Ali Pejman, CA - Institute of Chartered Accountants of BC

Ali Pejman, CA - Institute of Chartered Accountants of BC

Ali Pejman, CA - Institute of Chartered Accountants of BC

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

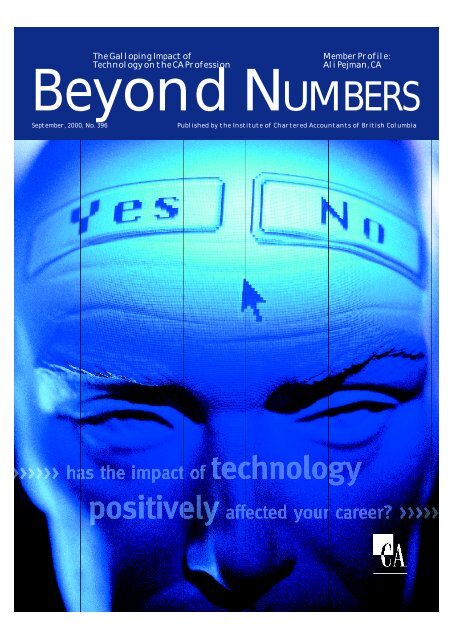

The Galloping Impact <strong>of</strong><br />

Technology on the <strong>CA</strong> Pr<strong>of</strong>ession<br />

Member Pr<strong>of</strong>ile:<br />

<strong>Ali</strong> <strong>Pejman</strong>, <strong>CA</strong><br />

Beyond NUMBERS<br />

September, 2000, No. 396<br />

Published by the <strong>Institute</strong> <strong>of</strong> <strong>Chartered</strong> <strong>Accountants</strong> <strong>of</strong> British Columbia

Beyond Numbers<br />

Contents<br />

September 2000, No. 396<br />

Published 10 times annually by the <strong>Institute</strong> <strong>of</strong><br />

<strong>Chartered</strong> <strong>Accountants</strong> <strong>of</strong> British Columbia.<br />

Director <strong>of</strong> External Affairs<br />

Lesley MacGregor<br />

Layout & Design<br />

Tammy Carter<br />

Advertising<br />

Advertising In Print<br />

Telephone: (604) 681-1811<br />

Facsimile: (604) 681-0456<br />

Cover: Realm Communications Inc.<br />

<strong>Institute</strong> Council<br />

Chuck Chandler, F<strong>CA</strong><br />

Frank Barr, <strong>CA</strong><br />

Robin Elliott, F<strong>CA</strong><br />

Terry Jonat, <strong>CA</strong><br />

Jack Arnold, <strong>CA</strong><br />

Robert Burrows<br />

David Chucko, <strong>CA</strong><br />

Leslie Cliff<br />

Johan de Rooy, F<strong>CA</strong><br />

Mark Dickie, <strong>CA</strong><br />

Brian Downie, <strong>CA</strong><br />

Chief Executive Officer<br />

Richard Rees, <strong>CA</strong><br />

Council Secretary<br />

Eleanor Joughin<br />

President<br />

1st Vice President<br />

2nd Vice President<br />

Treasurer<br />

Beyond Numbers is printed in British Columbia<br />

and mailed 10 times annually to more than 8,000<br />

chartered accountants and 900 <strong>CA</strong> students in public<br />

practice, industry, education and government service<br />

throughout B.C., Canada and other countries.<br />

Beyond Numbers’ editorial and business <strong>of</strong>fices are<br />

at 6th floor, 1133 Melville St., Vancouver, B.C. V6E 4E5<br />

Phone: (604) 681-3264<br />

Toll-free in <strong>BC</strong>: 1-800-663-2677<br />

Fax: (604) 681-1523<br />

Internet: www.ica.bc.ca<br />

Opinions expressed are not necessarily<br />

endorsed by the <strong>Institute</strong>.<br />

Beyond Numbers supports the <strong>CA</strong> pr<strong>of</strong>ession in B.C.<br />

by sharing news from the <strong>Institute</strong> and news about<br />

members, by sharing viewpoints on issues <strong>of</strong> specific<br />

interest to members, and by promoting member<br />

involvement in <strong>Institute</strong> activities.<br />

Publication Agreement Number: 1475940<br />

Odd Eidsvik, F<strong>CA</strong><br />

Ross Fraser<br />

Paul Grehan, <strong>CA</strong><br />

Janet Heino, <strong>CA</strong><br />

James Mills, <strong>CA</strong><br />

Douglas Murphy, <strong>CA</strong><br />

Margaret Parkinson, <strong>CA</strong><br />

Features<br />

6 Cover Story:<br />

The Galloping Impact <strong>of</strong><br />

Technology on the <strong>CA</strong><br />

Pr<strong>of</strong>ession<br />

12 Firms Like Wolrige Mahon<br />

Get a Head Start on<br />

Attracting Top Talent<br />

13 Coming This Month -<br />

<strong>BC</strong> Check Up<br />

14 High-Tech Leader Launches<br />

<strong>BC</strong> Business Summit 2000<br />

18 Under New Management<br />

20 Procedures For Election<br />

<strong>of</strong> Fellows<br />

23 Registrar Retires<br />

After 26 Years<br />

24 Communications Director<br />

Moves to IC<strong>BC</strong><br />

Sections<br />

4 For the Pr<strong>of</strong>ession<br />

5 President’s Notes<br />

22 Member Pr<strong>of</strong>ile:<br />

<strong>Ali</strong> <strong>Pejman</strong>, <strong>CA</strong><br />

25 Tax Traps & Tips<br />

27 Employment Opportunities<br />

29 At Your Service<br />

30 Classifieds<br />

30 Notes on Members<br />

Our Mission<br />

The mission <strong>of</strong> the <strong>Institute</strong> <strong>of</strong> <strong>Chartered</strong><br />

<strong>Accountants</strong> <strong>of</strong> British Columbia is to protect and<br />

serve the public, our members and students by<br />

providing exceptional education, regulation and<br />

member services programs so that chartered<br />

accountants may provide the highest quality <strong>of</strong><br />

pr<strong>of</strong>essional service.

For the Pr<strong>of</strong>ession<br />

By Richard Rees, <strong>CA</strong><br />

CEO, <strong>Institute</strong> <strong>of</strong> <strong>Chartered</strong> <strong>Accountants</strong> <strong>of</strong> <strong>BC</strong><br />

This issue <strong>of</strong> Beyond Numbers<br />

focuses on the impact changing<br />

technology is having on the<br />

<strong>CA</strong> pr<strong>of</strong>ession. It is also changing the way<br />

we work at the <strong>Institute</strong>. On the one hand,<br />

our environment is becoming increasing<br />

complex and expensive – making it<br />

increasingly difficult to deliver relevant<br />

services at a reasonable cost. On the other<br />

hand, new technology is creating opportunities<br />

for the <strong>Institute</strong> to rationalize and<br />

deliver programs and services in a more<br />

economical manner. In B.C., we are doing<br />

everything we can to harness the opportunities<br />

presented by technology to maximize<br />

member value.<br />

The B.C. <strong>Institute</strong> has a long track<br />

record <strong>of</strong> taking advantage <strong>of</strong> economies <strong>of</strong><br />

scale. We have been keen participants in the<br />

move to a consistent database program that<br />

allows sharing <strong>of</strong> information<br />

interprovincially and with CI<strong>CA</strong>. We have<br />

also joined with other western provinces to<br />

economize on the delivery <strong>of</strong> education<br />

with the new <strong>CA</strong> School <strong>of</strong> Business.<br />

These moves to greater coordination<br />

have been strongly endorsed by Council –<br />

and they await with interest further<br />

opportunities to collaborate to keep costs<br />

down and enhance service to members.<br />

Their desire for increased cooperation is<br />

being aided by a new national initiative<br />

focussing on member value maximization.<br />

The first step in this process is the<br />

commissioning <strong>of</strong> an independent study to<br />

review the plans and budgets <strong>of</strong> all<br />

<strong>Institute</strong>s in Canada to identify areas for<br />

enhanced cooperation and coordination<br />

through delivery <strong>of</strong> common services. The<br />

study is rooted in the evolving governance<br />

model in Canada, which promotes greater<br />

formal and informal information sharing,<br />

and takes advantage <strong>of</strong> emerging Internetbased<br />

delivery options.<br />

The project is being managed by a<br />

committee composed <strong>of</strong> four Presidents,<br />

each representing a region <strong>of</strong> Canada, and by<br />

representatives <strong>of</strong> the CI<strong>CA</strong> and provincial<br />

