GST: A Guide on Exports (Eleventh Edition) - IRAS

GST: A Guide on Exports (Eleventh Edition) - IRAS

GST: A Guide on Exports (Eleventh Edition) - IRAS

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

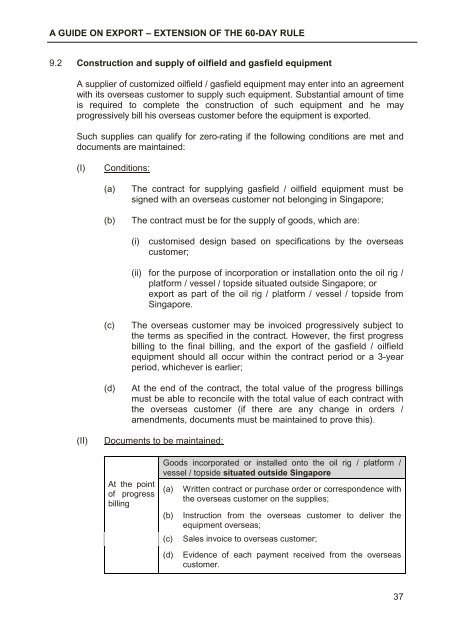

A GUIDE ON EXPORT – EXTENSION OF THE 60-DAY RULE<br />

9.2 C<strong>on</strong>structi<strong>on</strong> and supply of oilfield and gasfield equipment<br />

A supplier of customized oilfield / gasfield equipment may enter into an agreement<br />

with its overseas customer to supply such equipment. Substantial amount of time<br />

is required to complete the c<strong>on</strong>structi<strong>on</strong> of such equipment and he may<br />

progressively bill his overseas customer before the equipment is exported.<br />

Such supplies can qualify for zero-rating if the following c<strong>on</strong>diti<strong>on</strong>s are met and<br />

documents are maintained:<br />

(I)<br />

C<strong>on</strong>diti<strong>on</strong>s:<br />

(a)<br />

(b)<br />

The c<strong>on</strong>tract for supplying gasfield / oilfield equipment must be<br />

signed with an overseas customer not bel<strong>on</strong>ging in Singapore;<br />

The c<strong>on</strong>tract must be for the supply of goods, which are:<br />

(i)<br />

customised design based <strong>on</strong> specificati<strong>on</strong>s by the overseas<br />

customer;<br />

(ii) for the purpose of incorporati<strong>on</strong> or installati<strong>on</strong> <strong>on</strong>to the oil rig /<br />

platform / vessel / topside situated outside Singapore; or<br />

export as part of the oil rig / platform / vessel / topside from<br />

Singapore.<br />

(c)<br />

(d)<br />

The overseas customer may be invoiced progressively subject to<br />

the terms as specified in the c<strong>on</strong>tract. However, the first progress<br />

billing to the final billing, and the export of the gasfield / oilfield<br />

equipment should all occur within the c<strong>on</strong>tract period or a 3-year<br />

period, whichever is earlier;<br />

At the end of the c<strong>on</strong>tract, the total value of the progress billings<br />

must be able to rec<strong>on</strong>cile with the total value of each c<strong>on</strong>tract with<br />

the overseas customer (if there are any change in orders /<br />

amendments, documents must be maintained to prove this).<br />

(II)<br />

Documents to be maintained:<br />

At the point<br />

of progress<br />

billing<br />

Goods incorporated or installed <strong>on</strong>to the oil rig / platform /<br />

vessel / topside situated outside Singapore<br />

(a)<br />

(b)<br />

(c)<br />

(d)<br />

Written c<strong>on</strong>tract or purchase order or corresp<strong>on</strong>dence with<br />

the overseas customer <strong>on</strong> the supplies;<br />

Instructi<strong>on</strong> from the overseas customer to deliver the<br />

equipment overseas;<br />

Sales invoice to overseas customer;<br />

Evidence of each payment received from the overseas<br />

customer.<br />

37