Jersey Post Annual Report and Accounts | 2012 - States Assembly

Jersey Post Annual Report and Accounts | 2012 - States Assembly

Jersey Post Annual Report and Accounts | 2012 - States Assembly

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Jersey</strong> <strong>Post</strong> <strong>Annual</strong> <strong>Report</strong> <strong>and</strong> <strong>Accounts</strong> | <strong>2012</strong><br />

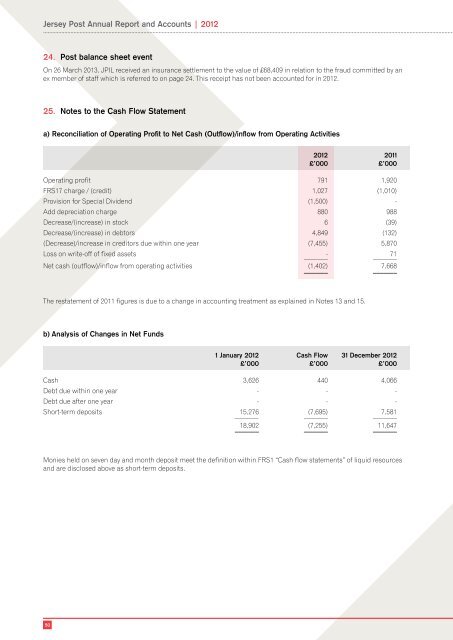

24. <strong>Post</strong> balance sheet event<br />

On 26 March 2013, JPIL received an insurance settlement to the value of £68,409 in relation to the fraud committed by an<br />

ex member of staff which is referred to on page 24. This receipt has not been accounted for in <strong>2012</strong>.<br />

25. Notes to the Cash Flow Statement<br />

a) Reconciliation of Operating Profit to Net Cash (Outflow)/inflow from Operating Activities<br />

<strong>2012</strong> 2011<br />

£’000 £’000<br />

Operating profit 791 1,920<br />

FRS17 charge / (credit) 1,027 (1,010)<br />

Provision for Special Dividend (1,500) -<br />

Add depreciation charge 880 988<br />

Decrease/(increase) in stock 6 (39)<br />

Decrease/(increase) in debtors 4,849 (132)<br />

(Decrease)/increase in creditors due within one year (7,455) 5,870<br />

Loss on write-off of fixed assets _______- _______ 71<br />

Net cash (outflow)/inflow from operating activities (1,402)<br />

_______<br />

7,668<br />

_______<br />

The restatement of 2011 figures is due to a change in accounting treatment as explained in Notes 13 <strong>and</strong> 15.<br />

b) Analysis of Changes in Net Funds<br />

1 January <strong>2012</strong> Cash Flow 31 December <strong>2012</strong><br />

£’000 £’000 £’000<br />

Cash 3,626 440 4,066<br />

Debt due within one year - - -<br />

Debt due after one year - - -<br />

Short-term deposits 15,276 (7,695) 7,581<br />

_______ _______ _______<br />

18,902 (7,255) 11,647<br />

_______ _______ _______<br />

Monies held on seven day <strong>and</strong> month deposit meet the definition within FRS1 “Cash flow statements” of liquid resources<br />

<strong>and</strong> are disclosed above as short-term deposits.<br />

50