<strong>Institute</strong> staff. I am pleased to tell you that I<br />

am the provincial <strong>Institute</strong> representative.<br />

The project is just getting underway,<br />

but will include:<br />

• Identifying common activities,<br />

priorities, and processes;<br />

• Comparing and evaluating resource<br />

requirements;<br />

• Identifying opportunities to improve<br />

efficiency and effectiveness; and<br />

• Identifying alternative service delivery<br />

approaches.<br />

The results <strong>of</strong> the project will help to<br />

increase efficiency and will address<br />

changing member needs as firms globalize,<br />

members and students become<br />

more mobile, and the need for instant<br />

information becomes more the norm.<br />

It is never easy to harmonize 13<br />

independent entities – particularly when<br />

they <strong>of</strong>fer different services, operate on<br />

varied systems, and have diverse regulatory<br />

environments. However, there are<br />

substantial commonalities between the<br />

<strong>Institute</strong>s and a strong resolve from the<br />

volunteer leadership to pursue common<br />

solutions. B.C. is playing a strong role in<br />

promoting this cooperative spirit and<br />

ensuring that it results in bottom-line<br />

savings for members in the province.<br />

I hope to report significant progress in<br />

maximizing your member value in the<br />

months ahead.<br />

4 Beyond Numbers / September 2000

President’s Notes<br />

By Chuck Chandler, F<strong>CA</strong>,<br />

President, <strong>Chartered</strong> <strong>Accountants</strong> <strong>of</strong> <strong>BC</strong><br />

“Change has considerable psychological<br />

impact on the human mind. To the<br />

fearful it is threatening because it means<br />

that things may get worse. To the hopeful<br />

it is encouraging because things may get<br />

better. To the confident it is inspiring<br />

because the challenge exists to make<br />

things better. – K. Whitney as quoted by<br />

the Wall Street Journal.<br />

Globalization – It’s as easy as XYZ<br />

It’s amazing how much business has<br />

been impacted by technology, especially<br />

the Internet, over the past few years. And<br />

the pace <strong>of</strong> change is increasing still. A<br />

few years ago I would have thought that<br />

global business meant big business.<br />

Today, we are all very much connected to<br />

events and transactions around the world.<br />

As <strong>CA</strong>s, we’re in the front lines <strong>of</strong> this<br />

change, whether it’s preparing financial<br />

statements that include US GAAP for the<br />

burgeoning US equity markets, or<br />

establishing e-commerce for global<br />

business transactions. In this issue <strong>of</strong><br />

Beyond Numbers, you will find pr<strong>of</strong>iles <strong>of</strong><br />

how technology has changed the life <strong>of</strong><br />

eight <strong>CA</strong>s in B.C. Even in my own firm <strong>of</strong> 22<br />

people, we have 2 CPAs who have<br />

attempted and passed the reciprocity<br />

exams. A third has headed <strong>of</strong>f to<br />

California to pursue her dreams — part <strong>of</strong><br />

the “brain drain” that <strong>of</strong>ficially doesn’t<br />

exist.<br />

In keeping with these real life trends,<br />

the CI<strong>CA</strong> is working with other national<br />

accounting organizations to develop a<br />

global pr<strong>of</strong>essional business designation<br />

(as yet unnamed – “XYZ” for now). The<br />

designation is intended to reflect all the<br />

services that members currently provide<br />

and all <strong>of</strong> the high-opportunity work that<br />

the pr<strong>of</strong>ession identified in the Vision<br />

process. Benefits are intended to accrue to<br />

designation holders, employers, and<br />

buyers <strong>of</strong> services. Negotiations on the<br />

specifics <strong>of</strong> the designation and entrance<br />

requirements are ongoing. The CI<strong>CA</strong> is<br />

keeping the <strong>BC</strong> <strong>Institute</strong> abreast <strong>of</strong> the<br />

changes, and we’ll keep our members<br />

informed as events unfold.<br />

Creating the Vision <strong>CA</strong> – Taking on<br />

the Challenges <strong>of</strong> Business in the<br />

New Millennium<br />

At our last full Council meeting in<br />

May, I asked our Council members what<br />

was the most pressing issue facing our<br />

pr<strong>of</strong>ession. Virtually everyone put<br />

attractiveness <strong>of</strong> the pr<strong>of</strong>ession at or<br />

near the top <strong>of</strong> the list. A survey <strong>of</strong><br />

recent literature and statistics points us<br />

in the same direction. One major<br />

executive recruiter commented that she<br />

“fears the <strong>CA</strong> firms are losing out on<br />

recruiting young people out <strong>of</strong> university<br />

because so many do not want to<br />

spend their entire articling period<br />

auditing.” Interestingly, 80% <strong>of</strong> the<br />

searches for senior personnel at this<br />

recruiting firm are for <strong>CA</strong>s because <strong>of</strong><br />

their perceived integrity and the credibility.<br />

The next issue <strong>of</strong> Beyond Numbers<br />

will be dedicated to young <strong>CA</strong>s – the<br />

challenges they face in becoming <strong>CA</strong>s, the<br />

opportunities available to them when they<br />

have their designation, and the ways the<br />

B.C. <strong>Institute</strong> is responding to these issues.<br />

The CI<strong>CA</strong>’s 1996 Vision Report recognized<br />

the issues, and the need for business<br />

advisors who are forward thinking and<br />

strategically motivated in a global<br />

economy. The Education Re-Engineering<br />

Task Force built recommended a framework<br />

for competency based learning. That<br />

would strengthen the link between <strong>CA</strong><br />

formal education and the candidate’s on<br />

the job performance. A “core plus focus”<br />

model was recommended to accommodate<br />

the expanded training in other areas such<br />

as IT and finance.<br />

Together with our fellow western<br />

provincial and territorial <strong>Institute</strong>s, the<br />

<strong>BC</strong> <strong>Institute</strong> has embraced the ERTF<br />

model and this Fall will be recruiting<br />

students to our new <strong>CA</strong> School <strong>of</strong> Business.<br />

This year, when recruiters speak to<br />

students, they can <strong>of</strong>fer them a pr<strong>of</strong>essional<br />

career that provides choice, the<br />

ability to select a focus or specialization<br />

down the road, and even the ability to<br />

complete part <strong>of</strong> their training outside <strong>of</strong><br />

public practice.<br />

Students who may have been<br />

leaning towards an MBA or a finance<br />

degree are now going to have to take a<br />

hard look at the <strong>CA</strong> option as being the<br />

best business degree available. Will it be<br />

just as tough to get a <strong>CA</strong>? You bet. But<br />

the rewards for people wishing to enter<br />

our pr<strong>of</strong>ession will be far more favourable.<br />

I invite you to check out the new<br />

<strong>CA</strong>SB website at www.calearn.com.<br />

My thanks and best wishes to past<br />

president John Dawson F<strong>CA</strong> (chair <strong>of</strong><br />

<strong>CA</strong>SB board) and Dr. Don Carter F<strong>CA</strong><br />

who, together with <strong>CA</strong>SB board member<br />

Tom Kirstein, <strong>CA</strong> and new board<br />

member Roger Wolff (Dean <strong>of</strong> Business<br />

at Uvic) are leading the way as <strong>BC</strong>’s<br />

representatives on <strong>CA</strong>SB.<br />

More on Your New Council.<br />

In my last column I welcomed three <strong>of</strong><br />

our four new council members. I neglected<br />

to welcome Margaret Parkinson, <strong>CA</strong>. My<br />

apologies! Margaret is a long-time volunteer<br />

with the <strong>Institute</strong> and I’m looking<br />

forward to working with her on Council.<br />

My thanks to “the big guy”<br />

As you saw in last month’s Beyond<br />

Numbers, the <strong>Institute</strong>’s former Director<br />

<strong>of</strong> Ethics, Brian Gardiner, <strong>CA</strong> has hung up<br />

his <strong>Institute</strong> skates to pursue exciting<br />

opportunities in the field <strong>of</strong> governance<br />

and advocacy with HLB Cinnamon Jang<br />

Willoughby. Welcome back to<br />

timesheets there, big guy. You’ve left a<br />

legacy <strong>of</strong> hard work that has kept our<br />

pr<strong>of</strong>ession in <strong>BC</strong> ahead <strong>of</strong> the rest in<br />

public perceptions <strong>of</strong> maintaining high<br />

standards <strong>of</strong> ethical and pr<strong>of</strong>essional<br />

conduct. Best wishes to you.<br />

I encourage you to e-mail<br />

president@ica.bc.ca with your comments<br />

at any time.<br />

September 2000 / Beyond Numbers 5

Cover Story<br />

The Galloping Impact<br />

<strong>of</strong> Technology on the<br />

<strong>CA</strong> Pr<strong>of</strong>ession<br />

By Deborah Folka, APR<br />

We wanted to know how <strong>CA</strong>s are dealing with the<br />

impact <strong>of</strong> technology on the pr<strong>of</strong>ession, so we<br />

asked eight members — four from public<br />

practice and four from industry — to give us their opinions on<br />

how technology has affected their individual careers, their<br />

clients or employers and what they think <strong>of</strong> the global impact<br />

