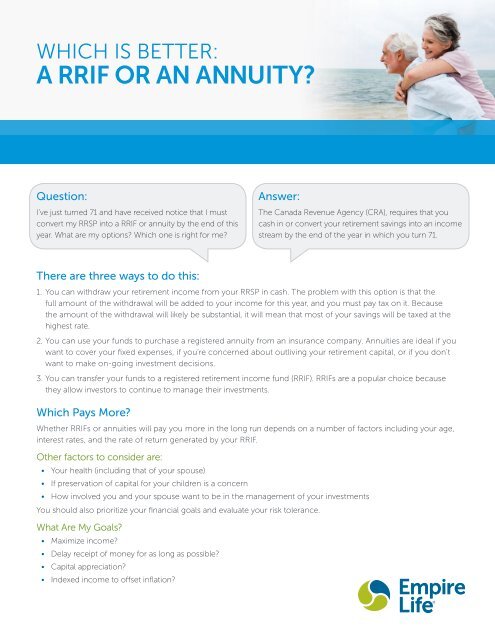

Which is Better: A RRIF or an Annuity? - Empire Life

Which is Better: A RRIF or an Annuity? - Empire Life

Which is Better: A RRIF or an Annuity? - Empire Life

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Which</strong> <strong>is</strong> better: a <strong>RRIF</strong> <strong>or</strong> <strong>an</strong> <strong>an</strong>nuity<br />

<strong>Which</strong> <strong>is</strong> better:<br />

a <strong>RRIF</strong> <strong>or</strong> <strong>an</strong> <strong>an</strong>nuity<br />

Question:<br />

I’ve just turned 71 <strong>an</strong>d have received notice that I must<br />

convert my RRSP into a <strong>RRIF</strong> <strong>or</strong> <strong>an</strong>nuity by the end of th<strong>is</strong><br />

year. What are my options <strong>Which</strong> one <strong>is</strong> right f<strong>or</strong> me<br />

Answer:<br />

The C<strong>an</strong>ada Revenue Agency (CRA), requires that you<br />

cash in <strong>or</strong> convert your retirement savings into <strong>an</strong> income<br />

stream by the end of the year in which you turn 71.<br />

There are three ways to do th<strong>is</strong>:<br />

1. You c<strong>an</strong> withdraw your retirement income from your RRSP in cash. The problem with th<strong>is</strong> option <strong>is</strong> that the<br />

full amount of the withdrawal will be added to your income f<strong>or</strong> th<strong>is</strong> year, <strong>an</strong>d you must pay tax on it. Because<br />

the amount of the withdrawal will likely be subst<strong>an</strong>tial, it will me<strong>an</strong> that most of your savings will be taxed at the<br />

highest rate.<br />

2. You c<strong>an</strong> use your funds to purchase a reg<strong>is</strong>tered <strong>an</strong>nuity from <strong>an</strong> insur<strong>an</strong>ce comp<strong>an</strong>y. Annuities are ideal if you<br />

w<strong>an</strong>t to cover your fixed expenses, if you’re concerned about outliving your retirement capital, <strong>or</strong> if you don’t<br />

w<strong>an</strong>t to make on-going investment dec<strong>is</strong>ions.<br />

3. You c<strong>an</strong> tr<strong>an</strong>sfer your funds to a reg<strong>is</strong>tered retirement income fund (<strong>RRIF</strong>). <strong>RRIF</strong>s are a popular choice because<br />

they allow invest<strong>or</strong>s to continue to m<strong>an</strong>age their investments.<br />

<strong>Which</strong> Pays M<strong>or</strong>e<br />

Whether <strong>RRIF</strong>s <strong>or</strong> <strong>an</strong>nuities will pay you m<strong>or</strong>e in the long run depends on a number of fact<strong>or</strong>s including your age,<br />

interest rates, <strong>an</strong>d the rate of return generated by your <strong>RRIF</strong>.<br />

Other fact<strong>or</strong>s to consider are:<br />

• Your health (including that of your spouse)<br />

• If preservation of capital f<strong>or</strong> your children <strong>is</strong> a concern<br />

• How involved you <strong>an</strong>d your spouse w<strong>an</strong>t to be in the m<strong>an</strong>agement of your investments<br />

You should also pri<strong>or</strong>itize your fin<strong>an</strong>cial goals <strong>an</strong>d evaluate your r<strong>is</strong>k toler<strong>an</strong>ce.<br />

