November 2010 - Welspun

November 2010 - Welspun

November 2010 - Welspun

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

On The Path of Global Leadership…<br />

WELSPUN CITY, ANJAR<br />

<strong>November</strong> <strong>2010</strong> Page 1

Disclaimer<br />

Certain statements made in this presentation may not be based on historical information or facts and may be “forward looking statements,” including<br />

those relating to general business plans and strategy of <strong>Welspun</strong> Corp. Limited (“WCL"), its future outlook and growth prospects, and future<br />

developments in its businesses and its competitive and regulatory environment. Actual results may differ materially from these forward-looking<br />

statements due to a number of factors, inter alia including future changes or developments in WCL's business, its competitive environment, its ability<br />

to implement its strategies and initiatives and respond to technological changes and political, economic, regulatory and social conditions in India.<br />

This presentation does not constitute a prospectus, offering circular or offering memorandum or an offer invitation, or a solicitation of any offer, to<br />

purchase or sell, any shares of WCL and should not be considered or construed in any manner whatsoever as a recommendation that any person<br />

should subscribe for or purchase any of WCL's shares. Neither this presentation nor any other documentation or information (or any part thereof)<br />

delivered or supplied under or in relation thereto shall be deemed to constitute an offer of or an invitation by or on behalf of WCL to subscribe for or<br />

purchase any of its shares.<br />

WCL, as such, makes no representation or warranty, express or implied, as to, and does not accept any responsibility or liability with respect to, the<br />

fairness, accuracy, completeness or correctness of any information or opinions contained herein. The information contained in this presentation,<br />

unless otherwise specified is only current as of the date of this presentation. WCL assumes no responsibility to publicly amend, modify or revise any<br />

forward looking statements contained herein, on the basis of any subsequent development, information or events, or otherwise. Unless otherwise<br />

stated in this document, the information contained herein is based on management information and estimates. The information contained herein is<br />

subject to change without notice and past performance is not indicative of future results. WCL may alter, modify or otherwise change in any manner<br />

the content of this presentation, without obligation to notify any person of such revision or changes. This presentation may not be copied and<br />

disseminated in any manner.<br />

THE INFORMATION PRESENTED HERE IS NOT AN OFFER INVITATION OR SOLICITATION OF ANY OFFER TO PURCHASE OR SELL ANY<br />

EQUITY SHARES OR ANY OTHER SECURITY OF WCL.<br />

This presentation is not for publication or distribution, directly or indirectly, in or into the United States, Canada or Japan.<br />

These materials are not an offer or solicitation of any offer of securities for purchase or sale in or into the United States, Canada or Japan.<br />

<strong>November</strong> <strong>2010</strong> Page 2

<strong>Welspun</strong> Group<br />

Brief Synopsis<br />

• One of the fastest emerging global groups, with multiple<br />

countries strategy and manufacturing facilities<br />

• Group companies enjoys market leadership positions :<br />

• Top 2 Large Diameter Pipe Company in World -<br />

Financial Times, UK<br />

• Globally renowned towel company<br />

• Global relationship with marquee clients including Fortune<br />

100 companies like Exxon Mobil (Golden Pass Pipeline),<br />

Chevron, Shell, Bechtel, Wal- Mart, Target etc<br />

• Equity investment by renowned investors like ICICI Life,<br />

Temasek (Govt. of Singapore), 3i (UK), Genesis (UK)<br />

• Excellent relationship with domestic and international lenders<br />

Global Recognitions<br />

<strong>Welspun</strong> Corp Star Performer Award for the year 2008-09<br />

All India Export Excellence Awards - EEPC <strong>2010</strong><br />

<strong>Welspun</strong> Corp<br />

Economic Times “Emerging Company of the Year Award”<br />

for Corporate Excellence - 2008<br />

<strong>Welspun</strong> India Gold Trophy for “Best Exporter” –<br />

Textile Promotion Council (TEXPROCIL) – 2008<br />

<strong>Welspun</strong> Corp<br />

2nd Largest (Large Diameter) Line Pipe Manufacturer<br />

in the World - Financial Times UK - 2008<br />

<strong>Welspun</strong> India Supplier of the Year Award – J C Penny - 2008<br />

Key Markets<br />

• 80% export mainly to US, Europe, Latin America, Middle East<br />

etc<br />

International Setup<br />

• Christy, UK<br />

• Sorema, Portugal<br />

• Textile facility in Mexico<br />

• Office in Manhattan-NY, Huston-US<br />

• Pipe facility in Arkansas, US<br />

• Pipe Facility in Saudi Arabia (In process)<br />

<strong>Welspun</strong> India<br />

Earth Care Awards – Times of India and<br />

Jindal Steel Ltd - 2008<br />

<strong>Welspun</strong> India Sustainability Award - Walmart - 2007<br />

<strong>Welspun</strong> Corp One of the fastest growing large companies in India –<br />

Business Today - 2007<br />

<strong>Welspun</strong> India 4 Gold Trophies for Outstanding Export Performance –<br />