<strong>of</strong> technology on the pr<strong>of</strong>ession.<br />

6 Beyond Numbers / September 2000

September 2000 / Beyond Numbers 7

As the technology partner with the<br />

Vancouver <strong>CA</strong> firm <strong>of</strong> Nordahl<br />

Craig Cummings & Gares, <strong>Chartered</strong><br />

<strong>Accountants</strong>, Gordon Baldwin, <strong>CA</strong>, is<br />

acutely aware <strong>of</strong> the effect <strong>of</strong> technology.<br />

“I’m totally wired at<br />

the <strong>of</strong>fice, using<br />

Outlook extensively<br />

and I have a computer<br />

at home where I<br />

mostly rely on<br />

hotmail, but so far no<br />

Palm Pilot device,” he<br />

says. “A few years<br />

ago, when I set up<br />

shop as a sole practitioner, it was technology<br />

that allowed me to get started with<br />

little overhead. You couldn’t have done<br />

that long ago.”<br />

Baldwin says clients’ use <strong>of</strong> technology<br />

is “a mixed bag.”<br />

“Sure, everyone has computers now,<br />

but so many <strong>of</strong> them in small to mediumsized<br />

businesses don’t have the capabilities<br />

to fix their technology problems; they<br />

don’t have an IT department,” he explains.<br />

“So <strong>of</strong>ten they don’t get the full advantage<br />

<strong>of</strong> the technology they’ve purchased. But<br />

this is where our expertise has been<br />

developed because they naturally turn to<br />

our firm for s<strong>of</strong>tware recommendations or<br />

solutions to their technology issues.”<br />

Baldwin says clients are all moving in<br />

the same direction, though some are<br />

slower than others and, at the other end <strong>of</strong><br />

the spectrum, some are keen to get into e-<br />

commerce.<br />

“Certainly, in doing our tax work and<br />

meaningful reports for clients, technology<br />

has helped immensely,” he points out. “I’ve<br />

even been able to do custom installation <strong>of</strong><br />

a technology system developed for a<br />

company in the fishing industry which<br />

was just perfect for them.<br />

“And, as far as the <strong>CA</strong> pr<strong>of</strong>ession is<br />

concerned, just look at the rapid advances in<br />

tax s<strong>of</strong>tware,” he says. “You can do a T-1 in<br />

15 minutes while the client sits in front <strong>of</strong><br />

you. But, just like with our clients, not<br />

every firm is taking advantage <strong>of</strong> the<br />

technology available. Some are resistant to<br />

change and some are intimidated by what<br />

they perceive to be a steep learning curve.<br />

“The Internet <strong>of</strong>fers lots <strong>of</strong> great<br />

opportunities for <strong>CA</strong> firms,” he points out.<br />

“It’s hard to get and keep good staff today so<br />

our firm is making it as easy as possible for<br />

staff to have remote computer access. When<br />

family issues come up or if someone wants<br />

to tele-commute, we have the capability<br />

without any work or time being lost.”<br />

A <strong>CA</strong> since 1979, Baldwin has been in<br />

both public practice and industry. He says<br />

he thinks keeping up on the latest technology<br />

will help <strong>CA</strong>s stay competitive and be<br />

able to generate good incomes. But he<br />

cautions “the paper-based world is not<br />

dead yet and you have to be careful, even<br />

with the most sophisticated s<strong>of</strong>tware<br />

programs that your information going in<br />

is accurate or you’re making decisions<br />

based on bad information.”<br />

In the investment dealer industry<br />

that Martin Burian, <strong>CA</strong>, CBV deals<br />

in, technology has had a huge impact.<br />

Burian, Vice President <strong>of</strong> Corporate<br />

Finance at Canaccord Capital Corporation<br />

and a <strong>CA</strong> since 1990, says he has seen the<br />

greatest changes in the last five years.<br />

“Our dependence on computers, e-<br />

mail and information technology generally<br />

has increased tremendously,” he says.<br />

“We’d find it tough to function without it<br />

because <strong>of</strong> the ease <strong>of</strong> sharing documents<br />

and transferring information. Things are<br />

done so much faster, <strong>of</strong>ten through several<br />

time zones, the best technology is essential<br />

to our business.”<br />

Burian is “totally plugged in” at the<br />

<strong>of</strong>fice, but away from there only carries a<br />

cellular phone which he uses judiciously.<br />

“When I’m at a client’s, I want to be<br />

totally focused and I can’t be distracted by<br />

cell calls or a laptop rattling <strong>of</strong>f e-mail,” he<br />

points out. “In our industry, the Internet<br />

has leveled the information access playing<br />

field and now anyone can get a stock<br />

quote or financial statements or other<br />

financial information in real time for free.<br />

So we have to work harder to provide<br />

relevant information to clients.”<br />

Burian says the costs <strong>of</strong> accessing<br />

information are still here and, in fact, are<br />

increasing from companies that disseminate<br />

well-organized, relevant information.<br />

“On a global scale, we see and finance a<br />

lot <strong>of</strong> technology companies and I believe<br />

that sector will continue to have a big<br />

impact on all <strong>of</strong> us. Businesses <strong>of</strong> all kinds —<br />

and the <strong>CA</strong>s associated with those businesses<br />

— will have to acknowledge it and<br />

use it or they won’t survive,” Burian says.<br />

Like Burian, Mark Brown, <strong>CA</strong>, is in<br />

the venture capital business with<br />

Pacific Opportunity Company Ltd. in<br />

Vancouver and, like his colleague, has the<br />

opportunity to see many emerging<br />

businesses.<br />

“<strong>CA</strong>s are expected to know a lot about<br />

computer systems and technology in<br />

general and we try to<br />

keep ahead <strong>of</strong> the pack in<br />

our business because<br />

having that knowledge<br />

helps us assess companies<br />

we’re trying to assist<br />

with capital,” he explains.<br />

“And the speed <strong>of</strong><br />

technology has an<br />

impact on how you operate as well. Communications<br />

are a marvel and e-mail is great,<br />

but then the client expectations rise as well.<br />

They expect you to speed-read the 100-page<br />

document they just e-mailed when it’s really<br />

more important to take extra time to make<br />

sure that the contents are well thought out.”<br />

Brown cautioned against <strong>CA</strong>s becoming<br />

“total techies”.<br />

“People are hiring us for the business<br />

principles we understand, not to be a<br />

technology expert,” he points out. “Of<br />

course we need to be in the forefront in<br />

knowledge <strong>of</strong> what’s out there, but it’s our<br />

expertise in running a business that adds<br />

value to the equation. At Pacific Opportunity,<br />

we rely on an external team <strong>of</strong><br />

experts to assess “black box” technologies.”<br />

Brown says he is “totally wired...or<br />

totally wireless” depending on your<br />

perspective.<br />

“I carry my whole <strong>of</strong>fice with me;<br />

8 Beyond Numbers / September 2000

laptop, cell phone, the whole thing,” he<br />

says. “And this all helps put deals together<br />

more quickly and allows me to work on<br />

several projects at the same time. The<br />

Internet is also a valuable tool for us,<br />

especially when travelling abroad. Of<br />

course, these same technologies were<br />

supposed to make our lives easier when<br />

we really just get more done in the same<br />

amount <strong>of</strong> time!”<br />

Brown, who has been with Pacific<br />

Opportunity for four years, estimates that<br />

technology has doubled the speed <strong>of</strong> doing<br />

business in the past year alone.<br />

“With e-mail and cell phones, we put<br />

together public <strong>of</strong>ferings in three months<br />

that used to take six months to do and<br />

acquisitions in six months that would<br />

previously have taken a year,” he says.<br />

He acknowledges that the negative<br />

side <strong>of</strong> rapid technology is the pressure <strong>of</strong><br />

increased client expectations, as well as<br />

the increased concerns about privacy,<br />

confidentiality and security.<br />

“<strong>CA</strong>s just need to stay on top <strong>of</strong> it<br />

and be aware <strong>of</strong> what’s going on out<br />

there,” he says.<br />

Allan May, <strong>CA</strong>, Director <strong>of</strong> Finance<br />

for Resort Communications<br />

Group, has been a <strong>CA</strong> since 1991 and<br />

articled with Deloitte & Touche LLP,<br />

<strong>Chartered</strong> <strong>Accountants</strong>. He is, by his own<br />

admission, the “totally wireless man”.<br />

“Cell phone, laptop, personal digital<br />

assistant, voice mail, e-mail at home and<br />

the <strong>of</strong>fice and with all those great portable<br />

devices, I am always in touch,” May says.<br />

But he acknowledges not everyone is<br />

operating the same way.<br />

“It still all depends on the client,” he<br />

points out. “Some are on the leading edge<br />

and have taken full advantage <strong>of</strong> technology<br />

to minimize the paper flow and<br />

maximize efficiencies in communications<br />

and financial reporting and operations.<br />

Others haven’t had this success and mostly<br />

it’s because <strong>of</strong> a lack <strong>of</strong> long-term planning.<br />

