The G20 processhas arrived ata low po<strong>in</strong>t. Itseems difficultfor <strong>the</strong> UnitedStates <strong>and</strong> <strong>the</strong> EUto reach beyond<strong>the</strong> m<strong>in</strong>imumconsensus.U.S. markets actually contracted (see graphs page5). 9 Ch<strong>in</strong>a alone can be expected to raise its share<strong>in</strong> global f<strong>in</strong>ancial markets by <strong>the</strong> end of <strong>the</strong> currentdecade to 13 percent <strong>in</strong> bank<strong>in</strong>g, 5 percent <strong>in</strong> debtsecurities, <strong>and</strong> 16 percent <strong>in</strong> stocks. 10These long-term dynamics <strong>in</strong> f<strong>in</strong>ancial marketsmake a very strong case for <strong>in</strong>clud<strong>in</strong>g key emerg<strong>in</strong>geconomies <strong>in</strong> f<strong>in</strong>ancial market reform at <strong>the</strong> globallevel. The still-dom<strong>in</strong>ant U.S. <strong>and</strong> EU shares <strong>in</strong>global f<strong>in</strong>ance, however, also illustrate that <strong>the</strong>United States <strong>and</strong> Europe are <strong>in</strong> a unique positionto promote global f<strong>in</strong>ancial reform, a position thatfor <strong>the</strong> time be<strong>in</strong>g rema<strong>in</strong>s unatta<strong>in</strong>able for anyo<strong>the</strong>r economy around <strong>the</strong> negotiat<strong>in</strong>g table.Transatlantic F<strong>in</strong>ancial MarketDiplomacy at a Low Po<strong>in</strong>tBe<strong>in</strong>g <strong>the</strong> most important f<strong>in</strong>ancial marketsworldwide is one th<strong>in</strong>g. Pursu<strong>in</strong>g jo<strong>in</strong>t <strong>in</strong>terests,however, may be a completely different matter. Inpr<strong>in</strong>ciple, <strong>the</strong> United States <strong>and</strong> <strong>the</strong> EU may havediverg<strong>in</strong>g, possibly compet<strong>in</strong>g <strong>in</strong>terests when itcomes to f<strong>in</strong>ancial market policy, <strong>and</strong> <strong>the</strong>y coulduse <strong>the</strong>ir economic <strong>and</strong> political weight as abasis for pursu<strong>in</strong>g <strong>the</strong>se <strong>in</strong>terests <strong>in</strong> a G20 sett<strong>in</strong>gconcurrently.In fact, two years <strong>in</strong>to <strong>the</strong> G20 process, transatlanticcooperation on f<strong>in</strong>ancial market policy appearsto have reached a low po<strong>in</strong>t. On <strong>the</strong> one h<strong>and</strong>,some credit can be given to <strong>the</strong> United States <strong>and</strong><strong>the</strong> EU, as well as to <strong>the</strong> o<strong>the</strong>r nations represented<strong>in</strong> <strong>the</strong> G20. Arriv<strong>in</strong>g at a jo<strong>in</strong>t agenda for policydevelopment <strong>and</strong> on broad policy directions9All figures based on own calculations <strong>and</strong> data from Bank forInternational Settlements, International F<strong>in</strong>ancial Services,Transatlantic Bus<strong>in</strong>ess Dialogue, World Federation ofExchanges.10Ch<strong>in</strong>a’s share <strong>in</strong> <strong>the</strong> global total is expected to rise from 9percent to 13 percent <strong>in</strong> bank<strong>in</strong>g, from 2 percent to 5 percent<strong>in</strong> debt securities, <strong>and</strong> from 6 percent to 16 percent <strong>in</strong> stockmarkets (Kern 2009).especially <strong>in</strong> <strong>the</strong> area