Textile Promotion Council (TEXPROCIL) - 2007<br />

<strong>November</strong> <strong>2010</strong> Page 3

WCL – An Introduction<br />

• WCL, flagship company of <strong>Welspun</strong> Group, is one of the<br />

largest pipe manufacturing company in the world<br />

• Incorporated in 1995, the Company offers a complete range<br />

of high grade line pipes ranging from ½ inch to 100 inch<br />

used inter alia for transmission of oil & gas<br />

• Partner of Choice for more than 50 Oil & Gas Giants across<br />

the globe with a geographically diverse client base including<br />

Chevron, Exxon Mobil (Golden Pass Pipeline), Saudi Aramco,<br />

British Gas , Kinder Morgan etc<br />

• International footprint<br />

• Accredited with ISO 9001, ISO 14001 and OHSAS 18001<br />

certifications<br />

• Strong order book of U.S. $ 1.0 Bn<br />

Shareholding Pattern, as on Sept. 30, <strong>2010</strong><br />

Steady Growth in Revenues and Profit<br />

Consolidated Total Revenues<br />

(INR MM)<br />

80,000<br />

60,000<br />

40,000<br />

20,000<br />

0<br />

US $ MM<br />

Gross Profit<br />

12,500<br />

9,500<br />

6,500<br />

3,500<br />

500<br />

CAGR (07-10): 40%<br />

26,834 39,945<br />

57,395<br />

73,503<br />

42,742<br />

2006-07 2007-08 2008-09 2009-10 H1 <strong>2010</strong>-11<br />

(2)<br />

(3)<br />

(4)<br />

617 991 1,250<br />

(INR MM) CAGR (07-10): 62%<br />

US $ MM<br />

2,666<br />

5,845 4,768<br />

11,301<br />

6,747<br />

2006-07 2007-08 2008-09 2009-10 H1 <strong>2010</strong>-11<br />

(2) (3)<br />

(4)<br />

61 145 104<br />

150 (6)<br />

Summary Market Statistics<br />

(5)<br />

1,637<br />

252 (5)<br />

951 (6)<br />

35.41%<br />

40.83%<br />

Promoter<br />

Mutual Funds<br />

As of Oct 29, <strong>2010</strong> INR MM US$ MM (6)<br />

Share Price (INR/ US$) 249.05 5.54<br />

FII<br />

Market Capitalization 50,945 1,134<br />

19.54%<br />

Public, Banks and<br />

Financial Institutions<br />

Enterprise Value (1) 58,294 1,297<br />

4.22%<br />

Note<br />

3. Average exchange rate of US$1 = Rs.40.29 from 01-Apr-07 till 31-Mar-08<br />

Note<br />

4. Average exchange rate of US$1 = Rs.45.91 from 01-Apr-08 till 31-Mar-09<br />

1. Net Debt at INR 7,349 MM as on 31 Mar, <strong>2010</strong><br />

5. Average exchange rate of US$1 = Rs.44.90 from 01-Apr-09 till 31-Mar-10<br />

2. Average exchange rate of US$1 = Rs 43.51 from 01-Apr-06 till 31-Mar-07<br />

<strong>November</strong> <strong>2010</strong> 6. Exchange rate of US$1 = Rs. 44.935 as on 30 th Sept <strong>2010</strong><br />