They don’t fully understand what exactly<br />

the technology they’re purchasing can<br />

do...so it doesn’t really work out for them as<br />

well as it could. They don’t go forward with<br />

a ‘technological road map’, as it were.”<br />

On a global scale, May says <strong>CA</strong>s should<br />

be aware <strong>of</strong> the opportunities technology is<br />

providing beyond our local environments.<br />

“Not many <strong>CA</strong>s are providing services<br />

on a global scale yet and I think in some<br />

cases it’s the clients holding them back —<br />

they continue to want paper-based<br />

comfort,” he says. “Many high-tech firms<br />

are doing paper-free communications <strong>of</strong><br />

their annual reports and other financial<br />

information, but most <strong>of</strong> the bricks and<br />

mortar clients are not there yet.”<br />

May says he has seen incredible<br />

change in technology since he began his<br />

articling in 1988.<br />

“But for many small to medium-sized<br />

businesses, they can’t totally accept the<br />

new world technology has created,” he<br />

points out. “For example, they want to<br />

keep their computers as long as possible to<br />

realize the depreciation benefits under the<br />

tax rules, so many <strong>of</strong> them are keeping<br />

obsolete machines too long and holding<br />

back their companies from the newer<br />

technologies. I would suggest that the tax<br />

rules around write-<strong>of</strong>fs be updated so<br />

clients can purchase new computers, stay<br />

competitive and get the advantage <strong>of</strong><br />

write-<strong>of</strong>fs for re-investing.”<br />

At Deloitte & Touche LLP’s Vancouver<br />

<strong>of</strong>fice, Steve Figner, <strong>CA</strong>, sports<br />

the title Senior Manager in Enterprise Risk<br />

Services and focuses his work exclusively<br />

on technology risk.<br />

“Personally, I have seen pr<strong>of</strong>ound<br />

changes in technology and how that has<br />

affected the way we do business,” Figner<br />

says. “When I began articling in 1994, we<br />

were still talking about mainframe environments<br />

and today, in my department, we<br />

all have cell phones we send e-mail from,<br />

state-<strong>of</strong>-the-art laptops, personal digital<br />

assistants and soon we’ll have the ability to<br />

access network resources from our home<br />

computers. I’ve witnessed the evolution <strong>of</strong><br />

the Internet, e-business<br />

and now we’re in the<br />

middle <strong>of</strong> a wave <strong>of</strong><br />

enterprise resource<br />

planning for the large,<br />

integrated s<strong>of</strong>tware<br />

programs.”<br />

In the big firm<br />

environment, Figner says they see larger<br />

clients with more sophisticated technology<br />

needs and they have geared up to<br />

service those needs.<br />

“Technology has introduced tremendous<br />

opportunity into the big business<br />

environment, but we also see how it has<br />

introduced risk as well,” Figner points out.<br />

“The integrity <strong>of</strong> the data, security issues,<br />

confidentiality, privacy and so on. It’s only<br />

going to get riskier as more and more<br />

companies move into e-business.”<br />

Figner says he is thoroughly impressed<br />

that the Canadian <strong>Institute</strong> <strong>of</strong> <strong>Chartered</strong><br />

<strong>Accountants</strong> and the Vision Task Force<br />

September 2000 / Beyond Numbers 9

grasped the importance <strong>of</strong> technological<br />

change for the pr<strong>of</strong>ession and have made it<br />

an integral part <strong>of</strong> the <strong>CA</strong> pr<strong>of</strong>ession.<br />

