2006 - The Office of Public Accountability

2006 - The Office of Public Accountability

2006 - The Office of Public Accountability

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Government <strong>of</strong> Guam - Emergency<br />

Executive Orders and Certificates <strong>of</strong><br />

Emergency<br />

From April 2003 to December 2005, 18<br />

Executive Orders authorized the transfer <strong>of</strong><br />

up to $4.5M for local emergencies related to<br />

civil defense, public safety, and healthcare.<br />

<strong>The</strong>se emergency funds increased the<br />

General Fund deficit, as emergency funds<br />

are not budgeted.<br />

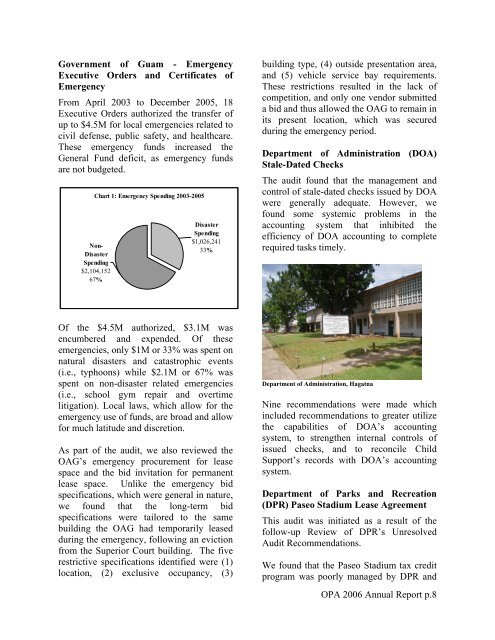

Chart 1: Emergency Spending 2003-2005<br />

Non-<br />

Disaster<br />

Spending<br />

$2,104,152<br />

67%<br />

Disaster<br />

Spending<br />

$1,026,241<br />

33%<br />

building type, (4) outside presentation area,<br />

and (5) vehicle service bay requirements.<br />

<strong>The</strong>se restrictions resulted in the lack <strong>of</strong><br />

competition, and only one vendor submitted<br />

a bid and thus allowed the OAG to remain in<br />

its present location, which was secured<br />

during the emergency period.<br />

Department <strong>of</strong> Administration (DOA)<br />

Stale-Dated Checks<br />

<strong>The</strong> audit found that the management and<br />

control <strong>of</strong> stale-dated checks issued by DOA<br />

were generally adequate. However, we<br />

found some systemic problems in the<br />

accounting system that inhibited the<br />

efficiency <strong>of</strong> DOA accounting to complete<br />

required tasks timely.<br />

Of the $4.5M authorized, $3.1M was<br />

encumbered and expended. Of these<br />

emergencies, only $1M or 33% was spent on<br />

natural disasters and catastrophic events<br />

(i.e., typhoons) while $2.1M or 67% was<br />

spent on non-disaster related emergencies<br />

(i.e., school gym repair and overtime<br />

litigation). Local laws, which allow for the<br />

emergency use <strong>of</strong> funds, are broad and allow<br />

for much latitude and discretion.<br />

As part <strong>of</strong> the audit, we also reviewed the<br />

OAG’s emergency procurement for lease<br />

space and the bid invitation for permanent<br />

lease space. Unlike the emergency bid<br />

specifications, which were general in nature,<br />

we found that the long-term bid<br />

specifications were tailored to the same<br />

building the OAG had temporarily leased<br />

during the emergency, following an eviction<br />

from the Superior Court building. <strong>The</strong> five<br />

restrictive specifications identified were (1)<br />

location, (2) exclusive occupancy, (3)<br />

Department <strong>of</strong> Administration, Hagatna<br />

Nine recommendations were made which<br />

included recommendations to greater utilize<br />

the capabilities <strong>of</strong> DOA’s accounting<br />

system, to strengthen internal controls <strong>of</strong><br />

issued checks, and to reconcile Child<br />

Support’s records with DOA’s accounting<br />

system.<br />

Department <strong>of</strong> Parks and Recreation<br />

(DPR) Paseo Stadium Lease Agreement<br />

This audit was initiated as a result <strong>of</strong> the<br />

follow-up Review <strong>of</strong> DPR’s Unresolved<br />

Audit Recommendations.<br />

We found that the Paseo Stadium tax credit<br />

program was poorly managed by DPR and<br />

OPA <strong>2006</strong> Annual Report p.8