Page 4

Corporate Structure<br />

Products<br />

Manufacturing Facilities<br />

WCL – An Introduction<br />

Promoters (40.83%) <strong>Welspun</strong> Corp Limited (WCL)<br />

Public and Others (59.17%)<br />

WCL – 100% WCL – 100%<br />

<strong>Welspun</strong> Pipes Inc, USA<br />

<strong>Welspun</strong> Plate and Coil Mill<br />

Division<br />

Manufacturer of state-of-art<br />

Plates and Coils<br />

<strong>Welspun</strong> Natural Resources<br />

Pvt. Ltd.<br />

Oil & Gas Exploration Activities<br />

<strong>Welspun</strong> Energy Ltd<br />

Solar & Renewable Energy<br />

100% Beneficial Interest 100% Beneficial Interest<br />

WCL – 100%<br />

<strong>Welspun</strong> Tubular LLC<br />

Manufacturer of Pipes,<br />

Coating and Double jointing<br />

<strong>Welspun</strong> Global Trade LLC<br />

<strong>Welspun</strong> Pipes Ltd.<br />

Proposed LSAW plant<br />

<strong>Welspun</strong> Infratech Ltd.<br />

Infrastructure (MSK)<br />

Pipes<br />

- Longitudinal (LSAW)<br />

- Helical / Spiral (HSAW)<br />

Plates & Coils<br />

Oil and Gas<br />

Renewable Energy &<br />

Infrastructure<br />

- Electrical (ERW)<br />

Anjar & Dahej Pipe Mills<br />

• Premier integrated set-up for manufacturing welded<br />

pipes. Installed state-of-the-art-technology and is<br />

completely geared to meet the requirements of the<br />

global industry.<br />

• The Longitudinal Pipes division (LSAW) has a<br />

capacity of 350,000 metric ton per annum.<br />

• The Spiral Pipes division (HSAW) has a capacity of<br />

550,000 metric ton per annum.<br />

• The ERW Pipes division has a capacity of 200,000<br />

metric ton per annum.<br />

• It also has Coating capabilities<br />

Little Rock , Arkansas, USA<br />

• With manufacturing facility on a 740-acre site adjacent<br />

to the Little Rock Port Authority, the $150 million<br />

facility commissioned in February 2009.<br />

• This API certified facility currently employs more than<br />

300 people and is capable of producing 350,000 tons<br />

of HSAW pipes annually for the use of the oil and gas<br />

industry.<br />

• The facility can produce Pipes from 24 to 60 inches as<br />

outer diameter; 6 mm to 25 mm as wall thickness and<br />

length of 40 -80ft.<br />

• It also has Coating and Double Jointing capabilities<br />

and is a one-stop-solution provider to <strong>Welspun</strong>'s<br />

valued customers<br />

Dammam, Saudi Arabia<br />

• Manufacturing facility of 300,000 tons of<br />

HSAW pipes annually for the use of the oil<br />

and gas industry.<br />

Plate-cum-Coil Mill<br />

• This backward integration at Anjar, Kutch,<br />

Gujarat, India has annual capacity to<br />

produce 1.5 million tones of Plate and Coil<br />

with plates (up to 4.5 meters wide, 140 mm<br />

thickness) and Coil (up to 2.8 meters wide,<br />

25 mm thickness) with strength of 120,000<br />

PSI.<br />

• This mill can cater to high end specialized<br />

product requirement of Line Pipe Industry<br />

(API grades), Shipping, Heavy construction,<br />

Bridges, Boiler plates, Wind blades etc.<br />

<strong>November</strong> <strong>2010</strong> Page 5

8<br />

Growth at Infinity<br />

Revenue<br />

Rs. 42,742 mn.<br />

H1 FY <strong>2010</strong>-11<br />

Rs. 73,503 mn. <strong>2010</strong><br />

Rs. 57,395 mn. 2009<br />

Growth<br />

- 100,000 tons HSAW Plant in Karnataka<br />

operational<br />

Investment in Middle East with HSAW<br />

capacity of 300,000 MT<br />

- 350,000 MT pipe capacity addition under<br />

implementation in India<br />

Foray into infra & pipe laying for O&G and<br />

water through MSK Projects India Ltd.<br />

350,000 tons US Spiral Mill commissioned<br />

Rs. 39,945 mn. 2008<br />

150,000 MT Spiral Mill commissioned<br />

Commissioning of Plate Mill & 43 MW Power Plant<br />

Rs. 26,834 mn.<br />

2007<br />

Anjar Facility , A Key Contributor<br />

Rs. 18,298 mn.<br />

2006<br />

Approvals from O&G majors for new facility<br />

Rs. 10,385 mn.<br />

2005<br />

New Capacity at Anjar, Gujarat for HSAW & Coating<br />

Rs. 8,277 mn.<br />

2004<br />

Merger of coating J.V. with WCL<br />

Rs. 2,565 mn.<br />

Rs. 585 mn.<br />

Rs. 180 mn.<br />

1998<br />

2000<br />

2001<br />

Pipe Coating in JV with EUPEC, Germany<br />

Dahej, Gujarat<br />

LSAW, Dahej, Gujarat<br />

HSAW, Dahej, Gujarat<br />

Incorporated<br />

1995<br />

Embarked on a Growth Journey<br />

<strong>November</strong> <strong>2010</strong> Page 6

<strong>Welspun</strong> Corp Limited: Strong Value & Growth Story<br />

1<br />

Strong Industry Fundamentals<br />

2<br />

Robust Business Fundamentals & Healthy Order Book<br />

3<br />

Global Footprint & Pre Approved with Oil & Gas Majors<br />

4<br />

Strong Management Team with Proven Execution Capabilities<br />

5<br />

Exponential Growth in Revenues & Margins<br />

<strong>November</strong> <strong>2010</strong> Page 7

1. Strong Industry Fundamentals<br />

Relatively Few Major Players<br />

• Industry is highly capital intensive with high barriers to<br />

entry<br />

• Niche markets exist which have been effectively<br />

exploited by <strong>Welspun</strong><br />

• Reliability and reputation for excellence are<br />

paramount, as pipelines are used for critical<br />

applications such as oil and gas transport<br />

• Prospects for the industry brightening with oil prices<br />

gaining strength<br />

Global Demand<br />

• Business potential of around USD 88 Bn (3) - Simdex<br />

• Replacement of the old pipelines in US<br />

• New Gas is required to replace annual decline in<br />

existing gas supplies in North America, which shall<br />

enhance demand for new pipelines<br />

• Shale Gas gradually increase its share in total gas<br />

requirement in US<br />

• Alaska Pipeline project -another boost to the demand<br />

for pipes<br />

Domestic Demand<br />

• Low pipeline penetration in India provides huge<br />

potential<br />

• Natural Gas as a source of energy is growing at a rapid<br />

pace and shall grow the demand for pipelines<br />

• Formation of the Petroleum & Natural Gas Regulatory<br />

Board (PNGRB) to give boost to trunk pipelines<br />

• City Gas Distribution set to take-off<br />

• Liquefied Natural Gas (LNG) terminals projects to<br />

enhance pipe demand<br />

• Water Infrastructure projects: A Key driver for HSAW<br />

pipes<br />

Source: Industry Sources<br />

Company<br />

<strong>Welspun</strong> is well placed, with global clients and state-ofthe-art<br />