“I’m glad to see the subject takes up a<br />

lot <strong>of</strong> space on a regular basis in <strong>CA</strong><br />

Magazine,” he says. “For us in public<br />

practice, <strong>of</strong> course it’s important to keep<br />

up-to-date, but it’s also critical for <strong>CA</strong>s who<br />

are CFOs or Controllers and not surrounded<br />

by other <strong>CA</strong>s.<br />

They need the pr<strong>of</strong>ession helping them<br />

understand how technology is continuing to<br />

impact their environments.”<br />

Figner also suggests that while the<br />

big firms have plunged into looking at the<br />

risks and problems associated with<br />

technology, it’s harder for the small or sole<br />

practitioners to do so and thus the <strong>Institute</strong><br />

has a role to play there.<br />

“I think we need mentoring and<br />

intensive pr<strong>of</strong>essional development<br />

around technology and the related issues,”<br />

Figner says. “These are important programs<br />

for all <strong>CA</strong>s.<br />

“<strong>CA</strong>s have always been about information<br />

and integrity,” he says. “Now these<br />

areas have collided with the surge in<br />

information technology and we must<br />

remain on top <strong>of</strong> it.”<br />

Derek Belyea, <strong>CA</strong>, MBA is with<br />

GNA Consulting Group in<br />

Vancouver and, for him, technology has<br />

meant “working harder than ever before.”<br />

“Overall, I see my cycle times for<br />

responding to client requests dropping,”<br />

Belyea says. “I notice that as clients adapt to<br />

new technologies I can add more value to<br />

their businesses with less wasted effort.<br />

That means a lower cost to the client, even<br />

though charge-out rates have been rising.<br />

But I am also juggling more projects at the<br />

same time because the technology allows it.”<br />

Belyea acknowledges that a negative<br />

side effect <strong>of</strong> the changes in technology is<br />

a higher stress level.<br />

“Everyone feels compelled to push<br />

harder and the technology continuously<br />

raises expectation levels,” he points out.<br />

Belyea observes that for most <strong>of</strong> his<br />

clients, technology investments are bigger<br />

than ever and more critical to their<br />

business successes.<br />

“The range <strong>of</strong> choices that is <strong>of</strong>fered is<br />

dizzying and changes daily,” he explains.<br />

“Clients are spending tons <strong>of</strong> money on<br />

technology — Internet, intranets, supply<br />

chain, ERP, CRM, data warehouses and on<br />

and on. They know they have to — just to<br />

keep up — but for many there is an uneasy<br />

feeling that they are not getting it quite<br />

right and not doing it fast enough.<br />

“Failure to get technology projects to<br />

succeed used to be a private matter,”<br />

Belyea continues. “Today everyone is more<br />

savvy about what can be done with<br />

technology and now it can be obvious to<br />

customers, suppliers and competitors that<br />

you are not delivering on technology.<br />

Customers can be fickle if you are not<br />

meeting their expectations and competitors<br />

will pounce when they see an opening.<br />

The businesses that succeed know<br />

how to make technology a competitive<br />

tool. They do this to reduce costs, shorten<br />

cycle times and improve quality. In many<br />

cases, it can mean a complete re-definition<br />

<strong>of</strong> the business.”<br />

Belyea points out that for many<br />

companies the CFO is <strong>of</strong>ten a <strong>CA</strong> with<br />

direct responsibility for technology<br />

investments.<br />

“The CFO needs to understand the<br />

opportunities for technology investments,”<br />

he explains. “He or she also needs to know<br />

how to drive the necessary change into the<br />

business, how to do it on time and within<br />

budget. This can be a tall order with lots <strong>of</strong><br />

risk.” Belyea suggests that the baseline<br />

computer skills most <strong>CA</strong>s have acquired<br />

over the last 20 years will keep on growing.<br />

“If you are not regularly updating<br />

your technology-related competence, it<br />

will show,” he says. “Employers and clients<br />

expect you to be current and are less likely<br />

to trust your judgment in other matters if<br />

you are not reasonably knowledgeable<br />

about technology.<br />

“For <strong>CA</strong>s in decision-making positions,<br />

the challenge is to know the right amount<br />

about technology options,” he explains.<br />

“You need to know the agendas and the<br />

shortcomings <strong>of</strong> the technology experts<br />

who advise you so you’re in a good<br />

position to make the business objectives<br />

drive the technology decisions rather than<br />

the other way around.”<br />

Belyea cautions that while learning<br />

about technology is quite exciting, it can<br />

also be dangerous to “fall in love” with<br />

technology solutions.<br />

“I have seen that happen and it’s<br />

fatal,” he points out. “This is a challenge<br />

that the <strong>CA</strong> pr<strong>of</strong>ession needs to address<br />

overtly. I think there is room for more<br />

education about the business <strong>of</strong> managing<br />

technology and all the related change<br />

management issues.”<br />

Jim McCulloch, <strong>CA</strong>, a tax partner<br />

with the Vancouver firm <strong>of</strong> Rolfe<br />

Benson, <strong>Chartered</strong> <strong>Accountants</strong>, has been<br />

around technology for a long time. A <strong>CA</strong><br />

since 1970, he remembers being “forced”<br />

along with all his tax colleagues into<br />

learning how to use Osborne computers<br />

and a program called “Visicalc”, the original<br />

spreadsheet.<br />

“Today it’s e-filing, totally computerized<br />

tax forms, project modeling and<br />

excellent tax research resources on the<br />

‘net or CD ROM updates,” he says. “It’s<br />

been a remarkable 20 years.”<br />

McCulloch himself has been ‘wired’ at<br />

both home and <strong>of</strong>fice for at least 15 years<br />

and relies heavily on his Lotus organizer.<br />

He carries a cell phone, but no laptop — at<br />

least not yet.<br />

“For clients, technology has meant so<br />

many improvements, it’s just marvelous,”<br />

he explains. “The computerization <strong>of</strong> all<br />

aspects <strong>of</strong> accounting — for example, the<br />

paperless audit and fully integrated<br />

systems — have improved operations and<br />

reporting immeasurably. And <strong>of</strong> course e-<br />

commerce will be a big market in the near<br />

future, though it means issues <strong>of</strong> security<br />

and privacy, too.”<br />

McCulloch admits there are some<br />

clients — and even some staff — who are<br />

resistant to technology, but “those<br />

numbers are small and dwindling all the<br />

time”.<br />

“I know it can be a long, slow process<br />

for some older <strong>CA</strong>s, especially when every<br />

<strong>CA</strong> student or young <strong>CA</strong> who comes<br />

through the door is so keen on all aspects<br />

<strong>of</strong> technology, but you have to embrace it,”<br />

McCulloch says. “<strong>CA</strong>s must go for all the<br />

technological knowledge they can acquire<br />

and always be on the leading edge. Clients<br />

and employers expect it, demand it.”<br />

Right now, McCulloch says he’s<br />

working with voice-recognition s<strong>of</strong>tware<br />

for dictation (“it’s not quite there yet”) and<br />

he’s convinced we’ll all have personal<br />

information managers soon.<br />

Travis Bryson, <strong>CA</strong>, “unplugs”when<br />

he’s at home. “I haven’t let technology<br />

grab too much <strong>of</strong> my life at home,”<br />

Bryson says. “There’s no cell, no laptop and<br />

no pager there. At work, it’s another story.<br />

There I’m totally plugged in.”<br />

Bryson, a <strong>CA</strong> since 1996, is the<br />

Manager <strong>of</strong> Business and<br />

Technology Solutions at<br />

BDO Dunwoody LLP in<br />

Vancouver. He says he<br />

remembers his first<br />

encounters with 286<br />

computers during his<br />

articling days in the early<br />

‘90s. [cont’d on page 24]<br />

10 Beyond Numbers / September 2000

Putting Transfer Pricing<br />

into Practice<br />

Trying to find how you can<br />

make the most <strong>of</strong> transfer<br />

pricing opportunities? Look no<br />

further! The <strong>BC</strong> Pr<strong>of</strong>essional<br />

Development program is<br />

<strong>of</strong>fering you a unique opportunity<br />

to hear three leading<br />

experts tell you how in this<br />

exciting new seminar.<br />

“Transfer Pricing & Foreign Tax<br />

Credits,” will provide participants will<br />

real-life insight into a variety <strong>of</strong><br />

transfer pricing issues. A case study<br />

will be presented by tax and trade law<br />

specialist Terrance Sweeney, BA, LLB, a<br />

senior tax partner in Borden Ladner<br />

Gervais LLP – Toronto <strong>of</strong>fice. The study<br />

deals with an Italian company and its<br />

Canadian subsidiary, and will cover<br />

the law, current administrative<br />

practices, and other issues.<br />

Instructor Lionel Newton, <strong>CA</strong>,<br />

practises in the area <strong>of</strong> cross-border<br />

taxation, estates, and litigation<br />

support. He will address tax credits<br />

related to foreign income, including<br />

what to watch for, recognition,<br />

timing, and utilization <strong>of</strong> credit<br />

alternatives. Key areas <strong>of</strong> the Canada-<br />

U.S. tax treaty will also be covered.<br />

Bob Crawford, <strong>CA</strong>, ATII, will bring<br />

a European perspective to the seminar.<br />

Crawford is a specialist in helping<br />

corporate and individual clients<br />

reduce their tax burden while complying<br />

with domestic and international<br />

laws. During the seminar, he will<br />

discuss the movement <strong>of</strong> goods in the<br />

European market. Key VAT-related<br />

issues will also be covered, an area <strong>of</strong><br />

where Crawford is an authority as he<br />

serves on the VAT Tribunal. He also<br />

chairs the Scottish <strong>Institute</strong>’s e-<br />

commerce initiative.<br />

To register call the I<strong>CA</strong><strong>BC</strong> Pr<strong>of</strong>essional<br />

