’d) EQ/

- Page 359 and 360:

Financial Highlights (cont’d) EQ/

- Page 361 and 362:

Financial Highlights (cont’d) EQ/

- Page 363 and 364:

Financial Highlights (cont’d) EQ/

- Page 365 and 366:

Financial Highlights (cont’d) EQ/

- Page 367 and 368:

Financial Highlights (cont’d) EQ/

- Page 369 and 370:

Financial Highlights (cont’d) EQ/

- Page 371 and 372:

Financial Highlights (cont’d) EQ/

- Page 373 and 374:

Financial Highlights (cont’d) EQ/

- Page 375 and 376:

Financial Highlights (cont’d) EQ/

- Page 377 and 378:

Financial Highlights (cont’d) EQ/

- Page 379 and 380:

Financial Highlights (cont’d) EQ/

- Page 382 and 383:

If you would like more information

- Page 384 and 385:

Overview EQ ADVISORS TRUST EQ Advis

- Page 386 and 387:

1. About the investment portfolio T

- Page 388 and 389:

• Investment Grade Securities Ris

- Page 390 and 391: 2. More information on risks and th

- Page 392 and 393: grade securities. Lower rated bonds

- Page 394 and 395: Information Regarding the Franklin

- Page 396 and 397: 3. Management of the Trust The Trus

- Page 398 and 399: 4. Fund distribution arrangements T

- Page 400 and 401: tinues, AXA Equitable may take acti

- Page 402 and 403: 7. Dividends and other distribution

- Page 404: 9. Financial Highlights The financi

- Page 407: PROSPECTUS May 1, 2008 AXA PREMIER

- Page 410 and 411: Table of CONTENTS Goals, Strategies

- Page 412 and 413: • Derivatives Risk — Derivative

- Page 414 and 415: MULTIMANAGER CORE BOND PORTFOLIO Ma

- Page 416 and 417: More information about the risks of

- Page 418 and 419: small number of issuers, which may

- Page 420 and 421: sub-advisers and may dismiss, repla

- Page 422 and 423: MULTIMANAGER INTERNATIONAL EQUITY P

- Page 424 and 425: MULTIMANAGER LARGE CAP CORE EQUITY

- Page 426 and 427: MULTIMANAGER LARGE CAP GROWTH PORTF

- Page 428 and 429: MULTIMANAGER LARGE CAP VALUE PORTFO

- Page 430 and 431: MULTIMANAGER MID CAP GROWTH PORTFOL

- Page 432 and 433: MULTIMANAGER MID CAP VALUE PORTFOLI

- Page 434 and 435: MULTIMANAGER SMALL CAP GROWTH PORTF

- Page 436 and 437: The following bar chart illustrates

- Page 438 and 439: • Large Capitalization Risk — L

- Page 442 and 443: PORTFOLIO FEES & EXPENSES (cont’d

- Page 444 and 445: PORTFOLIO FEES & EXPENSES (cont’d

- Page 446 and 447: MORE ABOUT INVESTMENT STRATEGIES &

- Page 448 and 449: MORE ABOUT INVESTMENT STRATEGIES &

- Page 450 and 451: MANAGEMENT TEAM The Manager and the

- Page 452 and 453: MANAGEMENT TEAM The Manager and the

- Page 454 and 455: MANAGEMENT TEAM The Manager and the

- Page 456 and 457: MANAGEMENT TEAM The Manager and the

- Page 458 and 459: MANAGEMENT TEAM The Manager and the

- Page 460 and 461: MANAGEMENT TEAM The Manager and the

- Page 462 and 463: MANAGEMENT TEAM The Manager and the

- Page 464 and 465: MANAGEMENT TEAM The Manager and the

- Page 466 and 467: MANAGEMENT TEAM The Manager and the

- Page 468 and 469: MANAGEMENT TEAM The Manager and the

- Page 470 and 471: MANAGEMENT TEAM The Manager and the

- Page 472 and 473: MANAGEMENT TEAM The Manager and the

- Page 474 and 475: PORTFOLIO SERVICES (cont’d) telep

- Page 476 and 477: PORTFOLIO SERVICES (cont’d) Tax C

- Page 478 and 479: DESCRIPTION OF BENCHMARKS Each port

- Page 480 and 481: FINANCIAL HIGHLIGHTS The financial

- Page 482 and 483: FINANCIAL HIGHLIGHTS (cont’d) Mul

- Page 484 and 485: FINANCIAL HIGHLIGHTS (cont’d) Mul

- Page 486 and 487: FINANCIAL HIGHLIGHTS (cont’d) Mul

- Page 488 and 489: FINANCIAL HIGHLIGHTS (cont’d) Mul

- Page 490 and 491:

FINANCIAL HIGHLIGHTS (cont’d) Mul

- Page 492 and 493:

FINANCIAL HIGHLIGHTS (cont’d) Mul

- Page 494 and 495:

FINANCIAL HIGHLIGHTS (cont’d) Mul

- Page 496 and 497:

FINANCIAL HIGHLIGHTS (cont’d) Mul

- Page 498 and 499:

FINANCIAL HIGHLIGHTS (cont’d) Mul

- Page 500 and 501:

FINANCIAL HIGHLIGHTS (cont’d) Mul

- Page 502:

FINANCIAL HIGHLIGHTS (cont’d) * P

- Page 505:

PROSPECTUS MAY 1, 2008 AXA PREMIER

- Page 508 and 509:

Table of CONTENTS Goals, Strategies

- Page 510 and 511:

Underlying Portfolios.” Each of t

- Page 512 and 513:

Target 2035 Allocation Portfolio Ca

- Page 514 and 515:

FEES AND EXPENSES OF THE TARGET ALL

- Page 516 and 517:

MORE ABOUT INVESTMENT STRATEGIES &

- Page 518 and 519:

MORE ABOUT INVESTMENT STRATEGIES &

- Page 520 and 521:

MORE ABOUT INVESTMENT STRATEGIES &

- Page 522 and 523:

INFORMATION REGARDING THE UNDERLYIN

- Page 524 and 525:

INFORMATION REGARDING THE UNDERLYIN

- Page 526 and 527:

INFORMATION REGARDING THE UNDERLYIN

- Page 528 and 529:

INFORMATION REGARDING THE UNDERLYIN

- Page 530 and 531:

INFORMATION REGARDING THE UNDERLYIN

- Page 532 and 533:

MANAGEMENT TEAM The Manager (cont

- Page 534 and 535:

PORTFOLIO SERVICES (cont’d) If AX

- Page 536 and 537:

PORTFOLIO SERVICES (cont’d) Tax C

- Page 538 and 539:

FINANCIAL HIGHLIGHTS The following

- Page 540 and 541:

FINANCIAL HIGHLIGHTS (cont’d) Tar

- Page 542 and 543:

FINANCIAL HIGHLIGHTS (cont’d) Tar

- Page 544:

FINANCIAL HIGHLIGHTS (cont’d) * C

- Page 547 and 548:

DEPARTMENT OF LABOR NOTICE AXA Equi