technology, to capitalise on this opportunity<br />

International Demand Outlook till 2015<br />

Region<br />

Projects<br />

Total<br />

Length<br />

(kms)<br />

Total Length<br />

(kms)<br />

Quantity<br />

(MMT) (1)<br />

Quantity<br />

(KMT) (1)<br />

Business<br />

Potential<br />

(US$ Bn) (2)<br />

North America 244 79,758 16 19<br />

Latin America 62 34,466 7 8<br />

Europe 139 48,778 10 12<br />

Africa 68 28,213 6 7<br />

Middle East 145 49,953 10 12<br />

Asia 192 108,761 22 26<br />

Australasia 59 18,315 4 4<br />

Total 909 368,244 74 88<br />

Source: Simdex, US, Sept <strong>2010</strong> Update<br />

Domestic Market Size<br />

Business<br />

Potential<br />

(US$ Bn) (2)<br />

GAIL 6,663 1,332 1.6<br />

RGTIL 2,750 550 0.7<br />

GSPL 5,675 1,135 1.4<br />

Total 15,088 3,017 3.7<br />

Source: GAIL India Ltd Presentation Aug 10 / Company data<br />

Share of Expected Demand<br />

Until 2015<br />

Asia<br />

30%<br />

Middle East<br />

14% Africa<br />

8%<br />

Proposed pipeline of GAIL<br />

Phase I by 2011 (Under Execution)<br />

Name of Pipeline<br />

Length<br />

(Kms)<br />

Cost<br />

(Rs Cr)<br />

Add. Cap<br />

(MMSCMD)<br />

DVPL Ph -II / Vijaypur Dadri 1,115 10,830 80<br />

Dadri - Bawana - Nangal 646 2,349 31<br />

Chainsa - Jhajjhar - Hissar 349 1,259 35<br />

Sub Total 2,110 14,438 146<br />

Phase II by 2012 (Approved in 2009)<br />

Name of Pipeline<br />

Australasia<br />

5%<br />

Source: Simdex, US, July <strong>2010</strong> Update<br />

Length<br />

(Kms)<br />

North America<br />

22%<br />

Europe<br />

16%<br />

Latin America<br />

9%<br />

Cost<br />

(Rs Cr)<br />

Add. Cap<br />

(MMSCMD)<br />

Jagdishpur - Haldia 2,050 7,596 32<br />

Dabhol - Bangalore 1,389 5,014 16<br />

Kochi - Mangalore - Bangalore 1,114 3,263 16<br />

Sub Total 4,553 15,873 64<br />

Grand Total 6,663 30,311 210<br />

Source GAIL India Investor Presentation , August <strong>2010</strong><br />

Note<br />

1. Conversion rate of 200 tonnes / km 2. Conversion rate of $1,200 / ton 3. As illustrated in the adjoining tables<br />

<strong>November</strong> <strong>2010</strong> Page 8

2. Robust Business Fundamentals & Healthy Order Book<br />

Strongly Positioned<br />

• <strong>Welspun</strong> serves several marquee<br />

customers like Exxon Mobil (Golden<br />

Pass Pipeline), Kinder Morgan, Ruby<br />

(El Paso) and GAIL because of its<br />

specialized offerings<br />

• It has long term contracts with giants<br />

like TransCanada; and framework<br />

agreements with Chevron, Saudi<br />

Aramco, etc<br />

• Successfully expanded into highly<br />

competitive North and Latin America to<br />

take advantage of higher realizations<br />

Current Capacities<br />

‘000 MT pa<br />

2,200<br />

1,800<br />

1,400<br />

1,000<br />

600<br />

200<br />

(200)<br />

350<br />

350<br />

300<br />

1,000<br />

200<br />

650<br />

LSAW HSAW ERW Total<br />

Pipe<br />

Existing Capacity<br />

1,550 1,500<br />

Plate Mill<br />

Proposed Capacity<br />

Going Strength to Strength<br />

Oil & Gas Co<br />

Approval<br />

Production<br />

( '000 MT)<br />

Revenue<br />

(US$ MM)<br />

PAT<br />

(US$ MM)<br />

No. of countries<br />

FY07 FY09 FY10<br />

36 >50 >50<br />

501 717 814<br />

571 1,250 1,637<br />

36 47 136<br />

Glob<br />

al<br />

Global<br />

Global<br />

Export Market 67% 76% 77%<br />

Production Growth<br />

Export Market Gaining Dominance<br />

‘000 MT<br />

900<br />

800<br />

700<br />

600<br />

500<br />

400<br />

300<br />

200<br />

100<br />

0<br />

814<br />

670<br />

718<br />

501<br />

508<br />

377<br />

384<br />

193<br />

228<br />

FY06 FY07 FY08 FY09 FY10 H1 FY11<br />

Pipes Plates<br />

100%<br />

80% 33%<br />

60%<br />

17% 24% 23%<br />

40%<br />

67%<br />

83% 76% 77%<br />

20%<br />

0%<br />

FY07 FY08 FY09 FY10<br />

Export Domestic<br />

<strong>November</strong> <strong>2010</strong> Page 9

2. Robust Business Fundamentals & Healthy Order Book<br />

Process<br />

Process<br />

Process<br />

Raw Steel<br />

Steel Slab<br />

(API Grade)<br />

Steel Plates/<br />

Coils (API Grade)<br />

Pipes<br />

(API Grade for O&G)<br />

Selling Price (1) :<br />

Selling Price (1) :<br />

Selling Price (1) :<br />

$ 700-800 /ton.<br />

$ 900-1,000 /ton.<br />

$ 1,300-1,400/ton.<br />

Welpsun’s Value Chain (from Slabs to Pipes)<br />

Backward integration into plates provides critical value advantage<br />

Opportunity to service the high end steel category which is currently serviced through imports<br />