What Are My Goals<br />

• Maximize income<br />

• Delay receipt of money f<strong>or</strong> as long as possible<br />

• Capital appreciation<br />

• Indexed income to offset inflation

<strong>Which</strong> <strong>is</strong> better: a <strong>RRIF</strong> <strong>or</strong> <strong>an</strong> <strong>an</strong>nuity<br />

What <strong>is</strong> my R<strong>is</strong>k Toler<strong>an</strong>ce<br />

If you’re r<strong>is</strong>k averse <strong>an</strong>d are only interested in guar<strong>an</strong>teed investments (such as GICs), then a life <strong>an</strong>nuity <strong>is</strong> probably<br />

your best bet. In a low interest rate environment, inclusion of the capital repayments dramatically increases your<br />

monthly <strong>or</strong> <strong>an</strong>nual income. As a result, reg<strong>is</strong>tered <strong>an</strong>nuities will almost invariably give you a higher retirement income<br />

th<strong>an</strong> a <strong>RRIF</strong>, without <strong>an</strong>y fear of running out of money. Annuities w<strong>or</strong>k best if you are over age 60.<br />

If you are a r<strong>is</strong>k taker <strong>RRIF</strong>s may be m<strong>or</strong>e attractive when you are able to obtain higher rates of return. The only way to<br />

achieve higher rates of return <strong>is</strong> by investing in stocks <strong>or</strong> equity funds, which <strong>is</strong> why your r<strong>is</strong>k toler<strong>an</strong>ce comes in to play.<br />

If you feel a bal<strong>an</strong>ced approach using a mix of 50% guar<strong>an</strong>teed investments <strong>an</strong>d 50% equities <strong>is</strong> a good<br />

comprom<strong>is</strong>e, then you might w<strong>an</strong>t to consider using a life <strong>an</strong>nuity f<strong>or</strong> the guar<strong>an</strong>teed p<strong>or</strong>tion <strong>an</strong>d a <strong>RRIF</strong> f<strong>or</strong> the<br />

equity p<strong>or</strong>tion. If the <strong>an</strong>nuity income <strong>is</strong> sufficient to meet your basic needs, th<strong>is</strong> approach allows you to be m<strong>or</strong>e<br />

aggressive in your investments.<br />

Table A below compares the amount of income you could expect to receive from a reg<strong>is</strong>tered <strong>an</strong>nuity as of J<strong>an</strong>uary<br />

2012, <strong>an</strong>d <strong>RRIF</strong>s at various rates of return. It also includes a bal<strong>an</strong>ced approach by combining a Joint & Last <strong>Life</strong> <strong>Annuity</strong><br />

f<strong>or</strong> $50,000 <strong>an</strong>d a <strong>RRIF</strong> f<strong>or</strong> $50,000 assuming a 6% <strong>an</strong>nual rate of return.<br />

Table A:<br />

Estimated Annual Income Produced by $100,000 of Reg<strong>is</strong>tered Funds at Age 71**<br />

Annuities 1 <strong>RRIF</strong>s 2 Combination 3<br />

<strong>Annuity</strong> / <strong>RRIF</strong><br />

Age Male <strong>Life</strong> - 10 Female <strong>Life</strong> - 10 Joint <strong>Life</strong> - 10 <strong>RRIF</strong> @ 4% <strong>RRIF</strong> @ 6% <strong>RRIF</strong> @ 8%<br />

@ 6%<br />

72 $7,843 $7,167 $6,347 $7,672 $7,818 $7,964 $7,042<br />

75 $7,843 $7,167 $6,347 $7,140 $7,704 $8,301 $6,985<br />

80 $7,843 $7,167 $6,347 $6,333 $7,517 $8,894 $6,892<br />

85 $7,843 $7,167 $6,347 $5,591 $7,300 $9,484 $6,783<br />

90 $7,843 $7,167 $6,347 $4,899 $7,036 $10,038 $6,651<br />

95 $7,843 $7,167 $6,347 $4,153 $6,562 $10,281 $6,414<br />

99 $7,843 $7,167 $6,347 $1,991 $3,396 $5,734 $4,831<br />

Total $219,604 $200,676 $177,716 $151,261 $193,419 $251,448 $184,436<br />

** Assumes a purchase date of J<strong>an</strong>uary, 2012 <strong>an</strong>d income payable <strong>an</strong>nually starting J<strong>an</strong>uary, 2013.<br />

1<br />

<strong>Annuity</strong> rates in effect as at J<strong>an</strong>uary, 2012. Based on a Single <strong>Life</strong> <strong>an</strong>d Joint <strong>Life</strong> <strong>Annuity</strong> f<strong>or</strong> male <strong>an</strong>d female, both age 71, with a 10-year guar<strong>an</strong>tee period.<br />

