Kenya Power UPDEA me..

Kenya Power UPDEA me..

Kenya Power UPDEA me..

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

3/1/2012<br />

<strong>Kenya</strong> <strong>Power</strong>’s Experiences and<br />

Challenges as a single off-taker<br />

in the <strong>Power</strong> Sector<br />

Presentation to the <strong>UPDEA</strong><br />

Scientific Committee Meeting<br />

By<br />

Eng. Joseph K. Njoroge, MBS,<br />

Managing Director & CEO<br />

<strong>Kenya</strong> <strong>Power</strong> & Lighting Co. Ltd.<br />

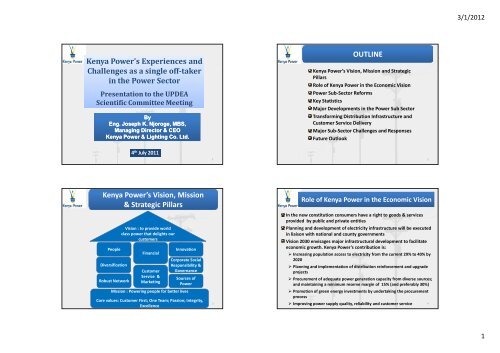

OUTLINE<br />

<strong>Kenya</strong> <strong>Power</strong>’s Vision, Mission and Strategic<br />

Pillars<br />

Role of <strong>Kenya</strong> <strong>Power</strong> in the Economic Vision<br />

<strong>Power</strong> Sub-Sector Reforms<br />

Key Statistics<br />

Major Develop<strong>me</strong>nts in the <strong>Power</strong> Sub Sector<br />

Transforming Distribution Infrastructure and<br />

Custo<strong>me</strong>r Service Delivery<br />

Major Sub-Sector Challenges and Responses<br />

Future Outlook<br />

4 th July 2011<br />

1<br />

2<br />

<strong>Kenya</strong> <strong>Power</strong>’s Vision, Mission<br />

& Strategic Pillars<br />

People<br />

Diversification<br />

Robust Network<br />

Vision : to provide world<br />

class power that delights our<br />

custo<strong>me</strong>rs<br />

Financial<br />

Custo<strong>me</strong>r<br />

Service &<br />

Marketing<br />

Innovation<br />

Corporate Social<br />

Responsibility &<br />

Governance<br />

Sources of<br />

<strong>Power</strong><br />

Mission : <strong>Power</strong>ing people for better lives<br />

Core values: Custo<strong>me</strong>r First; One Team; Passion; Integrity,<br />

Excellence<br />

3<br />

Role of <strong>Kenya</strong> <strong>Power</strong> in the Economic Vision<br />

In the new constitution consu<strong>me</strong>rs have a right to goods & services<br />

provided by public and private entities<br />

Planning and develop<strong>me</strong>nt of electricity infrastructure will be executed<br />

in liaison with national and county govern<strong>me</strong>nts<br />

Vision 2030 envisages major infrastructural develop<strong>me</strong>nt to facilitate<br />

economic growth. <strong>Kenya</strong> <strong>Power</strong>’s contribution is:<br />

Increasing population access to electricity from the current 29% to 40% by<br />

2020<br />

Planning and imple<strong>me</strong>ntation of distribution reinforce<strong>me</strong>nt and upgrade<br />

projects<br />

Procure<strong>me</strong>nt of adequate power generation capacity from diverse sources;<br />

and maintaining a minimum reserve margin of 15% (and preferably 30%)<br />

Promotion of green energy invest<strong>me</strong>nts by undertaking the procure<strong>me</strong>nt<br />

process<br />

Improving power supply quality, reliability and custo<strong>me</strong>r service 4<br />

1

3/1/2012<br />

Refor<strong>me</strong>d Electricity Sub-sector Structure<br />

Refor<strong>me</strong>d Electricity Regulatory Environ<strong>me</strong>nt<br />