Note<br />

1. Indicative market prices<br />

<strong>November</strong> <strong>2010</strong> Page 10

2. Robust Business Fundamentals & Healthy Order Book<br />

Order Book<br />

Current Order Book – Geographical Distribution by Volume<br />

• Orders Booked during FY 09 - $ 1.6 bn<br />

100%<br />

85%<br />

• Orders at the beginning of FY 10 - $ 1.6 bn<br />

‣ Orders Booked during FY 10 - $ 1.3 bn<br />

‣ Orders executed during FY 10 - $ 1.6 bn<br />

• Orders at the beginning of FY 11 - $ 1.4 bn<br />

‣ Orders Booked during FY 11 (YTD) - $ 0.5 bn<br />

‣ Orders executed during H1 FY 10 - $ 0.9 bn<br />

80%<br />

60%<br />

40%<br />

20%<br />

0%<br />

Export<br />

15%<br />

Domestic<br />

• Current Orders in Hand (650 k Tonnes) - $ 1.0 bn<br />

• Raw material tied up for all outstanding orders<br />

• Majority of the shipping finalized<br />

Some of the Top Clients for Pipes<br />

Client<br />

Ruby – El Paso<br />

Enterprise<br />

Transcanada Pipe Line Limited<br />

Gas Authority of India Ltd.<br />

Indian Oil Corporation of India<br />

Saudi Aramco<br />

Country<br />

USA<br />

USA<br />

Canada<br />

India<br />

India<br />

Middle-East<br />

<strong>November</strong> <strong>2010</strong> Page 11

3. Global Footprint & Pre Approved with Oil & Gas Majors<br />

Global Market Expansion<br />

World’s largest diameter steel pipe producers (1)<br />

2007 output (million tonnes)<br />

Salzgitter/Europipe* (Germany) 1.3<br />

Saudi Arabia<br />

Iraq<br />

<strong>Welspun</strong> (India) 1.0<br />

Canada<br />

Spain<br />

Venezuela<br />

Russia<br />

JFE (Japan) 0.7<br />

Sumitomo (Japan) 0.7<br />

US (Trader Mkt.)<br />

US (Projects)<br />

Mexico<br />

Peru<br />

Bolivia<br />

Tunisia<br />

Algeria<br />

Libya<br />

Egypt<br />

Columbia<br />

Oman<br />

Qatar<br />

Indonesia<br />

Sudan<br />

China<br />

Bangladesh<br />

Malaysia<br />

Evraz** (Russia) 0.6<br />

Nippon Steel (Japan) 0.6<br />

Riva (Italy) 0.6<br />

PSL (India) 0.5<br />

JSW (India) 0.3<br />

ArcelorMittal (Luxembourg) 0.2<br />

Year 2000–2001 Year 2001–2002 Year 2002–2003 Year 2003–2004 Year 2004–2005<br />

Year 2005–2006 Year 2006–2007 Year 2007–2008 Year 2008–2009<br />

Year 2009–<br />

<strong>2010</strong><br />

Stupp (US) 0.1<br />

Tata/Corus (India/UK/Netherlands) 0.1<br />

Others*** 7.3<br />

What Sets WCL Apart From Competition<br />

• Decade Long Experience<br />

• All Solutions Under One Roof<br />

• High Capacity Equipment to Meet Future Demand<br />

• Backward Integration with In-house Plate-cum-Coil-Mill<br />

Framework Agreements<br />

• Features<br />

- Selected few companies considered for supplies that meet stringent process of qualification<br />

- Typically customers with large requirement over a period of time<br />

- Flexibility in pricing terms and continuous business<br />

• Current Framework Agreements<br />

- Chevron, Saudi Aramco (pipe purchase agreement)<br />

WCL was rated 2 nd largest Pipe Company in 2007 and has since added further capacity of 0.55 MTPA<br />

Note<br />

1. As reported by Financial Times on April 13, 2008<br />

<strong>November</strong> <strong>2010</strong> Page 12

3. Global Footprint & Pre Approved with Oil & Gas Majors<br />

AGIP<br />

BECHTEL<br />

BRITISH GAS<br />

BRITISH PETROLEUM<br />

CHINA NATIONAL PETROLEUM CORPORATION<br />

CPMEC, CHINA<br />

CHEVRON (Framework Agreement)<br />

DOW<br />

RUBY (ELPASO)<br />

EGYPTIAN GENERAL PETROLEUM CORPORATION<br />

ENTERPRISE<br />

EXXON-MOBIL (GOLDEN PASS PIPELINE)<br />

GAIL<br />

GASCO, ABUDHABI<br />

GASCO, EGYPT<br />

GAZPROM (STROYTRANSGAZ)<br />

KINDER MORGAN<br />

MOGE, MYANMER<br />

N.A.O.C. - NIGERIA<br />

NPCC, ABU DHABI<br />

NTPC<br />

ONGC<br />

PETRO CHINA<br />

PETRONAS, MALAYSIA<br />

PDO, OMAN<br />

PGN, INDONESIA<br />

QATAR PETROLEUM<br />

RELIANCE INDUSTRIES LIMITED<br />

SAIPEM, SNAM<br />

SAUDI ARAMCO (Framework Agreement)<br />

SHELL<br />

STOLT OFFSHORE – Acergy<br />

SONATRACH<br />

TOTAL<br />

TECHNIP<br />

TRANSCANADA (Long Term Contract)<br />

UNOCAL<br />

PERU LNG (HUNT OIL)<br />

VIETSOPETRO<br />

Accreditation Process<br />

A significant entry barrier<br />

Setting up plant<br />

2 years<br />

Seeking API<br />

approval<br />

1 year<br />

3 - 5 years<br />

Approval from<br />

major domestic<br />

/ international<br />

oil and gas<br />

companies<br />

2 – 3 years<br />

<strong>November</strong> <strong>2010</strong> Page 13

4. Strong Management Team with Proven Execution<br />

Capabilities<br />

Management Team<br />

Mr. B.K. Goenka is the Chairman, and the chief architect<br />

of the <strong>Welspun</strong> Group. Today, with his entrepreneurial<br />

ability and professionalism, he has built up one of the most<br />

admired business conglomerates<br />

Mr. Asim Chakraborty is Executive Director and Plant Head<br />

of the Anjar facility. A Civil Engineer from the University of<br />

Kolkata, Mr. Chakraborty has been instrumental in timely<br />

construction of various projects<br />

Mr. R.R. Mandawewala is the Managing Director. He has<br />

been a key contributor in <strong>Welspun</strong>’s journey. A Chartered<br />

Accountant by profession and with over 20 years of<br />

experience, he has cross-industry expertise varying from<br />

Textiles to SAW pipes.<br />

Mr. L. T. Hotwani is Director, Supply Chain Management<br />

of <strong>Welspun</strong> Corp Limited. With a rich experience of over 36<br />