2<br />

<strong>RRIF</strong>s based on minimum income payments required by law. Assumes 4%, 6%, <strong>an</strong>d 8% <strong>an</strong>nual rate of return.<br />

3<br />

<strong>Annuity</strong> / <strong>RRIF</strong> combination <strong>is</strong> based on a $50,000 Joint & Last Surviv<strong>or</strong> <strong>Annuity</strong> f<strong>or</strong> male <strong>an</strong>d female at age 71, <strong>an</strong>d a $50,000 <strong>RRIF</strong> at a 6% assumed <strong>an</strong>nual<br />

rate of return.<br />

The Age Fact<strong>or</strong><br />

The younger you are, the longer your retirement income needs to last. When pl<strong>an</strong>ning your retirement, you’ll have to<br />

ensure you don’t use up your capital too quickly — you don’t w<strong>an</strong>t your income to expire bef<strong>or</strong>e you do! M<strong>an</strong>y fin<strong>an</strong>cial<br />

pl<strong>an</strong>ners point out that running out of money <strong>is</strong> one of the greatest d<strong>an</strong>gers facing seni<strong>or</strong>s today.<br />

<strong>Annuity</strong> income <strong>is</strong> also affected by your age <strong>an</strong>d <strong>an</strong>y minimum payment guar<strong>an</strong>tees. The longer the <strong>an</strong>nuity has to run,<br />

the smaller the amount of each monthly <strong>or</strong> <strong>an</strong>nual payment. Th<strong>is</strong> <strong>is</strong> the reason Joint & Last Surviv<strong>or</strong> <strong>an</strong>nuities pay less<br />

th<strong>an</strong> <strong>an</strong>nuities on only one life. It <strong>is</strong> also the reason life <strong>an</strong>nuities are less attractive f<strong>or</strong> younger people. However, one<br />

of the great adv<strong>an</strong>tages f<strong>or</strong> retirees <strong>is</strong> that the insur<strong>an</strong>ce comp<strong>an</strong>y providing the <strong>an</strong>nuity will base its calculations on the<br />

average length of time you’re expected to live, whereas with a <strong>RRIF</strong> you’ll have to ensure your <strong>RRIF</strong> income will last f<strong>or</strong><br />

the maximum period you might live. Table B shows estimates of the potential amount of <strong>an</strong>nual income f<strong>or</strong> Single <strong>an</strong>d<br />

Joint & Last Surviv<strong>or</strong> <strong>an</strong>nuities f<strong>or</strong> male <strong>an</strong>d female at age 71.<br />

2

<strong>Which</strong> <strong>is</strong> better: a <strong>RRIF</strong> <strong>or</strong> <strong>an</strong> <strong>an</strong>nuity<br />

Table B:<br />

$100,000 Reg<strong>is</strong>tered <strong>Life</strong> <strong>Annuity</strong><br />

Minimum<br />

Guar<strong>an</strong>tee Period † None 10 Years 18 Years<br />

Estimated Annual Income Estimated Annual Income Estimated Annual Income<br />

Male, age 71 $8,850 $7,843 $6,192<br />

Female, age 71 $7,688 $7,167 $6,025<br />

Joint & Last Surviv<strong>or</strong>,<br />

both age 71<br />

$6,460 $6,347 $5,804<br />

†<br />

In a single life <strong>an</strong>nuity, where the beneficiary <strong>is</strong> not the spouse <strong>or</strong> common-law partner, if the <strong>an</strong>nuit<strong>an</strong>t dies within the Minimum Guar<strong>an</strong>tee Period, the income<br />

payments f<strong>or</strong> the bal<strong>an</strong>ce of the guar<strong>an</strong>tee period are commuted <strong>an</strong>d paid to the beneficiary in a lump sum. However, if the beneficiary <strong>is</strong> the spouse <strong>or</strong> commonlaw<br />

partner the <strong>an</strong>nuity payments continue to that person f<strong>or</strong> the bal<strong>an</strong>ce of the remaining guar<strong>an</strong>teed period. Single <strong>an</strong>d Joint & Last Surviv<strong>or</strong> <strong>Annuity</strong> Rates are as<br />

of J<strong>an</strong>uary, 2012.<br />

The Growth Fact<strong>or</strong><br />

Table C shows the impact that different rates of return c<strong>an</strong> have on both your income <strong>an</strong>d the amount of capital that<br />

will be left f<strong>or</strong> your family. Keep in mind that almost half of the value remaining in the <strong>RRIF</strong> at your death may be lost<br />

in taxes if you don’t have a surviving spouse as beneficiary.<br />

Table C:<br />

Age<br />

Effect of Interest Rates on Capital <strong>an</strong>d Income in a <strong>RRIF</strong><br />

