Kenya Power UPDEA me..

Kenya Power UPDEA me..

Kenya Power UPDEA me..

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

3/1/2012<br />

<strong>Kenya</strong> <strong>Power</strong>’s Experiences and<br />

Challenges as a single off-taker<br />

in the <strong>Power</strong> Sector<br />

Presentation to the <strong>UPDEA</strong><br />

Scientific Committee Meeting<br />

By<br />

Eng. Joseph K. Njoroge, MBS,<br />

Managing Director & CEO<br />

<strong>Kenya</strong> <strong>Power</strong> & Lighting Co. Ltd.<br />

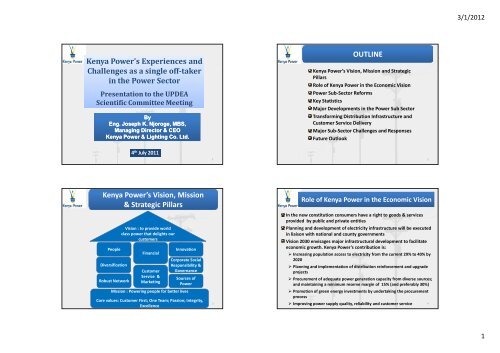

OUTLINE<br />

<strong>Kenya</strong> <strong>Power</strong>’s Vision, Mission and Strategic<br />

Pillars<br />

Role of <strong>Kenya</strong> <strong>Power</strong> in the Economic Vision<br />

<strong>Power</strong> Sub-Sector Reforms<br />

Key Statistics<br />

Major Develop<strong>me</strong>nts in the <strong>Power</strong> Sub Sector<br />

Transforming Distribution Infrastructure and<br />

Custo<strong>me</strong>r Service Delivery<br />

Major Sub-Sector Challenges and Responses<br />

Future Outlook<br />

4 th July 2011<br />

1<br />

2<br />

<strong>Kenya</strong> <strong>Power</strong>’s Vision, Mission<br />

& Strategic Pillars<br />

People<br />

Diversification<br />

Robust Network<br />

Vision : to provide world<br />

class power that delights our<br />

custo<strong>me</strong>rs<br />

Financial<br />

Custo<strong>me</strong>r<br />

Service &<br />

Marketing<br />

Innovation<br />

Corporate Social<br />

Responsibility &<br />

Governance<br />

Sources of<br />

<strong>Power</strong><br />

Mission : <strong>Power</strong>ing people for better lives<br />

Core values: Custo<strong>me</strong>r First; One Team; Passion; Integrity,<br />

Excellence<br />

3<br />

Role of <strong>Kenya</strong> <strong>Power</strong> in the Economic Vision<br />

In the new constitution consu<strong>me</strong>rs have a right to goods & services<br />

provided by public and private entities<br />

Planning and develop<strong>me</strong>nt of electricity infrastructure will be executed<br />

in liaison with national and county govern<strong>me</strong>nts<br />

Vision 2030 envisages major infrastructural develop<strong>me</strong>nt to facilitate<br />

economic growth. <strong>Kenya</strong> <strong>Power</strong>’s contribution is:<br />

Increasing population access to electricity from the current 29% to 40% by<br />

2020<br />

Planning and imple<strong>me</strong>ntation of distribution reinforce<strong>me</strong>nt and upgrade<br />

projects<br />

Procure<strong>me</strong>nt of adequate power generation capacity from diverse sources;<br />

and maintaining a minimum reserve margin of 15% (and preferably 30%)<br />

Promotion of green energy invest<strong>me</strong>nts by undertaking the procure<strong>me</strong>nt<br />

process<br />

Improving power supply quality, reliability and custo<strong>me</strong>r service 4<br />

1

3/1/2012<br />

Refor<strong>me</strong>d Electricity Sub-sector Structure<br />

Refor<strong>me</strong>d Electricity Regulatory Environ<strong>me</strong>nt<br />