years, Mr. Hotwani is instrumental in sourcing raw materials<br />

and managing supply chain with global players<br />

Mr. M.L. Mittal serves as Executive Director. A Chartered<br />

Accountant by profession, Mr. Mittal has been instrumental<br />

in arranging Long Term Loans and Working Capital<br />

Facilities. During his tenure, the Company has successfully<br />

funded several expansions projects.<br />

Mr. Lauri Malkki serves as CEO. Mr. Malkki has over 30<br />

years of experience within the international steel and pipes<br />

industries. Prior to <strong>Welspun</strong>, Mr. Malkki was the Managing<br />

Director, responsible for the global sales, of Europipe GmbH<br />

in Germany. For more than 20 years he was the head of the<br />

middle European operations of the Rautaruukki Group,<br />

Finland.<br />

Mr. B.R. Jaju serves as Director & CFO. A Chartered<br />

accountant by profession, member of Company Secretary (FCS),<br />

as well as a Law Degree (LL.B). He has a rich experience over<br />

30 years in finance and global M&A activities. Mr. Jaju has been<br />

awarded 3 times as Best Performing CFO in the year 2003, 2005<br />

and 2006, by the most credible nationally renowned jury.<br />

Mr. Prashant Mukherjee serves as Director of Welded<br />

Pipes. A Graduate in Science (Engineering, Mech) with over 24<br />

years experience mostly in the Oil & Gas Pipe Industry, Mr.<br />

Mukherjee has been instrumental in implementing expansion<br />

projects in the Company<br />

Mr. Akhil Jindal serves as Director of Corporate Affairs.<br />

He graduated with an Engineering Degree and thereafter an<br />

MBA from Indian Institute of Management, Bangalore. Mr.<br />

Jindal is responsible for strategic inorganic/organic<br />

initiatives within the Group and has spearheaded large fund<br />

raisings, cross border acquisitions, private equity raisings<br />

and financial closure of projects exceeding over US$ 1<br />

billion<br />

Mr. Vipul Mathur is the Director of Marketing & Sales<br />

(Pipes & Plates Division). A Science Graduate and Masters in<br />

Business Administration (MBA) in Marketing, he has a rich<br />

experience of over 16 years in the Oil & Gas Pipe Industry<br />

<strong>November</strong> <strong>2010</strong> Page 14

4. Strong Management Team with Proven Execution<br />

Capabilities<br />

LSAW Pipes<br />

ERW Pipes<br />

HSAW Pipes<br />

Coating of Pipes<br />

<strong>November</strong> <strong>2010</strong> Page 15

4. Strong Management Team with Proven Execution<br />

Capabilities<br />

Plates<br />

Plates<br />

US Plant<br />

<strong>November</strong> <strong>2010</strong> Page 16

4. Strong Management Team with Proven Execution<br />

Capabilities<br />

US Plant<br />

• Rationale for US Plant<br />

– Opportunity to locate closer to customers who were facing supply challenges<br />

– Transportation cost becomes quite large for inter-continental shipment<br />

– Existing capacity in the US was not able to serve the requirement of US clients<br />

• State of the art facility at Little Rock, Arkansas. Commissioned in Feb-09 and has obtained all API<br />

approvals<br />

• Key supplier for last 5 years in US with client list that includes Chevron, Exxon Mobil (Golden Pass<br />

Pipeline), Kinder-Morgan and Ruby (El Paso)<br />

– Framework agreement with Chevron, making <strong>Welspun</strong> one of the three global preferred vendor for<br />

next 3-5 years<br />

– Supplied pipes for world‟s deepest pipe- line in Gulf of Mexico<br />

• In H1 FY 2011 utilization levels ramp-up to 60%<br />

<strong>November</strong> <strong>2010</strong> Page 17

5. Exponential Growth in Revenues & Margins<br />

(„000 MT) (INR MM)<br />

CAGR (06-10): 22%<br />

814<br />

100,000<br />

850<br />

695<br />

641<br />

75,000<br />

650<br />

501<br />

(#) 476<br />

450 371<br />

387<br />

50,000<br />

250<br />

50<br />

# Plates<br />

(INR MM)<br />

12,000<br />

8,000<br />

4,000<br />

0<br />

US$ MM<br />

1,655<br />

CAGR (06-10): 68%<br />

(INR MM)<br />

(8)<br />

13,186<br />

CAGR (06-10): 78%<br />

6,000<br />

3,384<br />

6,555 6,348<br />

Notes<br />

1. Excluding Other Income<br />

2. Using avg. exchange rate of US$1 = Rs.44.28 from 01-Apr-05 till 31-Mar-06<br />

3. Using avg. exchange rate of US$1 = Rs.43.51 from 01-Apr-06 till 31-Mar-07<br />

4. Using avg. exchange rate of US$1 = Rs.40.29 from 01-Apr-07 till 31-Mar-08<br />

7,339<br />

2005-06 2006-07 2007-08 2008-09 2009-10 H1-<strong>2010</strong>-11<br />

(2)<br />

37 78<br />

Sales (volume) Consolidated Revenues (1)<br />

(#)<br />

154<br />

(3) (4) (5)<br />

(7)<br />

231<br />

(#)<br />

2005-06 2006-07 2007-08 2008-09 2009-10 H1-<strong>2010</strong>-11<br />

EBITDA (1)<br />

163 138<br />

(6)<br />

25,000<br />

0<br />

2005-06 2006-07 2007-08 2008-09 2009-10 H1-<strong>2010</strong>-11<br />

US$ MM 413 (2) 617 (3) 991<br />

(4) (5)<br />

1,250 1,637 (7)<br />

(9)<br />

951<br />

4,500<br />

3,000<br />

1,500<br />

0<br />

18,298<br />

614<br />

CAGR (05-10): 42%<br />

26,834<br />

1,425<br />

Profit After Tax<br />

3,408<br />

39,945<br />

2,135<br />

57,395<br />

6,104<br />

73,503<br />

PAT Margin (%)<br />

3,685<br />

2005-06 2006-07 2007-08 2008-09 2009-10 H1-<strong>2010</strong>-11<br />

(2)<br />

(3) (4) (5)<br />

294 163 (9) US$ MM 14 33 85 47 136 (7)<br />

82 (9)<br />

42,742<br />

16.0%<br />

12.0%<br />

8.0%<br />

4.0%<br />

0.0%<br />

Notes<br />

5. Using avg. exchange rate of US$1 = Rs.45.91 from 01-Apr-08 till 31-Mar-09<br />

6. Includes extraordinary items : forex provisioning of INR1,256MM, Inventory write-down of INR 385MM,<br />

ECB provisions of INR 178MM<br />

7. Using avg. exchange rate of US$1 = Rs.44.90 from 01-Apr-09 till 31-Mar-10<br />

8. Includes recovery of past forex provisioning ( in FY09) , which is reflected in better realization and cost of material<br />

9. Exchange rate of US$1 = Rs.44.935 as at 30-Sept-10<br />

<strong>November</strong> <strong>2010</strong> Page 18<br />

(6)