4% Interest 6% Interest 8% Interest<br />

Capital<br />

Estimated<br />

Income<br />

Capital<br />

Estimated<br />

Income<br />

Capital<br />

Estimated<br />

Income<br />

72 $103,955 $7,779 $105,932 $7,929 $107,909 $7,964<br />

75 $92,609 $7,321 $99,925 $7,974 $107,666 $8,301<br />

80 $74,249 $6,531 $88,128 $7,965 $104,267 $8,894<br />

85 $56,307 $5,803 $73,519 $7,947 $95,513 $9,484<br />

90 $38,543 $5,122 $55,360 $7,924 $78,977 $10,038<br />

95 $20,766 $3,738 $32,812 $6,648 $51,406 $10,281<br />

99 $9,955 $900 $16,978 $1,981 $28,671 $5,734<br />

Total $151,261 $193,419 $251,448<br />

<strong>Which</strong> <strong>is</strong> <strong>Better</strong> f<strong>or</strong> Me<br />

One of the most frequently asked questions in retirement pl<strong>an</strong>ning <strong>is</strong> “<strong>Which</strong> <strong>is</strong> better f<strong>or</strong> me, a reg<strong>is</strong>tered <strong>an</strong>nuity <strong>or</strong><br />

a <strong>RRIF</strong>”. Aside from the amount of income you would receive from each, Table D provides a brief summary of other<br />

fact<strong>or</strong>s you might w<strong>an</strong>t to consider when making your dec<strong>is</strong>ion.<br />

3

<strong>Which</strong> <strong>is</strong> better: a <strong>RRIF</strong> <strong>or</strong> <strong>an</strong> <strong>an</strong>nuity<br />

Table D:<br />

<strong>Which</strong> <strong>is</strong> <strong>Better</strong> f<strong>or</strong> Me — A <strong>RRIF</strong> <strong>or</strong> <strong>an</strong> <strong>Annuity</strong><br />

<strong>RRIF</strong>s<br />

Annuities<br />

The Basics<br />

Adv<strong>an</strong>tages<br />

D<strong>is</strong>adv<strong>an</strong>tages<br />

A <strong>RRIF</strong> <strong>is</strong> basically <strong>an</strong> extension of <strong>an</strong> RRSP, with<br />

some imp<strong>or</strong>t<strong>an</strong>t differences:<br />

• Once you have converted <strong>an</strong> RRSP to a <strong>RRIF</strong>, you<br />

c<strong>an</strong>not make further contributions.<br />

• You must make withdrawals, subject to prescribed<br />

minimums, every year f<strong>or</strong> the rest of your life <strong>or</strong><br />

until all the funds in your <strong>RRIF</strong> are withdrawn.<br />

• Income payments from a <strong>RRIF</strong>, including <strong>an</strong>y<br />

additional unscheduled withdrawals are taxable<br />

income in the year received.<br />

• You retain personal control of your investments.<br />

• You c<strong>an</strong> ch<strong>an</strong>ge the amount of your income.<br />

• You c<strong>an</strong> make lump sum withdrawals at <strong>an</strong>y time.<br />

• You may outlive your <strong>RRIF</strong> income.<br />

• Your capital may dimin<strong>is</strong>h m<strong>or</strong>e quickly th<strong>an</strong><br />

pl<strong>an</strong>ned because of lump sum withdrawals <strong>or</strong><br />

po<strong>or</strong> investment perf<strong>or</strong>m<strong>an</strong>ce.<br />

• Your <strong>RRIF</strong> requires continuing investment<br />

m<strong>an</strong>agement dec<strong>is</strong>ions.<br />

An <strong>an</strong>nuity c<strong>an</strong> provide set income payments f<strong>or</strong> life<br />

<strong>or</strong> over a specific term:<br />

• In the case of <strong>an</strong> <strong>an</strong>nuity, you are purchasing<br />

a contract. In exch<strong>an</strong>ge f<strong>or</strong> a one-time deposit,<br />

you receive set guar<strong>an</strong>teed income payments<br />

over a fixed period of time <strong>or</strong> your lifetime with<br />

<strong>or</strong> without a minimum guar<strong>an</strong>tee period.<br />

• The amount of income you receive depends on<br />

a variety of fact<strong>or</strong>s such as the deposit amount,<br />

current interest rates, age <strong>an</strong>d the type of <strong>an</strong>nuity<br />

you choose.<br />

• The full amount of the <strong>an</strong>nuity payments are<br />

taxable income in the year received.<br />

• A life <strong>an</strong>nuity guar<strong>an</strong>tees that you c<strong>an</strong>not outlive<br />

your income.<br />

• Neither you n<strong>or</strong> your spouse are required to make<br />

<strong>an</strong>y investment <strong>or</strong> m<strong>an</strong>agement dec<strong>is</strong>ions — the<br />

insur<strong>an</strong>ce comp<strong>an</strong>y assumes the investment r<strong>is</strong>k.<br />

