2006 - The Office of Public Accountability

2006 - The Office of Public Accountability

2006 - The Office of Public Accountability

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

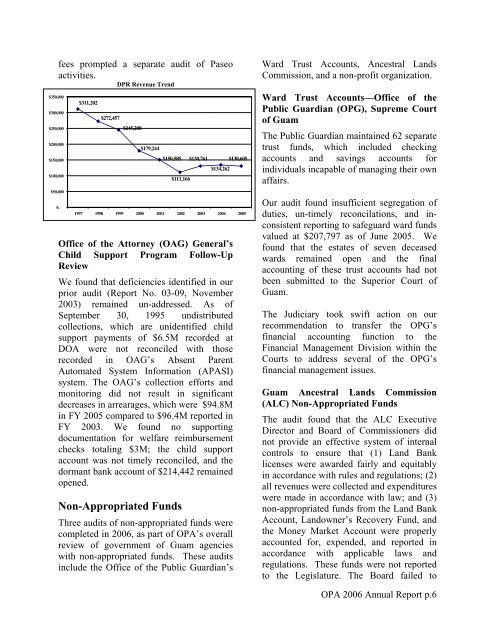

$350,000<br />

$300,000<br />

$250,000<br />

$200,000<br />

$150,000<br />

$100,000<br />

fees prompted a separate audit <strong>of</strong> Paseo<br />

activities.<br />

DPR Revenue Trend<br />

$50,000<br />

$-<br />

$311,202<br />

$272,457<br />

$245,208<br />

$179,244<br />

$150,585<br />

$111,166<br />

$130,761 $130,605<br />

$134,262<br />

1997 1998 1999 2000 2001 2002 2003 2004 2005<br />

<strong>Office</strong> <strong>of</strong> the Attorney (OAG) General’s<br />

Child Support Program Follow-Up<br />

Review<br />

We found that deficiencies identified in our<br />

prior audit (Report No. 03-09, November<br />

2003) remained un-addressed. As <strong>of</strong><br />

September 30, 1995 undistributed<br />

collections, which are unidentified child<br />

support payments <strong>of</strong> $6.5M recorded at<br />

DOA were not reconciled with those<br />

recorded in OAG’s Absent Parent<br />

Automated System Information (APASI)<br />

system. <strong>The</strong> OAG’s collection efforts and<br />

monitoring did not result in significant<br />

decreases in arrearages, which were $94.8M<br />

in FY 2005 compared to $96.4M reported in<br />

FY 2003. We found no supporting<br />

documentation for welfare reimbursement<br />

checks totaling $3M; the child support<br />

account was not timely reconciled, and the<br />

dormant bank account <strong>of</strong> $214,442 remained<br />

opened.<br />

Non-Appropriated Funds<br />

Three audits <strong>of</strong> non-appropriated funds were<br />

completed in <strong>2006</strong>, as part <strong>of</strong> OPA’s overall<br />

review <strong>of</strong> government <strong>of</strong> Guam agencies<br />

with non-appropriated funds. <strong>The</strong>se audits<br />

include the <strong>Office</strong> <strong>of</strong> the <strong>Public</strong> Guardian’s<br />

Ward Trust Accounts, Ancestral Lands<br />

Commission, and a non-pr<strong>of</strong>it organization.<br />

Ward Trust Accounts—<strong>Office</strong> <strong>of</strong> the<br />

<strong>Public</strong> Guardian (OPG), Supreme Court<br />

<strong>of</strong> Guam<br />

<strong>The</strong> <strong>Public</strong> Guardian maintained 62 separate<br />

trust funds, which included checking<br />

accounts and savings accounts for<br />

individuals incapable <strong>of</strong> managing their own<br />

affairs.<br />

Our audit found insufficient segregation <strong>of</strong><br />

duties, un-timely reconcilations, and inconsistent<br />

reporting to safeguard ward funds<br />

valued at $207,797 as <strong>of</strong> June 2005. We<br />

found that the estates <strong>of</strong> seven deceased<br />

wards remained open and the final<br />

accounting <strong>of</strong> these trust accounts had not<br />

been submitted to the Superior Court <strong>of</strong><br />

Guam.<br />

<strong>The</strong> Judiciary took swift action on our<br />

recommendation to transfer the OPG’s<br />

financial accounting function to the<br />

Financial Management Division within the<br />

Courts to address several <strong>of</strong> the OPG’s<br />

financial management issues.<br />

Guam Ancestral Lands Commission<br />

(ALC) Non-Appropriated Funds<br />

<strong>The</strong> audit found that the ALC Executive<br />

Director and Board <strong>of</strong> Commissioners did<br />

not provide an effective system <strong>of</strong> internal<br />

controls to ensure that (1) Land Bank<br />

licenses were awarded fairly and equitably<br />

in accordance with rules and regulations; (2)<br />

all revenues were collected and expenditures<br />

were made in accordance with law; and (3)<br />

non-appropriated funds from the Land Bank<br />

Account, Landowner’s Recovery Fund, and<br />

the Money Market Account were properly<br />

accounted for, expended, and reported in<br />

accordance with applicable laws and<br />

regulations. <strong>The</strong>se funds were not reported<br />

to the Legislature. <strong>The</strong> Board failed to<br />

OPA <strong>2006</strong> Annual Report p.6