5. Exponential Growth in Revenues & Margins<br />

EPS (Rs./Share)(Diluted)<br />

35<br />

28<br />

CAGR (06-10): 61%<br />

28.4<br />

21<br />

18.3<br />

16.6<br />

14<br />

7<br />

4.2<br />

8.7<br />

11.5<br />

0<br />

2005-06 2006-07 2007-08 2008-09 2009-10 H1-<strong>2010</strong>-11<br />

ROCE and ROE (%)<br />

25%<br />

20%<br />

15%<br />

14.7%<br />

12.2%<br />

17.3%<br />

21.8% 21.7%<br />

19.1%<br />

11.4%<br />

R OC E<br />

13.7%<br />

R OE<br />

19.5%<br />

21.0%<br />

10%<br />

5%<br />

0%<br />

2005-06 2006-07 2007-08 2008-09 2009-10<br />

<strong>November</strong> <strong>2010</strong> Page 19

5. Exponential Growth in Revenues & Margins<br />

Consolidated Balance Sheet (Rs. Mn.) FY2009 FY<strong>2010</strong> Change<br />

Sources of Funds<br />

Shareholders' Funds<br />

Share Capital 932 1,022 89<br />

Reserves and Surplus 14,664 27,990 13,325<br />

15,597 29,011 13,414<br />

Minority Interest 0 0 (0)<br />

Foreign Currency Monetary Item Translation Difference A/c - 75 75<br />

Loan Funds -<br />

Secured Loans 26,435 18,654 (7,780)<br />

Unsecured Loans 103 6,822 6,718<br />

26,538 25,476 (1,062)<br />

Deferred Tax Liabilities (Net) 2,488 3,352 865<br />

Total 44,623 57,915 13,292<br />

<strong>November</strong> <strong>2010</strong> Page 20

5. Exponential Growth in Revenues & Margins<br />

Consolidated Balance Sheet (Rs. Mn.) FY2009 FY<strong>2010</strong> Change<br />

Application Of Funds<br />

Fixed Assets<br />

Gross Block 34,844 38,810 3,966<br />

Less:Depreciation/Amortisation/Impairment 3,847 5,889 2,042<br />

Net Block 30,996 32,921 1,924<br />

Capital Work-In-Progress 5,808 5,412 (396)<br />

36,804 38,333 1,529<br />

Investments 1,140 1,596 456<br />

Foreign Currency Monetary Item Translation Difference A/c 355 - (355)<br />

Current Assets, Loans and Advances -<br />

Income Accrued on Investments 113 13 (99)<br />

Inventories 26,113 20,322 (5,791)<br />

Sundry Debtors 4,601 8,077 3,476<br />

Cash and Bank Balances 9,470 17,028 7,558<br />

Loans and Advances 5,552 6,031 479<br />

45,848 51,471 5,623<br />

Less : Current Liabilities and Provisions -<br />

Current Liabilities 38,955 32,291 (6,663)<br />

Provisions 601 1,219 618<br />

39,555 33,510 (6,045)<br />

Net Current Assets 6,293 17,961 11,668<br />

Preliminary Expenses 0 0 (0)<br />

Deferred Revenue Expenditure 31 25 (5)<br />

Total 44,623 57,915 13,292<br />

<strong>November</strong> <strong>2010</strong> Page 21

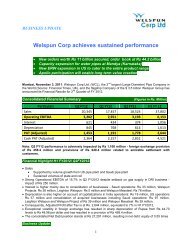

H1 & Q2 FY <strong>2010</strong>-11 Highlights<br />

Major Highlights<br />

• Sales growth of 4% on the back of:<br />

• Volume growth from US pipe plant<br />

• Higher plate and coil volumes<br />

• Lower steel prices lowers the realization. However,<br />

profitability inches up<br />

• EBITDA grows by 8%. However, operational EBITDA registers<br />

a growth of 20% as H1FY10 included realignment gain of Rs<br />

667.9 mn<br />

• Interest lower by 57% mainly on account of repayment of high<br />

cost term loans and higher interest income<br />

• Depreciation is higher in comparison to corresponding quarter<br />

on account of capitalization, commissioning of Coil Mill and<br />

consolidation of subsidiary.<br />

• Consequently, Profit after Tax at Rs. 3685 mn, reflects growth<br />

of 33% on YoY basis.<br />

• EPS grew by 13% despite dilution effect of $ 100 million equity<br />

raising by QIP (Qualified Institutional Placement) and potential<br />

dilution impact of $150 mn FCCB (Foreign Currency<br />

Convertible Bonds) conversion.<br />

• This quarter has witnessed higher sales volume and higher<br />

operational EBITDA. Interest cost is lower and depreciation is<br />

higher in line with H1 FY11 trend. Resultant PAT growth is 8%<br />

to Rs 1778 mn.<br />

Summary of H1& Q2 FY11<br />

Particulars<br />

Breakdown of Production and Sales in MT<br />

* Includes internal sales<br />

Q2<br />

FY 11<br />

Q2<br />

FY 10<br />

Growth<br />

H1<br />

FY 11<br />

H1<br />

FY 10<br />

(Rs. Million)<br />

Growth<br />

Sales 18,524 21,734 -15% 42,742 41,133 4%<br />

Reported EBITDA 3,504 3,703 -5% 7,339 6,775 8%<br />

Interest 374 610 -39% 592 1,361 -57%<br />

Depreciation 614 538 14% 1,155 1,030 12%<br />

PAT 1,778 1,651 8% 3,685 2,770 33%<br />

EPS (Rs./Share) - Diluted 8.02 8.79 -9% 16.59 14.74 13%<br />

Reported EBITDA Margin (%) 18.9% 17.0% 17.2% 16.5%<br />

PAT Margin (%) 9.6% 7.6% 8.6% 6.7%<br />

Production Volume<br />

(in MT) Q2 FY11 Q2 FY10 Growth H1 FY11 H1 FY10 Growth FY<strong>2010</strong><br />

Total Pipes<br />

Consolidated 254,337 210,469 21% 507,827 456,865 11% 813,750<br />

Plates & Coils 111,546 90,911 23% 228,356 183,163 25% 383,577<br />

Sales Volume (in MT) Q2 FY11 Q2 FY10 Growth H1 FY11 H1 FY10 Growth FY<strong>2010</strong><br />