of f<strong>in</strong>ancial market reformmarks an important political achievement that canhardly be overestimated.On <strong>the</strong> o<strong>the</strong>r h<strong>and</strong>, however, it has been difficultfor U.S. <strong>and</strong> EU policymakers to reach beyond<strong>the</strong> m<strong>in</strong>imum consensus on agenda items <strong>and</strong>broad policy directions. Importantly, <strong>the</strong>y differsubstantially <strong>in</strong> <strong>the</strong>ir approaches to <strong>the</strong> G20 agenda<strong>and</strong> its implementation at home. While <strong>the</strong> UnitedStates chose a s<strong>in</strong>gle-package strategy that hasalready resulted <strong>in</strong> <strong>the</strong> Dodd-Frank Act, cover<strong>in</strong>gall major areas of f<strong>in</strong>ancial reform. The EU, on <strong>the</strong>o<strong>the</strong>r h<strong>and</strong>, follows a menu-type strategy of morethan 25 <strong>in</strong>dividual measures for f<strong>in</strong>al adoption <strong>in</strong><strong>the</strong> course of 2011. As a consequence, <strong>the</strong> politicalprocesses have rema<strong>in</strong>ed largely out of sync.Apart from procedural questions, Americans <strong>and</strong>Europeans also disagree on a number of substantiveissues. These <strong>in</strong>clude topics such as <strong>the</strong> U.S. VolckerRule, a proposal not directly conta<strong>in</strong>ed <strong>in</strong> <strong>the</strong> G20agenda. While <strong>the</strong> EU is not plann<strong>in</strong>g comparablemeasures, <strong>the</strong>re is widespread concern that itsimplementation may have negative extraterritorialeffects. Similarly, <strong>the</strong>re is, reflect<strong>in</strong>g on earlierexperiences, concern that <strong>the</strong> United States maynot succeed <strong>in</strong> implement<strong>in</strong>g <strong>the</strong> recent versionof <strong>the</strong> Basel Accord on bank capital, despite itsendorsement at <strong>the</strong> November 2010 Seoul Summit.Americans, <strong>in</strong> turn, are ill at ease with <strong>the</strong> EUrules on alternative <strong>in</strong>vestments as adopted <strong>in</strong> <strong>the</strong>Alternative Investment Fund Managers Directive(AIFM) <strong>and</strong> are critical of <strong>the</strong> treatment of thirdcountryfunds under <strong>the</strong> new regime. Fur<strong>the</strong>rtransatlantic deviations can be found <strong>in</strong> <strong>the</strong>approaches to additional bank taxes <strong>and</strong> levies, aswell as to short sell<strong>in</strong>g. 1111For details on <strong>the</strong> differ<strong>in</strong>g policy positions between <strong>the</strong>United States <strong>and</strong> <strong>the</strong> EU, see Atlantic Council (2010).6Transatlantic Academy

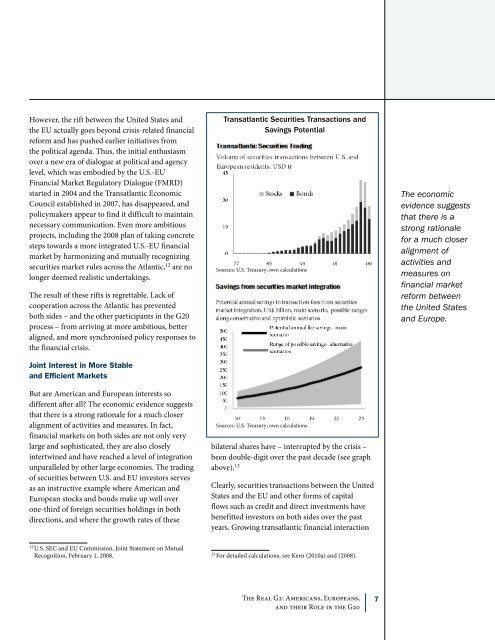

However, <strong>the</strong> rift between <strong>the</strong> United States <strong>and</strong><strong>the</strong> EU actually goes beyond crisis-related f<strong>in</strong>ancialreform <strong>and</strong> has pushed earlier <strong>in</strong>itiatives from<strong>the</strong> political agenda. Thus, <strong>the</strong> <strong>in</strong>itial enthusiasmover a new era of dialogue at political <strong>and</strong> agencylevel, which was embodied by <strong>the</strong> U.S.