Companies Act (Cap 486)<br />

Nairobi Stock<br />

Exchange Listing<br />

Rules<br />

State Corporations Act<br />

KPLC<br />

The New<br />

Constitution of<br />

<strong>Kenya</strong><br />

ERC Regulations<br />

Cities<br />

& Counties<br />

Capital<br />

Markets<br />

Authority Act<br />

Public<br />

Procure<strong>me</strong>nt &<br />

Disposal Act<br />

Environ<strong>me</strong>nt Grid Code<br />

Manage<strong>me</strong>nt &<br />

Coordination Act<br />

Energy Act<br />

2006<br />

5<br />

6<br />

Key Statistics<br />

Installed capacity MW (May 2011) 1,599.9<br />

Available Generation Capacity MW (May2011) 1,359.2<br />

System Peak Demand MW to date* (10 th May 2011) 1,191.03<br />

Forecasted unconstrained demand MW 1,290<br />

Reserve Margin % (May 2011) * 5.1%<br />

Energy Purchased 2009/10 (GWh) 6,692<br />

Total Sales 2009/10 (GWh) 5,624<br />

Sales % of Energy Purchased 2009/10 84.0%<br />

Losses as % of Energy Purchased 2009/10 16.0%<br />

Transmission and Distribution Lines, Circuit Length in<br />

Kilo<strong>me</strong>ters (11kV to 220kV) 47,347<br />

Number of Custo<strong>me</strong>rs (May 2011) 1,720,868<br />

Population Electricity Access 29%<br />

Note: Reserve margin is thin at 5.1% as compared to the ideal of 15%. About<br />

112MW of demand is not being <strong>me</strong>t due to insufficient generation capacity,<br />

currently occasioned by poor hydrology 7<br />

Major Develop<strong>me</strong>nts Underway in the <strong>Power</strong><br />

Subsector<br />

Recent creation of REA, Ketraco and GDC<br />

New Energy Scale Up Program targeting 1million new households<br />

over 5 yrs at cost of KShs. 84 billion<br />

Planned East African Regional Interconnection projects e.g.<br />

Connection to Tanzania , Ethiopia and 2 nd Uganda line totaling 1,780<br />

kms at an estimated cost of US$ 876 million<br />

38 committed transmission projects totaling 3,697 kms and 2,421<br />

MVA of substation capacity being developed within the country<br />

between 2011 and 2015 at an estimated US$ 482 million,<br />

Public private partnership fra<strong>me</strong>work to facilitate procure<strong>me</strong>nt of<br />

new projects that aug<strong>me</strong>nt capacity e.g. geothermal, thermal, wind<br />

Green energy invest<strong>me</strong>nts through Feed-in-Tariff<br />

A total of 1,789.6MW of new generation capacity is being developed<br />

between 2011 and 2015 out of which 857MW will be green energy<br />

(hydro, geothermal and wind), 732MW of new thermal plant (MS<br />

Diesel and coal) and 200MW of imports.<br />

8<br />

2

3/1/2012<br />

20 000<br />

18 000<br />

16 000<br />

14 000<br />

12 000<br />

10 000<br />

8 000<br />

PROJECTED NATIONAL SUPPLY AND DEMAND<br />

– 2011 to 2030<br />

In 2020 <strong>Kenya</strong> must have at<br />

least 40% population access to<br />

electricity to reach the Vision<br />

2030 target<br />

Total Capacity (MW)<br />

Peak Demand (MW)<br />

8 226<br />

Vision 2030<br />

demand<br />

Forecast of 8-10 %<br />

17 764<br />

12 141<br />

10 097<br />

15 066<br />

Significant generation<br />

potential<br />

Geothermal(~ 7,000MW);<br />

Hydro (~1,500MW);<br />

Wind (~4,400 MW); and<br />

TRANSFORMING DISTRIBUTION<br />

INFRASTRUCTURE AND CUSTOMER SERVICE<br />

DELIVERY<br />

6 000<br />

4 000<br />

2 000<br />

0<br />

1,229<br />

1,107<br />

2010<br />

2011<br />

2012<br />

2009/10<br />

3 141<br />

2 038<br />

2014/15<br />

4 659<br />

3 474<br />

6 768<br />

2018/19 2023/24 2026/27 2029/30<br />

2013<br />

2014<br />

2015<br />

2016<br />

2017<br />

2018<br />

2019<br />

2020<br />

2021<br />

2022<br />

2023<br />

2024<br />

2025<br />

2026<br />

2027<br />

2028<br />

2029<br />

2030<br />

Potentially Coal and Gas.<br />

• 15% Reserve Margin<br />

Vision 2030 ~<br />

Projected Demand<br />

15,000MW<br />

Source: Update of <strong>Kenya</strong>’s Least Cost <strong>Power</strong> Develop<strong>me</strong>nt Plan 2010-2030 9<br />