Companies Act (Cap 486)<br />

Nairobi Stock<br />

Exchange Listing<br />

Rules<br />

State Corporations Act<br />

KPLC<br />

The New<br />

Constitution of<br />

<strong>Kenya</strong><br />

ERC Regulations<br />

Cities<br />

& Counties<br />

Capital<br />

Markets<br />

Authority Act<br />

Public<br />

Procure<strong>me</strong>nt &<br />

Disposal Act<br />

Environ<strong>me</strong>nt Grid Code<br />

Manage<strong>me</strong>nt &<br />

Coordination Act<br />

Energy Act<br />

2006<br />

5<br />

6<br />

Key Statistics<br />

Installed capacity MW (May 2011) 1,599.9<br />

Available Generation Capacity MW (May2011) 1,359.2<br />

System Peak Demand MW to date* (10 th May 2011) 1,191.03<br />

Forecasted unconstrained demand MW 1,290<br />

Reserve Margin % (May 2011) * 5.1%<br />

Energy Purchased 2009/10 (GWh) 6,692<br />

Total Sales 2009/10 (GWh) 5,624<br />

Sales % of Energy Purchased 2009/10 84.0%<br />

Losses as % of Energy Purchased 2009/10 16.0%<br />

Transmission and Distribution Lines, Circuit Length in<br />

Kilo<strong>me</strong>ters (11kV to 220kV) 47,347<br />

Number of Custo<strong>me</strong>rs (May 2011) 1,720,868<br />

Population Electricity Access 29%<br />

Note: Reserve margin is thin at 5.1% as compared to the ideal of 15%. About<br />

112MW of demand is not being <strong>me</strong>t due to insufficient generation capacity,<br />

currently occasioned by poor hydrology 7<br />

Major Develop<strong>me</strong>nts Underway in the <strong>Power</strong><br />

Subsector<br />

Recent creation of REA, Ketraco and GDC<br />

New Energy Scale Up Program targeting 1million new households<br />

over 5 yrs at cost of KShs. 84 billion<br />

Planned East African Regional Interconnection projects e.g.<br />

Connection to Tanzania , Ethiopia and 2 nd Uganda line totaling 1,780<br />

kms at an estimated cost of US$ 876 million<br />

38 committed transmission projects totaling 3,697 kms and 2,421<br />

MVA of substation capacity being developed within the country<br />

between 2011 and 2015 at an estimated US$ 482 million,<br />

Public private partnership fra<strong>me</strong>work to facilitate procure<strong>me</strong>nt of<br />

new projects that aug<strong>me</strong>nt capacity e.g. geothermal, thermal, wind<br />

Green energy invest<strong>me</strong>nts through Feed-in-Tariff<br />

A total of 1,789.6MW of new generation capacity is being developed<br />

between 2011 and 2015 out of which 857MW will be green energy<br />

(hydro, geothermal and wind), 732MW of new thermal plant (MS<br />

Diesel and coal) and 200MW of imports.<br />

8<br />

2

3/1/2012<br />

20 000<br />

18 000<br />

16 000<br />

14 000<br />

12 000<br />

10 000<br />

8 000<br />

PROJECTED NATIONAL SUPPLY AND DEMAND<br />

– 2011 to 2030<br />

In 2020 <strong>Kenya</strong> must have at<br />

least 40% population access to<br />

electricity to reach the Vision<br />

2030 target<br />

Total Capacity (MW)<br />

Peak Demand (MW)<br />

8 226<br />

Vision 2030<br />

demand<br />

Forecast of 8-10 %<br />

17 764<br />

12 141<br />

10 097<br />

15 066<br />

Significant generation<br />

potential<br />

Geothermal(~ 7,000MW);<br />

Hydro (~1,500MW);<br />

Wind (~4,400 MW); and<br />

TRANSFORMING DISTRIBUTION<br />

INFRASTRUCTURE AND CUSTOMER SERVICE<br />

DELIVERY<br />

6 000<br />

4 000<br />

2 000<br />

0<br />

1,229<br />

1,107<br />

2010<br />

2011<br />

2012<br />

2009/10<br />

3 141<br />

2 038<br />

2014/15<br />

4 659<br />

3 474<br />

6 768<br />

2018/19 2023/24 2026/27 2029/30<br />

2013<br />

2014<br />

2015<br />

2016<br />

2017<br />

2018<br />

2019<br />

2020<br />

2021<br />

2022<br />

2023<br />

2024<br />

2025<br />

2026<br />

2027<br />

2028<br />

2029<br />

2030<br />

Potentially Coal and Gas.<br />

• 15% Reserve Margin<br />

Vision 2030 ~<br />

Projected Demand<br />

15,000MW<br />

Source: Update of <strong>Kenya</strong>’s Least Cost <strong>Power</strong> Develop<strong>me</strong>nt Plan 2010-2030 9<br />

