The world's local bank Annual Report and Accounts CCF - HSBC

The world's local bank Annual Report and Accounts CCF - HSBC

The world's local bank Annual Report and Accounts CCF - HSBC

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

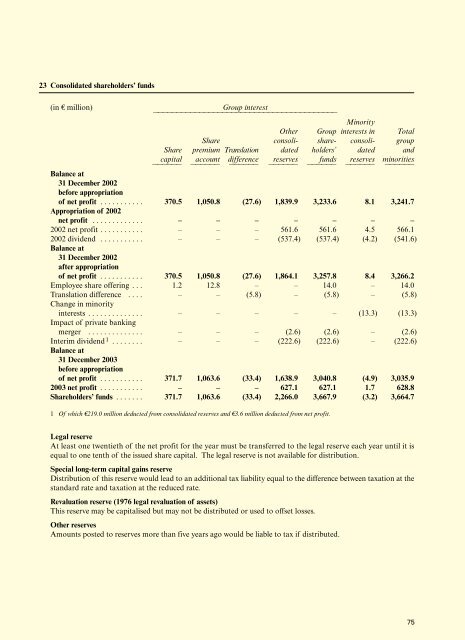

23 Consolidated shareholders’ funds<br />

(in € million)<br />

Group interest<br />

dddddddddddddddddddddddddddddddddddddddd<br />

Minority<br />

Other Group interests in Total<br />

Share consoli- share- consoli- group<br />

Share premium Translation dated holders’ dated <strong>and</strong><br />

capital account difference reserves funds reserves minorities<br />

dddddd dddddd dddddd dddddd dddddd dddddd dddddd<br />

Balance at<br />

31 December 2002<br />

before appropriation<br />

of net profit . . . . . . . . . . . 370.5 1,050.8 (27.6) 1,839.9 3,233.6 8.1 3,241.7<br />

Appropriation of 2002<br />

net profit . . . . . . . . . . . . . – – – – – – –<br />

2002 net profit . . . . . . . . . . . – – – 561.6 561.6 4.5 566.1<br />

2002 dividend . . . . . . . . . . . – – – (537.4) (537.4) (4.2) (541.6)<br />

Balance at<br />

31 December 2002<br />

after appropriation<br />

of net profit . . . . . . . . . . . 370.5 1,050.8 (27.6) 1,864.1 3,257.8 8.4 3,266.2<br />

Employee share offering . . . 1.2 12.8 – – 14.0 – 14.0<br />

Translation difference . . . . – – (5.8) – (5.8) – (5.8)<br />

Change in minority<br />

interests . . . . . . . . . . . . . . – – – – – (13.3) (13.3)<br />

Impact of private <strong>bank</strong>ing<br />

merger . . . . . . . . . . . . . . – – – (2.6) (2.6) – (2.6)<br />

Interim dividend 1 . . . . . . . . – – – (222.6) (222.6) – (222.6)<br />

Balance at<br />

31 December 2003<br />

before appropriation<br />

of net profit . . . . . . . . . . . 371.7 1,063.6 (33.4) 1,638.9 3,040.8 (4.9) 3,035.9<br />

2003 net profit . . . . . . . . . . . – – – 627.1 627.1 1.7 628.8<br />

Shareholders’ funds . . . . . . . 371.7 1,063.6 (33.4) 2,266.0 3,667.9 (3.2) 3,664.7<br />

1 Of which €219.0 million deducted from consolidated reserves <strong>and</strong> €3.6 million deducted from net profit.<br />

Legal reserve<br />

At least one twentieth of the net profit for the year must be transferred to the legal reserve each year until it is<br />

equal to one tenth of the issued share capital. <strong>The</strong> legal reserve is not available for distribution.<br />

Special long-term capital gains reserve<br />

Distribution of this reserve would lead to an additional tax liability equal to the difference between taxation at the<br />

st<strong>and</strong>ard rate <strong>and</strong> taxation at the reduced rate.<br />

Revaluation reserve (1976 legal revaluation of assets)<br />

This reserve may be capitalised but may not be distributed or used to offset losses.<br />

Other reserves<br />

Amounts posted to reserves more than five years ago would be liable to tax if distributed.<br />

75