• You c<strong>an</strong> spend every income payment without<br />

w<strong>or</strong>ry because your future income <strong>is</strong> guar<strong>an</strong>teed.<br />

• Most <strong>an</strong>nuities c<strong>an</strong>not be surrendered <strong>or</strong> altered<br />

after income has commenced.<br />

• Payments c<strong>an</strong>not be adjusted to reflect<br />

ch<strong>an</strong>ging needs.<br />

Seek Unbiased Advice<br />

If you decide that a reg<strong>is</strong>tered <strong>an</strong>nuity might be a good idea, then ensure you consult someone who sells both<br />

<strong>an</strong>nuities <strong>an</strong>d <strong>RRIF</strong>s, otherw<strong>is</strong>e, you may get only part of the st<strong>or</strong>y. <strong>RRIF</strong>s are sold by most, if not all, fin<strong>an</strong>cial institutions<br />

but life <strong>an</strong>nuities (where the income <strong>is</strong> guar<strong>an</strong>teed f<strong>or</strong> your lifetime regardless of how long you live), are available only<br />

from life insur<strong>an</strong>ce comp<strong>an</strong>ies. You may feel that you’re not likely to live beyond age 90, but why take the ch<strong>an</strong>ce<br />

A life <strong>an</strong>nuity guar<strong>an</strong>tees that you c<strong>an</strong>not outlive your income. Annuities provide set income payments f<strong>or</strong> life.<br />

The inf<strong>or</strong>mation in th<strong>is</strong> document <strong>is</strong> based on the facts as presented. Any differences, including fact<strong>or</strong>s such as assumed growth rates, age, marital status, type <strong>an</strong>d/<br />

<strong>or</strong> source of income c<strong>an</strong> ch<strong>an</strong>ge the inf<strong>or</strong>mation provided in the various tables dramatically. In addition, th<strong>is</strong> document may not be complete in <strong>an</strong>y expl<strong>an</strong>ation of<br />

applicable tax rules as they apply to your personal situation.<br />

Past perf<strong>or</strong>m<strong>an</strong>ce <strong>is</strong> no guar<strong>an</strong>tee of future perf<strong>or</strong>m<strong>an</strong>ce. The inf<strong>or</strong>mation in th<strong>is</strong> document <strong>is</strong> f<strong>or</strong> general inf<strong>or</strong>mation purposes only <strong>an</strong>d <strong>is</strong> not to be construed<br />

as providing legal, tax, fin<strong>an</strong>cial <strong>or</strong> professional advice. The <strong>Empire</strong> <strong>Life</strong> Insur<strong>an</strong>ce Comp<strong>an</strong>y assumes no responsibility f<strong>or</strong> <strong>an</strong>y reli<strong>an</strong>ce made on <strong>or</strong> m<strong>is</strong>use <strong>or</strong><br />

om<strong>is</strong>sions of the inf<strong>or</strong>mation contained in th<strong>is</strong> document. Please seek professional advice bef<strong>or</strong>e making <strong>an</strong>y dec<strong>is</strong>ion.<br />

A description of the key features of the individual variable insur<strong>an</strong>ce contract <strong>is</strong> contained in the Inf<strong>or</strong>mation Folder f<strong>or</strong> the product being considered. Any amount<br />

that <strong>is</strong> allocated to a segregated fund <strong>is</strong> invested at the r<strong>is</strong>k of the contract owner <strong>an</strong>d may increase <strong>or</strong> decrease in value.<br />

®<br />

Reg<strong>is</strong>tered trademark of The <strong>Empire</strong> <strong>Life</strong> Insur<strong>an</strong>ce Comp<strong>an</strong>y. Policies are <strong>is</strong>sued by The <strong>Empire</strong> <strong>Life</strong> Insur<strong>an</strong>ce Comp<strong>an</strong>y.<br />

Investments • Insur<strong>an</strong>ce • Group solutions<br />

www.empire.ca info@empire.ca<br />

ENG-02/13