Total Pipes<br />

Consolidated 229,688 209,023 10% 476,251 440,103 8% 815,550<br />

Plates & Coils* 128,358 113,611 13% 231,427 175,949 32% 387,224<br />

Status of Projects<br />

Capacity of Pipes is being increased to 2.2 million MTPA:<br />

• LSAW expansion of 350 K MTPA at Anjar in Q1 FY 2012.<br />

• HSAW plant of 100K MTPA at Karnataka is now fully<br />

operational.<br />

• After modifications, Saudi plant with capacity of 300K<br />

MTPA has started trial production and is likely to be on<br />

stream by the end the of 3rd quarter FY 2011.<br />

New Initiatives<br />

• Effective 16th August, <strong>2010</strong>, <strong>Welspun</strong> Infratech Ltd (a 100% subsidiary of <strong>Welspun</strong> Corp)<br />

acquired control on MSK Projects India Ltd and now holds 61.12%.<br />

• With reulatory approval processes in Saudi Arabia underway, the transaction is expected to<br />

be completed soon. This development will contribute to <strong>Welspun</strong>’s global reach not just in<br />

terms of supply, but also for production facilities.<br />

• Mr David Delie, previously CEO of Berg Steel Pipe Corporation with over 30 years of<br />

experience in the industry, was appointed as the President of <strong>Welspun</strong> Tubular LLC. His<br />

appointment will tie in with the Company’s committment to supply products from multiple<br />

sources with quality unmatched in the industry<br />

<strong>November</strong> <strong>2010</strong> Page 22

Consolidated Balance Sheet as on 30 th Sept <strong>2010</strong><br />

A<br />

Particulars As at 30.09.<strong>2010</strong><br />

Unaudited<br />

(Rs. Mn)<br />

Sources of Funds<br />

1 Shareholders Fund<br />

a Share Capital 10,22.8<br />

b Reserves and Surplus 31,469.9<br />

c Share Application Money -<br />

d Minority Interest 15,48.4<br />

2 Loan Funds 38,913.5<br />

3 Foreign Currency Monetory Item Translation Difference Account 37.7<br />

4 Deferred Tax Liabilities-Net 3,761.2<br />

B<br />

Total 76,753.5<br />

Application of Funds<br />

1 Fixed Assets 40,295.9<br />

2 Build Operate and Transfer Projects Expenditure 4,158.5<br />

3 Investments 13,065.0<br />

4 Foreign Currency Monetory Item Translation Difference Account<br />

5 Current Assets, Loans and Advances<br />

Less<br />

a Inventories 19,002.2<br />

b Sundry Debtors 12,997.8<br />

c Cash and Bank Balances 13,131.6<br />

d Loans and Advances 4,964.4<br />

4 Current Liabilities and Provisions<br />

5<br />

a Current Liabilities 29,404.4<br />

b Provisions 1,482.3<br />

Miscellaneous Expenditure 24.8<br />

Total 76,753.5<br />

<strong>November</strong> <strong>2010</strong> Page 23

Summary<br />

1 Strong Industry<br />

Fundamentals<br />

• Capital intensive, high<br />

barriers to entry<br />

• North America expected to<br />

lead demand<br />

5<br />

Exponential Growth in<br />

Revenues & Margins<br />

• Revenues have grown at a<br />

CAGR of 42% over the last<br />

five years<br />

• PAT has grown at a CAGR of<br />

78% in the same period<br />

2<br />

Robust Business<br />

Fundamentals<br />

& Healthy Order Book<br />

• Strong volume growth<br />

• Order Book in excess of US$<br />

1.0 Bn<br />

• Capacities of global size<br />

• Comprehensive product mix<br />

4 3 Global Footprint & Pre<br />

Strong Management Team<br />

with Proven Execution<br />

Capabilities<br />

• Recognized by the FT as the<br />

second largest steel pipe<br />

producer in the world in 2007<br />

• First Indian company to supply<br />

pipes for offshore projects in US<br />

Approved with O&G Majors<br />

• Presence across more than 25<br />

countries<br />

• Pre-approved with more than<br />

50 O&G Majors<br />

<strong>November</strong> <strong>2010</strong> Page 24

<strong>Welspun</strong> on the Path of Global Leadership<br />

Scale Leadership<br />

Scale of operations through large economic plants across the globe<br />

Cost Leadership<br />

Produce world class products at the least cost and maintain competitive edge<br />

Technology<br />

Leadership<br />

Adopt and innovate cutting-edge technology to satisfy stringent<br />

requirements of customers<br />

Quality Leadership<br />

Consistent focus on quality at all levels; be the best in delighting customers<br />

Process Leadership<br />

Most efficient and effective processes to achieve optimal utilizations<br />

People Leadership<br />

Best in class people : Produce extraordinary results<br />

Global Leadership Serve Globally, Act Locally<br />

<strong>November</strong> <strong>2010</strong> Page 25

Key questions on recent updates<br />

What is <strong>Welspun</strong>'s exposure to current civil proceedings?<br />

During the previous year one of the customer reported defect in the pipes supplied<br />

alleging grade of steel used did not meet the specifications, the company replaced the<br />

defective pipes and also provided for the expected loss on this account. During the year<br />

the said customer initiated legal action against the company in the United States of<br />

America claiming loss / damages of $ 66 million on account of defects in the pipes<br />

supplied, consequently the company also initiated legal action against the steel supplier<br />

claiming corresponding loss / damages it may suffer on account of this claim of the<br />

customer. Hence the company does not expect any liability on account of the claim<br />

against it.<br />

<strong>November</strong> <strong>2010</strong> Page 26

Thank You<br />

For further details, please contact:<br />

Akhil Jindal<br />

Director - Corporate Affairs<br />

Tel.: +91- 22- 6613 5721<br />

Mob.: +91- 98- 7029 6187<br />

Email: akhil_jindal@welspun.com<br />

Navin Agarwal<br />

AVP - Corporate Affairs<br />

Tel.: +91- 22- 6613 5734<br />

Mob.: +91- 98- 7000 9224<br />

Email: navin_agarwal@welspun.com<br />

Company Website: http://www.welspuncorp.com<br />

<strong>November</strong> <strong>2010</strong> Page 27