The future of IFRSs in Europe

Since the adoption of the IAS Regulation in 2002, the International Financial Reporting Standards (IFRSs) have served as the authoritative accounting rules for publicly traded companies in the European Union.

Since the adoption of the IAS Regulation in 2002, the International Financial Reporting Standards (IFRSs) have served as the authoritative accounting rules for publicly traded companies in the European Union.

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

ankenverband<br />

Commission launched a fundamental structural review<br />

<strong>in</strong> 2013. Second, the Lisbon Treaty <strong>of</strong> 1 December 2009<br />

grants greater powers to the <strong>Europe</strong>an Parliament<br />

and provides for greater <strong>in</strong>volvement <strong>of</strong> the national<br />

parliaments.<br />

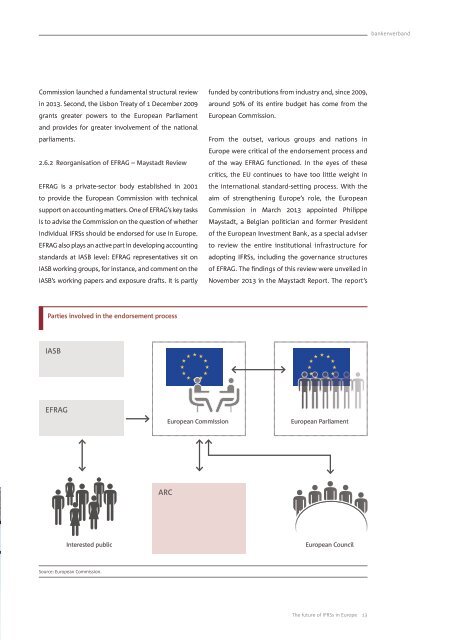

2.6.2 Reorganisation <strong>of</strong> EFRAG – Maystadt Review<br />

EFRAG is a private-sector body established <strong>in</strong> 2001<br />

to provide the <strong>Europe</strong>an Commission with technical<br />

support on account<strong>in</strong>g matters. One <strong>of</strong> EFRAG’s key tasks<br />

is to advise the Commission on the question <strong>of</strong> whether<br />

<strong>in</strong>dividual <strong>IFRSs</strong> should be endorsed for use <strong>in</strong> <strong>Europe</strong>.<br />

EFRAG also plays an active part <strong>in</strong> develop<strong>in</strong>g account<strong>in</strong>g<br />

standards at IASB level: EFRAG representatives sit on<br />

IASB work<strong>in</strong>g groups, for <strong>in</strong>stance, and comment on the<br />

IASB’s work<strong>in</strong>g papers and exposure drafts. It is partly<br />

funded by contributions from <strong>in</strong>dustry and, s<strong>in</strong>ce 2009,<br />

around 50% <strong>of</strong> its entire budget has come from the<br />

<strong>Europe</strong>an Commission.<br />

From the outset, various groups and nations <strong>in</strong><br />

<strong>Europe</strong> were critical <strong>of</strong> the endorsement process and<br />

<strong>of</strong> the way EFRAG functioned. In the eyes <strong>of</strong> these<br />

critics, the EU cont<strong>in</strong>ues to have too little weight <strong>in</strong><br />

the <strong>in</strong>ternational standard-sett<strong>in</strong>g process. With the<br />

aim <strong>of</strong> strengthen<strong>in</strong>g <strong>Europe</strong>’s role, the <strong>Europe</strong>an<br />

Commission <strong>in</strong> March 2013 appo<strong>in</strong>ted Philippe<br />

Maystadt, a Belgian politician and former President<br />

<strong>of</strong> the <strong>Europe</strong>an Investment Bank, as a special adviser<br />

to review the entire <strong>in</strong>stitutional <strong>in</strong>frastructure for<br />

adopt<strong>in</strong>g <strong>IFRSs</strong>, <strong>in</strong>clud<strong>in</strong>g the governance structures<br />

<strong>of</strong> EFRAG. <strong>The</strong> f<strong>in</strong>d<strong>in</strong>gs <strong>of</strong> this review were unveiled <strong>in</strong><br />

November 2013 <strong>in</strong> the Maystadt Report. <strong>The</strong> report’s<br />

Parties <strong>in</strong>volved <strong>in</strong> the endorsement process<br />

IASB<br />

EFRAG<br />

<strong>Europe</strong>an Commission<br />

<strong>Europe</strong>an Parliament<br />

ARC<br />

Interested public<br />

<strong>Europe</strong>an Council<br />

Source: <strong>Europe</strong>an Commission.<br />

<strong>The</strong> <strong>future</strong> <strong>of</strong> <strong>IFRSs</strong> <strong>in</strong> <strong>Europe</strong> 13