10<br />

Distribution Expansion Plan Under<br />

Imple<strong>me</strong>ntation 2010/11 to 2014/15<br />

To connect over 1 million new custo<strong>me</strong>rs spread<br />

countrywide every 5 years.<br />

Construction of an additional approximately :<br />

16,000 kms of Medium Voltage distribution lines,<br />

1,000 MVA of distribution substations,<br />

50,000 kms of LV distribution lines,<br />

30,000 (3,000 MVA) of distribution transfor<strong>me</strong>rs and<br />

1 million service lines connections<br />

11<br />

Distribution Infrastructure Invest<strong>me</strong>nt Funding<br />

Since 2005 to date, a total of US$ 480 Million (Kshs 38.4 billion) has been mobilised to<br />

improve distribution infrastructure as follows:<br />

PROJECT FINANCIER AMOUNT PROJECT COMPONENTS OBJECTIVES<br />

Energy Sector Recovery Project<br />

(2005 to 2012)<br />

•IDA–US$111.5m<br />

•EIB–Euro51m<br />

•AFD–Euro25m<br />

•NDF–Euro10m<br />

•KPLC–US$34m<br />

<strong>Kenya</strong> Electricity Expansion<br />

Project (2010 to 2015) (IDA US<br />

$102.2 mill , KPLC US$ 29.8mill)<br />

Rights Issue Funding (2011 to<br />

2013) (KPLC)<br />

US$ 233<br />

million<br />

US$ 132<br />

million<br />

KShs. 9.2<br />

billion<br />

•Completed 25 substations,<br />

1,250 kms of fibre optic, 540<br />

kms of 66,33 & 11 kV<br />

distribution lines, procured<br />

406,000 static energy <strong>me</strong>ters,<br />

and installed Mt. <strong>Kenya</strong> Radio<br />

System.<br />

•Works ongoing at 26<br />

substations, 465 kms of lines<br />

and SCADA/EMS system.<br />

To date, US $ 102 million has<br />

been disbursed.<br />

Procuring 26 substations, 1400<br />

kms MV lines and prepaid<br />

<strong>me</strong>ters<br />

Procuring 17 Distribution<br />

substations, 4 transmission<br />

substations, 300,000 prepaid<br />

<strong>me</strong>ters<br />

•Enhanced access to<br />

electricity<br />

•Capacity<br />

enhance<strong>me</strong>nt<br />

•Supply reliability &<br />

power quality<br />

improve<strong>me</strong>nt<br />

•Revenue<br />

enhance<strong>me</strong>nt &<br />

protection<br />

•Enhanced custo<strong>me</strong>r<br />

satisfaction<br />

12<br />

3

3/1/2012<br />

3 500 000<br />

3 000 000<br />

2 500 000<br />

2 000 000<br />

1 500 000<br />

1 000 000<br />

500 000<br />

-<br />

Total Number of Custo<strong>me</strong>rs<br />

Projected<br />

2 000 000<br />

1 720 868<br />

3 000 000<br />

In order to address critical electricity supply quality service challenges facing the<br />

company the following new projects are being imple<strong>me</strong>nted in the period 2010/11 to<br />