10<br />

Distribution Expansion Plan Under<br />

Imple<strong>me</strong>ntation 2010/11 to 2014/15<br />

To connect over 1 million new custo<strong>me</strong>rs spread<br />

countrywide every 5 years.<br />

Construction of an additional approximately :<br />

16,000 kms of Medium Voltage distribution lines,<br />

1,000 MVA of distribution substations,<br />

50,000 kms of LV distribution lines,<br />

30,000 (3,000 MVA) of distribution transfor<strong>me</strong>rs and<br />

1 million service lines connections<br />

11<br />

Distribution Infrastructure Invest<strong>me</strong>nt Funding<br />

Since 2005 to date, a total of US$ 480 Million (Kshs 38.4 billion) has been mobilised to<br />

improve distribution infrastructure as follows:<br />

PROJECT FINANCIER AMOUNT PROJECT COMPONENTS OBJECTIVES<br />

Energy Sector Recovery Project<br />

(2005 to 2012)<br />

•IDA–US$111.5m<br />

•EIB–Euro51m<br />

•AFD–Euro25m<br />

•NDF–Euro10m<br />

•KPLC–US$34m<br />

<strong>Kenya</strong> Electricity Expansion<br />

Project (2010 to 2015) (IDA US<br />

$102.2 mill , KPLC US$ 29.8mill)<br />

Rights Issue Funding (2011 to<br />

2013) (KPLC)<br />

US$ 233<br />

million<br />

US$ 132<br />

million<br />

KShs. 9.2<br />

billion<br />

•Completed 25 substations,<br />

1,250 kms of fibre optic, 540<br />

kms of 66,33 & 11 kV<br />

distribution lines, procured<br />

406,000 static energy <strong>me</strong>ters,<br />

and installed Mt. <strong>Kenya</strong> Radio<br />

System.<br />

•Works ongoing at 26<br />

substations, 465 kms of lines<br />

and SCADA/EMS system.<br />

To date, US $ 102 million has<br />

been disbursed.<br />

Procuring 26 substations, 1400<br />

kms MV lines and prepaid<br />

<strong>me</strong>ters<br />

Procuring 17 Distribution<br />

substations, 4 transmission<br />

substations, 300,000 prepaid<br />

<strong>me</strong>ters<br />

•Enhanced access to<br />

electricity<br />

•Capacity<br />

enhance<strong>me</strong>nt<br />

•Supply reliability &<br />

power quality<br />

improve<strong>me</strong>nt<br />

•Revenue<br />

enhance<strong>me</strong>nt &<br />

protection<br />

•Enhanced custo<strong>me</strong>r<br />

satisfaction<br />

12<br />

3

3/1/2012<br />

3 500 000<br />

3 000 000<br />

2 500 000<br />

2 000 000<br />

1 500 000<br />

1 000 000<br />

500 000<br />

-<br />

Total Number of Custo<strong>me</strong>rs<br />

Projected<br />

2 000 000<br />

1 720 868<br />

3 000 000<br />

In order to address critical electricity supply quality service challenges facing the<br />

company the following new projects are being imple<strong>me</strong>nted in the period 2010/11 to<br />

