Study of student costs using activity based costing methodology - aair

Study of student costs using activity based costing methodology - aair

Study of student costs using activity based costing methodology - aair

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

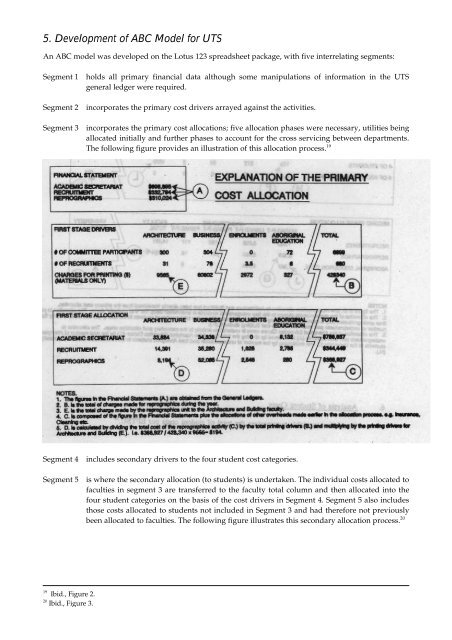

5. Development <strong>of</strong> ABC Model for UTS<br />

An ABC model was developed on the Lotus 123 spreadsheet package, with five interrelating segments:<br />

Segment 1<br />

holds all primary financial data although some manipulations <strong>of</strong> information in the UTS<br />

general ledger were required.<br />

Segment 2 incorporates the primary cost drivers arrayed against the activities.<br />

Segment 3<br />

incorporates the primary cost allocations; five allocation phases were necessary, utilities being<br />

allocated initially and further phases to account for the cross servicing between departments.<br />

The following figure provides an illustration <strong>of</strong> this allocation process. 19<br />

Segment 4 includes secondary drivers to the four <strong>student</strong> cost categories.<br />

Segment 5<br />

is where the secondary allocation (to <strong>student</strong>s) is undertaken. The individual <strong>costs</strong> allocated to<br />

faculties in segment 3 are transferred to the faculty total column and then allocated into the<br />

four <strong>student</strong> categories on the basis <strong>of</strong> the cost drivers in Segment 4. Segment 5 also includes<br />

those <strong>costs</strong> allocated to <strong>student</strong>s not included in Segment 3 and had therefore not previously<br />

been allocated to faculties. The following figure illustrates this secondary allocation process. 20<br />

19 Ibid., Figure 2.<br />

20 Ibid., Figure 3.