Development Department at<br />

(604) 488-2641, toll-free 1-800-663-<br />

2677, fax, (604) 684-1267 or e-mail<br />

ong@ica.bc.ca<br />

Code T0310a<br />

October 27<br />

9am-5pm<br />

Sutton Place Hotel<br />

Non-Member $595<br />

Member $495<br />

Passport Invalid<br />

PD Week Schedule<br />

Victoria September 25th - 28th Harbour Towers Hotel<br />

Surrey October 2nd - 4th Guildford Sheraton Inn<br />

Parksville October 11th-13th Best Western Bayside Inn<br />

Vancouver October 23rd - 28th Sutton Place Hotel<br />

Kamloops November 6th-8th Coast Candian Inn<br />

Kelowna November 20th-24th Grande Okanagan Resort<br />

PD Schedule<br />

Vancouver Schedule<br />

(excluding PD Week, see flyer enclosed)<br />

Oct 3 Employment Standards Update*<br />

Oct 11 Effective Instructional Skills**<br />

Oct 12 Income Tax Update<br />

Oct 13 Understanding US Immigration**<br />

Oct 14 Introduction to the Mining Industry<br />

Oct 14 Rules & Standards<br />

Oct 16 Caseware 2000<br />

Oct 16 Business Process Re-engineering<br />

Oct 17 Caseview I<br />

Oct 17 Balanced Scorecards<br />

Oct 18 Caseview II<br />

Oct 18 Getting Ready for e-Business<br />

Oct 18 Taxation <strong>of</strong> Emigrating Canadians*<br />

Oct 19 Accounting & Auditing Update<br />

for Mutual Funds<br />

Oct 19 Motivating Your Staff Towards<br />

Peak Performance<br />

Oct 20 Section 85<br />

Oct 20-21 Income Tax Refresher: Corporate<br />

Oct 21 Effective Management Skills<br />

Surrey PD Week - Guildford Sheraton Inn<br />

Oct 2 Accounting, Auditing &<br />

Pr<strong>of</strong>essional Practice Update<br />

Oct 2 Advanced Tax Planning<br />

Oct 3 Business Valuation: Basic<br />

Oct 3 Financial Statement Presentation<br />

Oct 4 Income Tax Update<br />

Parksville PD Week - BaysideInn<br />

Oct 11 Review & Compilation Engagements<br />

Oct 11 Business Valuation: Basic<br />

Oct 12 Financial Statement Presentation<br />

Oct 12 Advanced Tax Planning<br />

Oct 13 Income Tax Update<br />

Victoria PD Week - Harbour Towers Hotel<br />

Sept 25 Purchase & Sale <strong>of</strong> a Business<br />

Sept 26 Charitable Gift Planning**<br />

Sept 26 Staying Out <strong>of</strong> Trouble**<br />

Sept 26 Building an E-Business Presence<br />

Sept 27 Accounting, Auditing &<br />

Pr<strong>of</strong>essional Practice Update<br />

Sept 27 E-Business Security,<br />

Controls & Assurance<br />

Sept 28 Accounting for Income Taxes<br />

Sept 28 Business Valuation: Basic<br />

Sept 29 Income Tax Update<br />

Kelowna Schedule<br />

Oct 2 Caseware 2000<br />

Oct 3 Caseview I<br />

Oct 4 Caseview II<br />

Oct 24 NPOs: Accounting & Auditing Issues<br />

All seminars listed are one or two days long, except:<br />

*executive breakfast seminar<br />

** half-day seminar<br />

September 2000 / Beyond Numbers 11

Firms Like Wolrige Mahon Get a<br />

Head Start on Attracting Top Talent<br />

By Melodie Yue<br />

Firms like Wolrige Mahon, tax and<br />

small business consultants, know the<br />

importance <strong>of</strong> hiring for skill set and<br />

mentoring their recruits to become<br />

future leaders, managers and strong<br />

contributors within their firm. As part<br />

<strong>of</strong> Wolrige Mahon’s philosophy and<br />

mindset, this mentoring approach can<br />

almost guarantee that their <strong>CA</strong>s will<br />

have what it takes to work effectively<br />

with team members, communicate<br />

clearly with clients and build the<br />

leadership skills necessary in the<br />

business world — whether the recruit’s<br />

background is engineering,<br />

finance or psychology.<br />

Wolrige Mahon’s belief in this<br />

mentoring approach extends beyond<br />

the firm’s own four walls. As a major<br />

sponsor <strong>of</strong> Leaders <strong>of</strong> Tomorrow<br />

(LOT) , an innovative student program<br />

started in 1999 by the Vancouver<br />

Board <strong>of</strong> Trade, Wolrige Mahon has<br />

committed to providing mentorship<br />

for a select number <strong>of</strong> LOT students.<br />

The approximately 100 students<br />

selected for this program are top<br />

students in their field <strong>of</strong> study with<br />

exceptional community service,<br />

leadership and communication skills,<br />

which means Wolrige Mahon may have<br />

a head-start in recruiting top new<br />

talent to their firm.<br />

When asked about the firm’s<br />

participation in the LOT program,<br />

Wolrige Mahon partner Gregg Smith,<br />

<strong>CA</strong> states, “This is an excellent<br />

program where the students get a<br />

taste <strong>of</strong> what’s happening in the<br />

business community. Often, many<br />

students have gone straight through<br />

school and their knowledge is all out<br />

<strong>of</strong> a book. It’s important to mingle, get<br />

out and learn about the experiences <strong>of</strong><br />

business people.”<br />

Supporting and helping students<br />

achieve their goals early is a win-win<br />

for both the mentor and student, as<br />

more firms are beginning to see and<br />

reap the benefits <strong>of</strong> providing<br />

mentorship to their candidates in the<br />

early stages <strong>of</strong> their careers.<br />

To become a mentor in The Leaders <strong>of</strong><br />

Tomorrow program, contact the Chair,<br />

Glenn Young, at 684-9186 or<br />

gyoung@itstradewind.com or the Project<br />

Coordinator, Rebecca Clapperton at 641-1246<br />

and rclapperton@board<strong>of</strong>trade.com.<br />

Taking Control<br />

The job <strong>of</strong> corporate controller<br />

is being reinvented, particularly<br />

among controllers who report to<br />

heads <strong>of</strong> business units. The results<br />

<strong>of</strong> an ongoing study by Gunn<br />

Partners and Georgia State University<br />

show that these executives are<br />

assuming a business-partner role<br />

in which they advise CEOs and<br />

CFOs on strategic-planning issues.<br />

These controllers name communicating,<br />

acting strategically, and<br />

influencing others as the key<br />

competencies for their jobs in the<br />

future. Controllers who report to<br />

financial executives, on the other<br />

hand, rank other competencies<br />

higher than those three.<br />

Source: “Corporate Controllers<br />

Reinvent Themselves,” Financial Executive,<br />

July/August 2000<br />

12 Beyond Numbers / September 2000

Coming this month -<br />

<strong>BC</strong> Check Up 2000<br />

In mid-September, the I<strong>CA</strong><strong>BC</strong> will<br />

be releasing the 2 nd annual <strong>BC</strong> Check-<br />

Up, a report on living, working, and<br />

investing in British Columbia. The<br />

study reviews 15 economic and social<br />

indicators and compiles LIVE, WORK,<br />

and INVEST Indices.<br />

This year’s report has been<br />

expanded to include interjurisdictional<br />

comparisons between<br />

B.C. and the other “have” provinces<br />

<strong>of</strong> Alberta and Ontario, as<br />

well as the national average.<br />

The result is a comprehensive<br />

economic and social assessment<br />

<strong>of</strong> Canada’s three richest<br />

provinces.<br />

The <strong>Institute</strong> is compiling and<br />

releasing the <strong>BC</strong> Check-Up report to<br />

increase both the awareness and<br />

relevance <strong>of</strong> the pr<strong>of</strong>ession within the<br />

business community, news media, and<br />

government.<br />

In doing so, the report shows that<br />

<strong>CA</strong>s do much more than tax and audit,<br />

and have an important role to play in<br />

the public policy arena <strong>of</strong> the province.<br />

A media campaign and speaking<br />

engagements are planned for the <strong>BC</strong><br />

Check-Up this fall. <strong>Institute</strong> CEO Richard<br />

Rees, <strong>CA</strong> will be speaking to a breakfast<br />

meeting <strong>of</strong> the Vancouver Board <strong>of</strong> Trade<br />

on September 19 th , and a breakfast event<br />

for the Kelowna Chamber <strong>of</strong> Commerce<br />

on September 26 th . Events in Victoria<br />

and Prince George are also in the works,<br />

as are PD workshops.<br />

Watch for a special member<br />

mailing <strong>of</strong> the <strong>BC</strong> Check-Up 2000 this<br />

month, and catch updates on <strong>BC</strong> Check-<br />

Up events on the I<strong>CA</strong><strong>BC</strong> Web site at<br />

www.ica.bc.ca.<br />

For more information on the <strong>BC</strong><br />

Check-Up 2000 report, contact Craig<br />

Fitzsimmons at 488-2625/1-800-663-<br />

2677 or e-mail fitzsimm@ica.bc.ca<br />

Top 10 Uses for the<br />

<strong>BC</strong> Check-Up:<br />

1. Write about it in your firm’s<br />

newsletter.<br />

2. Send a copy <strong>of</strong> the report to your<br />

clients.<br />

3. Send a copy <strong>of</strong> the report to<br />

prospective clients.<br />

4. Write a column in your local<br />

newspaper about the results <strong>of</strong> the<br />

report.<br />

5. Use the information when advising<br />

clients on the investment<br />

climate in B.C.<br />

6. Include copies <strong>of</strong> the report in your<br />

<strong>of</strong>fice’s lobby or waiting area.<br />

7. Consider giving a speech on the<br />

report in your community.<br />

8. Put the <strong>BC</strong> Check-Up report on<br />

your Web site.<br />

9. Show the report to your non-<strong>CA</strong><br />

colleagues.<br />

10. Bring your clients to <strong>BC</strong> Check-Up<br />

speeches in your area.<br />

September 2000 / Beyond Numbers 13

High-tech leader launches<br />

<strong>BC</strong> Business Summit 2000<br />

The second-ever <strong>BC</strong> Business<br />

Summit conference will be held on<br />

November 18-19, 2000 at the Westin<br />

Bayshore Hotel & Convention Centre<br />

in Vancouver.<br />

<strong>BC</strong> Business Summit 2000 will be<br />

attended by entrepreneurs and private<br />

sector leaders from throughout the<br />

province, including the I<strong>CA</strong><strong>BC</strong>. The<br />

event will build upon the momentum<br />

created by the first <strong>BC</strong> Business Summit<br />

in 1998 and the Panel on Securing<br />

<strong>BC</strong>’s Future in the fall <strong>of</strong> 1999 in pursuit<br />