2015/16:<br />

Project Objective Status<br />

1. Distribution Master Plan Plan for comprehensive improve<strong>me</strong>nt Tendered<br />

to the entire distribution network<br />

2. Under grounding of electricity To reduce electricity line break downs In progress<br />

lines<br />

in urban centres as well as to enhance<br />

public safety<br />

3. Automation Extension of new technologies such as Pilot projects in<br />

smart grid, so as to improve Nairobi and<br />

performance of the electricity network Mombasa in<br />

progress<br />

4. Auto changeovers Installation of more efficient load<br />

switching equip<strong>me</strong>nt<br />

In progress<br />

5. Dry Type Transfor<strong>me</strong>rs and<br />

Intruder Alarms<br />

6. Joint Venture Transfor<strong>me</strong>r<br />

Factory<br />

Distribution Strategic Initiatives<br />

Change from oil type to dry type<br />

transfor<strong>me</strong>rs that are less prone to<br />

vandalism<br />

Initiate manufacturing of transfor<strong>me</strong>rs<br />

locally in a joint venture arrange<strong>me</strong>nt.<br />

Alarms being<br />

installed<br />

Tendered<br />

13<br />

14<br />

Project Objective Status<br />

7. Reactive<br />

<strong>Power</strong><br />

Compensation<br />

8.Aerial Bundled<br />

Conductors<br />

To improve voltages and<br />

harmonics through installation of<br />

capacitors and other equip<strong>me</strong>nt.<br />

Use of Aerial Bundled Conductors<br />

in urban areas or where there is<br />

heavy vegetation, as they require<br />

much less maintenance work<br />

In progress<br />

Tendered and expected to cost<br />

about Shs 3 billion<br />

9. Concrete Poles Increased use of concrete poles in 26,300 concrete poles received<br />

power line construction leading to from the supplier to date out of<br />

fewer faults and less maintenance which 16,104 have been used<br />

10. Change to<br />

Smart Grid<br />

System<br />

Distribution Strategic Initiatives contd.<br />

To realize a grid which has<br />

communication linkages between<br />

custo<strong>me</strong>rs and system operators.<br />

To improve service delivery,<br />

efficiency and effectiveness in<br />

operations. Will facilitate<br />

leveraging of assets.<br />

Prepaid <strong>me</strong>tering being done with<br />

adaptable <strong>me</strong>ters, fibre optic<br />

installation being done in so<strong>me</strong><br />

parts of the system<br />

15<br />

Custo<strong>me</strong>r Service Strategic Initiatives<br />

Effectively collect revenue while providing efficient and high quality<br />

custo<strong>me</strong>r handling services. KPLC has developed a core competence of<br />

consistently achieving over 98% revenue collection as percent of billing<br />

Action<br />

Ti<strong>me</strong> Fra<strong>me</strong><br />

i. Automatic Meter Reading (AMR) project Pilot 2008/9<br />

Roll-out 2009/10 to<br />

2014/15<br />

ii. Prepaid Meters Pilot Rollout project to retrofit Pilot 2009/10<br />

250,000 per year small to <strong>me</strong>dium custo<strong>me</strong>rs.<br />

Install 200,000 <strong>me</strong>ters per year for new Roll-out 2010/11 to<br />

custo<strong>me</strong>rs<br />

2014/15<br />

iii. Smart <strong>me</strong>tering for 100,000 do<strong>me</strong>stic and Roll-out 2010/11 to<br />

small com<strong>me</strong>rcial custo<strong>me</strong>r<br />

2014/15<br />

iv. Use feeder <strong>me</strong>tering and transfor<strong>me</strong>r ring Roll-out 2009/10 to<br />

fencing to guide and monitor loss campaigns 2014/15<br />

v. Improve supply to people settle<strong>me</strong>nts Roll-out 2010/11 to<br />

2014/15<br />

16<br />

4

3/1/2012<br />

Threat<br />

1. Electricity theft & vandalism of<br />

infrastructure<br />

2. Sufficiency of Generation Capacity<br />

(delays due to protracted negotiations<br />

and lack of guarantees).<br />

3. Vagaries of weather including drought<br />

and floods.<br />

4. Affordability of power (new<br />

connections, tariffs, fuel costs)<br />

5. Right of Way for power infrastructure<br />

(levies, encroach<strong>me</strong>nt, etc.)<br />

MAJOR SUB-SECTORAL SECTORAL CHALLENGES<br />

Mitigation<br />

• Dry type transfor<strong>me</strong>rs, intruder alarms,<br />

relocation of transfor<strong>me</strong>rs, etc .<br />

• Community policing, public education<br />

• Lobbying for stiff penalties for infrastructure<br />

vandals<br />

• E<strong>me</strong>rgency generation<br />

• Raising reserve margin<br />

• Fast tracking so<strong>me</strong> projects<br />

• Projects under Feed In Tariffs policy<br />

• Diversify generation sources<br />

• Regional Interconnection<br />

• Least Cost Generation Planning<br />

• Promoting green energy sources<br />

• Credit facilities to custo<strong>me</strong>rs for connection<br />

costs<br />

• Public Education<br />

• Engaging local authorities<br />

6. Uncoordinated urban planning. • Engaging local authorities, Govern<strong>me</strong>nt urban<br />

17<br />

planners and other infrastructural developers<br />

FUTURE OUTLOOK<br />

Strategies for <strong>me</strong>eting demand going forward are in place.<br />

Support from develop<strong>me</strong>nt partners for network<br />

infrastructural invest<strong>me</strong>nt program in place – <strong>Kenya</strong> <strong>Power</strong>’s<br />

contribution also in place.<br />

Favorable operating environ<strong>me</strong>nt is expected from a vibrant<br />

economy.<br />

Accelerated economic activity is expected from large scale<br />

expansion of infrastructure.<br />

Revised legislation to imple<strong>me</strong>nt the new constitution will lead<br />

to :<br />

Better streamlining of stakeholder interests in power<br />

supply<br />

Clearer invest<strong>me</strong>nt boundaries for players in the electricity<br />

subsector<br />

18<br />

THANK YOU<br />

19<br />

5