2015/16:<br />

Project Objective Status<br />

1. Distribution Master Plan Plan for comprehensive improve<strong>me</strong>nt Tendered<br />

to the entire distribution network<br />

2. Under grounding of electricity To reduce electricity line break downs In progress<br />

lines<br />

in urban centres as well as to enhance<br />

public safety<br />

3. Automation Extension of new technologies such as Pilot projects in<br />

smart grid, so as to improve Nairobi and<br />

performance of the electricity network Mombasa in<br />

progress<br />

4. Auto changeovers Installation of more efficient load<br />

switching equip<strong>me</strong>nt<br />

In progress<br />

5. Dry Type Transfor<strong>me</strong>rs and<br />

Intruder Alarms<br />

6. Joint Venture Transfor<strong>me</strong>r<br />

Factory<br />

Distribution Strategic Initiatives<br />

Change from oil type to dry type<br />

transfor<strong>me</strong>rs that are less prone to<br />

vandalism<br />

Initiate manufacturing of transfor<strong>me</strong>rs<br />

locally in a joint venture arrange<strong>me</strong>nt.<br />

Alarms being<br />

installed<br />

Tendered<br />

13<br />

14<br />

Project Objective Status<br />

7. Reactive<br />

<strong>Power</strong><br />

Compensation<br />

8.Aerial Bundled<br />

Conductors<br />

To improve voltages and<br />

harmonics through installation of<br />

capacitors and other equip<strong>me</strong>nt.<br />

Use of Aerial Bundled Conductors<br />

in urban areas or where there is<br />

heavy vegetation, as they require<br />

much less maintenance work<br />

In progress<br />

Tendered and expected to cost<br />

about Shs 3 billion<br />

9. Concrete Poles Increased use of concrete poles in 26,300 concrete poles received<br />

power line construction leading to from the supplier to date out of<br />

fewer faults and less maintenance which 16,104 have been used<br />

10. Change to<br />

Smart Grid<br />

System<br />

Distribution Strategic Initiatives contd.<br />

To realize a grid which has<br />

communication linkages between<br />

custo<strong>me</strong>rs and system operators.<br />

To improve service delivery,<br />

efficiency and effectiveness in<br />

operations. Will facilitate<br />

leveraging of assets.<br />

Prepaid <strong>me</strong>tering being done with<br />

adaptable <strong>me</strong>ters, fibre optic<br />

installation being done in so<strong>me</strong><br />

parts of the system<br />

15<br />

Custo<strong>me</strong>r Service Strategic Initiatives<br />

Effectively collect revenue while providing efficient and high quality<br />

custo<strong>me</strong>r handling services. KPLC has developed a core competence of<br />

consistently achieving over 98% revenue collection as percent of billing<br />

Action<br />

Ti<strong>me</strong> Fra<strong>me</strong><br />

i. Automatic Meter Reading (AMR) project Pilot 2008/9<br />

Roll-out 2009/10 to<br />

2014/15<br />

ii. Prepaid Meters Pilot Rollout project to retrofit Pilot 2009/10<br />

250,000 per year small to <strong>me</strong>dium custo<strong>me</strong>rs.<br />

Install 200,000 <strong>me</strong>ters per year for new Roll-out 2010/11 to<br />

custo<strong>me</strong>rs<br />

2014/15<br />

iii. Smart <strong>me</strong>tering for 100,000 do<strong>me</strong>stic and Roll-out 2010/11 to<br />

small com<strong>me</strong>rcial custo<strong>me</strong>r<br />

2014/15<br />

iv. Use feeder <strong>me</strong>tering and transfor<strong>me</strong>r ring Roll-out 2009/10 to<br />

fencing to guide and monitor loss campaigns 2014/15<br />

v. Improve supply to people settle<strong>me</strong>nts Roll-out 2010/11 to<br />

2014/15<br />

16<br />

4

3/1/2012<br />

Threat<br />

1. Electricity theft & vandalism of<br />

infrastructure<br />

2. Sufficiency of Generation Capacity<br />

(delays due to protracted negotiations<br />

and lack of guarantees).<br />

3. Vagaries of weather including drought<br />

and floods.<br />

4. Affordability of power (new<br />

connections, tariffs, fuel costs)<br />

5. Right of Way for power infrastructure<br />

(levies, encroach<strong>me</strong>nt, etc.)<br />

MAJOR SUB-SECTORAL SECTORAL CHALLENGES<br />

Mitigation<br />

• Dry type transfor<strong>me</strong>rs, intruder alarms,<br />

relocation of transfor<strong>me</strong>rs, etc .<br />

• Community policing, public education<br />

• Lobbying for stiff penalties for infrastructure<br />

vandals<br />

• E<strong>me</strong>rgency generation<br />

• Raising reserve margin<br />

• Fast tracking so<strong>me</strong> projects<br />

• Projects under Feed In Tariffs policy<br />

• Diversify generation sources<br />

• Regional Interconnection<br />

• Least Cost Generation Planning<br />

• Promoting green energy sources<br />

• Credit facilities to custo<strong>me</strong>rs for connection<br />

costs<br />

• Public Education<br />

• Engaging local authorities<br />

6. Uncoordinated urban planning. • Engaging local authorities, Govern<strong>me</strong>nt urban<br />

17<br />

planners and other infrastructural developers<br />

FUTURE OUTLOOK<br />

Strategies for <strong>me</strong>eting demand going forward are in place.<br />

Support from develop<strong>me</strong>nt partners for network<br />

infrastructural invest<strong>me</strong>nt program in place – <strong>Kenya</strong> <strong>Power</strong>’s<br />

contribution also in place.<br />

Favorable operating environ<strong>me</strong>nt is expected from a vibrant<br />

economy.<br />

Accelerated economic activity is expected from large scale<br />

expansion of infrastructure.<br />

Revised legislation to imple<strong>me</strong>nt the new constitution will lead<br />

to :<br />

Better streamlining of stakeholder interests in power<br />

supply<br />

Clearer invest<strong>me</strong>nt boundaries for players in the electricity<br />

subsector<br />

18<br />

THANK YOU<br />

19<br />

5