<strong>of</strong> economic change and renewal in<br />

British Columbia.<br />

“I believe we are on the threshold<br />

<strong>of</strong> tremendous economic and social<br />

change in this province, and I am proud<br />

to be part <strong>of</strong> a business community that<br />

is taking a leadership role in forging that<br />

change,” said Bob Bailey, CEO <strong>of</strong> PMC<br />

Sierra Inc. in announcing the event.<br />

The Summit process began in November<br />

1998, when more than 800 business<br />

leaders attended the first-ever <strong>BC</strong> Business<br />

Summit conference. While the first Summit<br />

event focused on the province’s economic<br />

challenges and on identifying the policy<br />

changes necessary for economic renewal,<br />

<strong>BC</strong> Business Summit 2000 will focus on<br />

creating a common vision for the province’s<br />

economic future.<br />

“<strong>BC</strong> Business Summit 2000 will<br />

provide a venue for all business people to<br />

contribute their perspectives, their experience<br />

and their enthusiasm,” Bailey said.<br />

<strong>BC</strong> Business Summit 2000 is being<br />

organized by 52 business organizations<br />

and industry associations, whose<br />

memberships collectively represent<br />

more than 90 per cent <strong>of</strong> all private<br />

sector employers in British Columbia.<br />

Detailed information about the <strong>BC</strong><br />

Business Summit 2000 program will be<br />

released in the fall.<br />

14 Beyond Numbers / September 2000

September 2000 / Beyond Numbers 15

16 Beyond Numbers / September 2000

September 2000 / Beyond Numbers 17

Under New Management<br />

By Deborah Folka, APR<br />

“Under New Management” is a<br />

phrase you <strong>of</strong>ten see associated with<br />

businesses hoping to rise phoenix-like<br />

from the ashes <strong>of</strong> difficulties. And<br />

organizations like the <strong>Institute</strong> <strong>of</strong><br />

<strong>Chartered</strong> <strong>Accountants</strong> <strong>of</strong> British<br />

Columbia are <strong>of</strong>ten thought to plod<br />

along without change forever.<br />

Wrong on both counts.<br />

Along with a Chief Executive<br />

Officer whose term is only a year old,<br />

the <strong>Institute</strong> really is ‘under new<br />

management’ and it has nothing to do<br />

with old difficulties, but rather with<br />

new opportunities.<br />

hen I arrived at the <strong>Institute</strong><br />

“W<br />

in mid-1999, I<br />

took some time<br />

to review the<br />

management<br />

structure,”<br />

Richard Rees, <strong>CA</strong>,<br />

CEO <strong>of</strong> I<strong>CA</strong><strong>BC</strong><br />

says. “I looked at<br />

the alignment<br />

<strong>of</strong> the functions<br />

— internal and external — at a vacant<br />

Chief Operating Officer position and<br />

decided a more effective operational<br />

alignment would be four functions:<br />

Member Services, External Affairs, Internal<br />

Operations and Education.”<br />

Rees’s approach has flattened the<br />

<strong>Institute</strong>’s management structure and<br />

eased reporting structures into a framework<br />

which better reflects the needs <strong>of</strong><br />

the members and the external demands<br />

on an organization constituted to protect<br />

the public interest.<br />

“Since June 1, we’ve put four<br />

senior directors into new roles with<br />

departmental management responsibility,”<br />

Rees explains. “The pr<strong>of</strong>essional<br />

programs <strong>of</strong> the <strong>Institute</strong> will<br />

continue to be managed by program<br />

18 Beyond Numbers / September 2000

directors and managers.”<br />

The four are Director <strong>of</strong> External<br />

Affairs Lesley MacGregor, MBA ; Director<br />

<strong>of</strong> Internal Operations Jan Sampson, <strong>CA</strong>;<br />

Director <strong>of</strong> Member Services Barry<br />

Mottershead, <strong>CA</strong> and Director <strong>of</strong><br />

Education Dr. Don Carter, F<strong>CA</strong>.<br />

MacGregor joined the <strong>Institute</strong><br />

earlier this year after<br />

five years with the Heart and Stroke<br />

Foundation <strong>of</strong> B.C. & Yukon as Manager<br />

and Director <strong>of</strong> Advocacy and Public<br />

Issues. Prior to that, she was Director <strong>of</strong><br />

Marketing and Communication at the<br />

Canadian Nature Federation, an environmental<br />

advocacy group based in Ottawa.<br />

As Director <strong>of</strong> External Affairs,<br />

MacGregor is responsible for government<br />

relations,<br />

media relations,<br />

member<br />

communications,<br />

marketing,<br />

recruiting,<br />

pr<strong>of</strong>essional<br />

development<br />

and planning.<br />

“My goals<br />

are three-fold,”<br />

MacGregor says. “I want to demonstrate<br />

to government, to the business community<br />

and to students the important role<br />

that <strong>CA</strong>s play in a broad range <strong>of</strong> businesses;<br />

to enhance communication with<br />

members and to ensure that <strong>CA</strong>s have<br />

access to outstanding pr<strong>of</strong>essional<br />

development, especially through the<br />

application <strong>of</strong> new methods <strong>of</strong> learning.”<br />

Director <strong>of</strong> Internal Operations<br />

Jan Sampson, <strong>CA</strong>, was most<br />

recently Director <strong>of</strong> Practice Review<br />

and Licensing at I<strong>CA</strong><strong>BC</strong> for five years.<br />

In that role, Sampson coordinated a<br />

team <strong>of</strong> review <strong>of</strong>ficers who help firms<br />

meet the <strong>CA</strong> standard <strong>of</strong> public<br />

practice in the most efficient ways.<br />

“With the changes in standards<br />

and the broadening <strong>of</strong> areas in which<br />

practitioners work, the challenge was<br />

to ensure that PR&L was relevant to<br />

our public practice members in an<br />

on-line, real-time world,” Sampson<br />

points out.<br />

Before joining the <strong>Institute</strong>,<br />

Sampson<br />

was in<br />

public<br />

practice for<br />

almost 20<br />

years,<br />

working in<br />

a variety <strong>of</strong> areas including forensic<br />

accounting, computer auditing, quality<br />

assurance, assisting owner-managers<br />

and international financial investigations.<br />

Her new responsibilities include<br />

management <strong>of</strong> human resources,<br />

finance, administration and technology.<br />

“With our new technology platform,<br />

there is tremendous opportunity to<br />

share among the provincial institutes<br />

and truly explore and develop the<br />

potential for technology in the areas <strong>of</strong><br />

membership information and financial<br />

reporting at I<strong>CA</strong><strong>BC</strong>,” Sampson explains.<br />

Barry Mottershead, <strong>CA</strong>, has<br />

been with the <strong>Institute</strong> for 15<br />

years. He moved from a public<br />

practice firm in the Okanagan to<br />

become the Pr<strong>of</strong>essional Standards<br />

Advisor. After four years in that role,<br />

he became the Director <strong>of</strong> Practice<br />

Review and Licensing for six years. In<br />

1995, Mottershead moved into the<br />

position <strong>of</strong> Director <strong>of</strong> Pr<strong>of</strong>essional<br />

Advisory Services.<br />

“In my new role as Director <strong>of</strong><br />

Member Services, I will lead the<br />

operation <strong>of</strong> all<br />

the memberfocused<br />

programs<br />

at the<br />

<strong>Institute</strong>,”<br />

Mottershead<br />

explains. “This<br />

includes legislative<br />

and selfregulatory<br />

matters — i.e.<br />

the <strong>CA</strong> Act, bylaws and rules <strong>of</strong> conduct<br />

and so on — the operation <strong>of</strong> the peer<br />

review programs (ethics, discipline and<br />

practice review) and the pr<strong>of</strong>essional<br />

advisory and related member services.”<br />

Mottershead says he intends to<br />

develop and implement programs to<br />

assess and respond to member needs<br />

across all segments <strong>of</strong> the <strong>Institute</strong>’s<br />

membership, “...with particular emphasis<br />

on addressing the needs <strong>of</strong> members<br />

outside public practice.”<br />

“We are clearly moving towards an<br />

increase in our external focus, as well<br />

as enhanced member services to all<br />

sectors <strong>of</strong> our membership,”<br />

Mottershead points out. “The use <strong>of</strong><br />

technology will be a significant<br />

component in achieving these strategic<br />

directions. The use <strong>of</strong> the Web site and<br />

e-mail and other technologies gives the<br />

<strong>Institute</strong> the opportunity to provide<br />

innovative, relevant, cost-effective<br />

programs for all our members.”<br />

Don Carter, Ph.D., F<strong>CA</strong>, has<br />

been involved in the education<br />

<strong>of</strong> chartered accountants<br />

throughout his entire career. He<br />

joined I<strong>CA</strong><strong>BC</strong> as principal <strong>of</strong> the<br />