-EUF<strong>in</strong>ancial Market Regulatory Dialogue (FMRD)started <strong>in</strong> 2004 <strong>and</strong> <strong>the</strong> Transatlantic EconomicCouncil established <strong>in</strong> 2007, has disappeared, <strong>and</strong>policymakers appear to f<strong>in</strong>d it difficult to ma<strong>in</strong>ta<strong>in</strong>necessary communication. Even more ambitiousprojects, <strong>in</strong>clud<strong>in</strong>g <strong>the</strong> 2008 plan of tak<strong>in</strong>g concretesteps towards a more <strong>in</strong>tegrated U.S.-EU f<strong>in</strong>ancialmarket by harmoniz<strong>in</strong>g <strong>and</strong> mutually recogniz<strong>in</strong>gsecurities market rules across <strong>the</strong> Atlantic, 12 are nolonger deemed <strong>real</strong>istic undertak<strong>in</strong>gs.The result of <strong>the</strong>se rifts is regrettable. Lack ofcooperation across <strong>the</strong> Atlantic has preventedboth sides – <strong>and</strong> <strong>the</strong> o<strong>the</strong>r participants <strong>in</strong> <strong>the</strong> G20process – from arriv<strong>in</strong>g at more ambitious, betteraligned, <strong>and</strong> more synchronised policy responses to<strong>the</strong> f<strong>in</strong>ancial crisis.Jo<strong>in</strong>t Interest <strong>in</strong> More Stable<strong>and</strong> Efficient MarketsBut are American <strong>and</strong> European <strong>in</strong>terests sodifferent after all? The economic evidence suggeststhat <strong>the</strong>re is a strong rationale for a much closeralignment of activities <strong>and</strong> measures. In fact,f<strong>in</strong>ancial markets on both sides are not only verylarge <strong>and</strong> sophisticated, <strong>the</strong>y are also closely<strong>in</strong>tertw<strong>in</strong>ed <strong>and</strong> have reached a level of <strong>in</strong>tegrationunparalleled by o<strong>the</strong>r large economies. The trad<strong>in</strong>gof securities between U.S. <strong>and</strong> EU <strong>in</strong>vestors servesas an <strong>in</strong>structive example where American <strong>and</strong>European stocks <strong>and</strong> bonds make up well overone-third of foreign securities hold<strong>in</strong>gs <strong>in</strong> bothdirections, <strong>and</strong> where <strong>the</strong> growth rates of <strong>the</strong>seTransatlantic Securities Transactions <strong>and</strong>Sav<strong>in</strong>gs PotentialSources: U.S. Treasury; own calculationsSources: U.S. Treasury; own calculationsbilateral shares have – <strong>in</strong>terrupted by <strong>the</strong> crisis –been double-digit over <strong>the</strong> past decade (see graphabove). 13Clearly, securities transactions between <strong>the</strong> UnitedStates <strong>and</strong> <strong>the</strong> EU <strong>and</strong> o<strong>the</strong>r forms of capitalflows such as credit <strong>and</strong> direct <strong>in</strong>vestments havebenefitted <strong>in</strong>vestors on both sides over <strong>the</strong> pastyears. Grow<strong>in</strong>g transatlantic f<strong>in</strong>ancial <strong>in</strong>teractionThe economicevidence suggeststhat <strong>the</strong>re is astrong rationalefor a much closeralignment ofactivities <strong>and</strong>measures onf<strong>in</strong>ancial marketreform between<strong>the</strong> United States<strong>and</strong> Europe.12U.S. SEC <strong>and</strong> EU Commission, Jo<strong>in</strong>t Statement on MutualRecognition, February 1, 2008.13For detailed calculations, see Kern (2010a) <strong>and</strong> (2008).The Real G2: Americans, Europeans,<strong>and</strong> <strong>the</strong>ir Role <strong>in</strong> <strong>the</strong> G207