School <strong>of</strong> <strong>Chartered</strong> Accountancy in<br />

1980 and now assumes the role <strong>of</strong><br />

Director <strong>of</strong> Education.<br />

“The most important development<br />

in the education <strong>of</strong> <strong>CA</strong>s in this<br />

province is the<br />

establishment<br />

<strong>of</strong> the new <strong>CA</strong><br />

School <strong>of</strong><br />

Business this<br />

past spring,”<br />

Carter explains.<br />

“In turning our<br />

education<br />

process into<br />

one that is<br />

learner-focused, instead <strong>of</strong> instructorfocused<br />

and taking full advantage <strong>of</strong><br />

new technologies for distance learning,<br />

we are jumping into the future <strong>of</strong><br />

education for the pr<strong>of</strong>ession.<br />

“<strong>CA</strong>SB will use the latest technology<br />

to deliver the most relevant<br />

training programs available to <strong>CA</strong>s<br />

today,” Carter says. “The training <strong>CA</strong><br />

students will receive will be more<br />

applicable right away to the ‘real world’<br />

and focused on competencies as<br />

opposed to academic subjects.”<br />

With the new management<br />

structure, there are also some new<br />

faces at a program director level. We<br />

will be pr<strong>of</strong>iling the program directors<br />

in an upcoming issue.<br />

September 2000 / Beyond Numbers 19

Member Recognition<br />

Procedures for<br />

Election <strong>of</strong> Fellows<br />

1. Nominations for the election <strong>of</strong> Fellows<br />

shall be sought from all members <strong>of</strong><br />

the <strong>Institute</strong> and the F<strong>CA</strong> Nominating<br />

Committee.<br />

2. Nominations shall be submitted on an<br />

approved nomination form signed by a<br />

proposer and two seconders.<br />

3. Nominators must demonstrate that<br />

their nominee has given outstanding<br />

service to the pr<strong>of</strong>ession or brought<br />

distinction to it in the following<br />

areas. Except in extraordinary<br />

circumstances, the nominee must<br />

have provided leadership and service<br />

with distinction in more than one <strong>of</strong><br />

these areas.<br />

a. in the work <strong>of</strong> the British Columbia<br />

or Canadian <strong>Institute</strong>;<br />

b. in the work <strong>of</strong> an Association having<br />

objectives relating to the candidate’s<br />

chosen business or pr<strong>of</strong>ession;<br />

c. in the pursuit <strong>of</strong> his/her career;<br />

d. in service (civic, community, political<br />

or not-for-pr<strong>of</strong>it organizations);<br />

e. in research, teaching, writing or<br />

speaking on pr<strong>of</strong>essional matters.<br />

4. The fullest possible information on the<br />

nominee is to be given, together with<br />

reasons why he/she should be considered<br />

for election as a Fellow, all supplemented<br />

by additional comments where necessary.<br />

To be recognized as having brought<br />

distinction to the pr<strong>of</strong>ession, it is <strong>of</strong><br />

paramount importance that in the activity<br />

cited, the member is clearly identified as<br />

being a <strong>Chartered</strong> Accountant. Service<br />

must be rendered while a member <strong>of</strong> the<br />

<strong>Institute</strong> <strong>of</strong> <strong>Chartered</strong> <strong>Accountants</strong> <strong>of</strong><br />

British Columbia. Proposers or seconders<br />

may wish to contact the secretary, spouse<br />

or business associates <strong>of</strong> the candidate, or<br />

the candidate directly, if additional<br />

information on certain sections <strong>of</strong> the<br />

form is required.<br />

5. Sitting members <strong>of</strong> Council,<br />

exclusive <strong>of</strong> the <strong>Institute</strong>’s First<br />

Vice-President, shall not be<br />

eligible to be elected Fellows.<br />

6. An F<strong>CA</strong> designation may be<br />

awarded posthumously only if<br />

the candidate died after the<br />

F<strong>CA</strong> Nominating Committee<br />

recommended the awarding <strong>of</strong><br />

his/her fellowship. An exception<br />

would be made if an<br />

outstanding individual died<br />

before the next F<strong>CA</strong> Nominating<br />

Committee meeting, when<br />

the Executive Committee could<br />

refer that individual to the<br />

current F<strong>CA</strong> Nominating<br />

Committee for its consideration.<br />

7. Nomination forms shall be<br />

submitted to a nominating<br />

committee to consist <strong>of</strong> a<br />

minimum <strong>of</strong> five members (the<br />

“Committee”). The Chair <strong>of</strong> the<br />

Committee shall be an F<strong>CA</strong><br />

appointed by Council at its July<br />

meeting, and he/she shall select<br />

his/her Committee at his/her<br />

discretion from F<strong>CA</strong>s, including<br />

always a past president <strong>of</strong> the<br />

<strong>Institute</strong>.<br />

8. The Chief Executive Officer should<br />

attend all meetings as staff liaison and<br />

resource person.<br />

9. The procedures for election <strong>of</strong> Fellows<br />

are to be published in the September<br />

issue <strong>of</strong> Beyond Numbers, with a view<br />

to educating the members on the<br />

election process and eliciting nominations.<br />

10. Nominations shall be sought in the<br />

period from September 1 to October 15 in<br />

each year.<br />

11. The Chief Executive Officer shall review<br />

each nomination form and delete<br />

information known to be in error and<br />

add information known to be omitted.<br />

If necessary, the Chief Executive Officer<br />

shall contact the proposer or seconders<br />

for additional information.<br />

12. The Committee shall:<br />

a. review the nominations received<br />

from the members, accept or reject<br />

them, correct or add to data submitted;<br />

b. prepare its own nominations, as<br />

considered necessary;<br />

c. ensure that all nominations have<br />

been vetted by the Chief Executive<br />

Officer for disciplinary matters; and<br />

d. prepare a complete list <strong>of</strong> candidates<br />

to appear on the election ballot.<br />

13. The Chair <strong>of</strong> the F<strong>CA</strong> Nominating<br />

Committee shall report to Council<br />

during an in-camera session on the<br />

results <strong>of</strong> the Committee’s deliberations<br />

before the ballots are distributed.<br />

Reviews <strong>of</strong> F<strong>CA</strong> candidates are to include<br />

advice <strong>of</strong> any violations <strong>of</strong> the Rules <strong>of</strong><br />

Pr<strong>of</strong>essional Conduct through the<br />

disciplinary process, regardless <strong>of</strong> when<br />

the <strong>of</strong>fences may have occurred, except<br />

violations where an anonymous<br />

Determination and Recommendation<br />

was issued more than two years prior to<br />

the F<strong>CA</strong> review and was accepted by the<br />

member cited.<br />

14. The election <strong>of</strong> Fellows shall be by ballot<br />

<strong>of</strong> Council members, each Council<br />

member being entitled to one vote for<br />

each candidate.<br />

15. There shall be one ballot only and all<br />

Council members shall vote for or<br />

against. At least 70% <strong>of</strong> Council must<br />

vote in favour <strong>of</strong> the candidate for him/<br />

her to be elected. If the government<br />

representative(s) deem(s) it appropriate<br />

20 Beyond Numbers / September 2000

to withdraw from the voting, the<br />

withdrawal will not represent an<br />

abstention, and Council will be regarded<br />

as complete without his/her/their<br />

participation. Where a conflict <strong>of</strong><br />

interest arises, the Council member(s)<br />

should so indicate on the ballot; Council<br />

will be regarded as complete without<br />

his/her/their participation in regard to<br />

that/those particular candidate(s).<br />

16. Scrutineers <strong>of</strong> the ballot shall be the<br />

President and the Chief Executive<br />

Officer.<br />

17. Announcement <strong>of</strong> the successful<br />

candidates shall be made to Council as<br />

soon as the ballots have been counted.<br />

Those elected shall be informed immediately.<br />

All members and the press shall<br />

be advised <strong>of</strong> the results <strong>of</strong> the election<br />

as soon as conveniently possible.<br />

18. Proposers <strong>of</strong> unsuccessful candidates<br />

should be advised <strong>of</strong> the candidate’s lack<br />

<strong>of</strong> success at either the nomination<br />

stage or the election stage (without<br />

disclosing which) by the Chair <strong>of</strong> the<br />

Nominating Committee.<br />

19. Nomination forms for those members<br />

not elected shall, on the recommendation<br />

<strong>of</strong> the Outgoing Committee, be brought<br />

forward to the Committee the following<br />

year for consideration. The applicable<br />

forms will go forward from the Outgoing<br />

Committee to the Incoming Committee,<br />

with a transmittal letter, and the Incoming<br />

Committee will be responsible for<br />

contacting the original proposers for the<br />

purpose <strong>of</strong> updating the information.<br />

20. The F<strong>CA</strong> Nominating Committee shall<br />