Pricing Currency Options Under Stochastic Volatility

Pricing Currency Options Under Stochastic Volatility

Pricing Currency Options Under Stochastic Volatility

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Pricing</strong> <strong>Currency</strong> <strong>Options</strong> <strong>Under</strong> <strong>Stochastic</strong> <strong>Volatility</strong>Ming-Hsien ChenDepartment of FinanceNational Cheng Chi UniversityYin-Feng Gau *Department of International Business StudiesNational Chi Nan UniversityAugust 2004Keywords: <strong>Stochastic</strong> volatility; <strong>Currency</strong> options; Implied risk premium of volatility.JEL codes: F31, G13.* Corresponding Author. Department of International Business Studies, National Chi Nan University, 1 University Rd., Puli,Nantou 545, Taiwan, E-Mail: yfgau@ncnu.edu.tw, Tel: (886)49-2910960 ext. 4921, Fax: (886)-49-2912595. The authors aregrateful to the Philadelphia Stock Exchange (PHLX) for offering the data of Foreign <strong>Currency</strong> <strong>Options</strong> <strong>Pricing</strong> History (FCOPH).1

AbstractThis paper investigates the relative pricing performance between constant volatility andstochastic volatility pricing models, based on a comprehensive sample of options onfour currencies, including the British pound, Deutsche mark, Japanese yen and Swissfranc, traded frequently in the Philadelphia Stock Exchange (PHLX) from 1994 to 2001.The results show that the model of Heston (1993) outperforms the model of Garmanand Kohlhagen (1983) in terms of sum of squared pricing errors for all currency options.Furthermore, the adjustment speed toward the long-run mean volatility in the currencymarket is faster than that in the stock market. It may be attributed to the largermomentum effect in the stock. We also find that the stock market exhibits largerimplied skewness than the currency market. This may be due to stronger ‘trend effect’in the stock market, especially involved in the bear market.Keywords: <strong>Stochastic</strong> volatility; <strong>Currency</strong> options; Implied risk premium of volatility.JEL Codes: F31, G13.2

1. IntroductionIt has been shown that the Black-Scholes (1973) option pricing model is subject tosystematic biases originated from the violation of the normal distribution assumptionon the underlying returns (e.g., Melino and Turnbull (1990), Day and Lewis (1992),Rubinstein (1994), Bakshi, Cao, and Chen (1997), Nandi (1998), Bates (1996, 2000,2003), and Lin, Strong and Xu (2001)). Empirically, the negative implicit skewnesscauses the out-of-the-money option price bias, whereas the implicit leptokurtosisincreases the prices of deeply in-the-money and out-of-money options and lower pricesof near-the-money options.To enhance the pricing accuracy, the stochastic volatility (SV) option pricingmodels, such as Hull and While (1987), Scott (1987), Wiggins (1987), Melino andTurnbull (1990), and Heston (1993), incorporate the leptokurtosis or excess kurtosis ofthe underlying asset returns by allowing the volatility process to behave randomly. 1Black and Scholes (1973) specified that the source of volatility risk comes fromstochastic returns of the underlying, however, the SV option pricing models allow thepricing risk to emerge from both the stochastic processes of price and the volatility. Tomodel the stochastic process of volatility in the SV option pricing model, one has tospecify the market price of volatility risk, the volatility of variance, and the correlationbetween underlying price (return) and its volatility. Assuming zero correlation of priceand volatility, Hull and White (1987) used the Taylor expansion technique andproposed a power series approximation for the European stock call option; Scott (1987)specified the volatility process as a mean-reverting Ornstein-Uhlenbeck process;Wiggins (1987) included investors’ utility function into the model to incorporate themarket price of volatility risk. The major limitation of Hull and White (1987), Scott(1987), and Wiggins (1987) models is the assumption of zero correlation between the3

underlying return and its volatility, although they do consider the phenomenon ofleptokurtosis of the return process. Fleming (1998) and Guo (1996) argued that theimplied variance extracted from the model of Hull and White (1987) is dominant butstill a biased estimator in terms of out-of-sample forecasting performance in thestock-index and foreign currency options markets.Stein and Stein (1991) offered the stock price distribution evaluated by an inverseFourier series transformation based on the no correlation between the underlying returnand its volatility, and obtained a closed-form formula for the European options.Specifically, Hull and White (1987), Scott (1987), Wiggins (1987) and Stein and Stein(1991) contributed the consideration of the kurtosis by modeling the volatility to astochastic process, but left the skewness of the underlying returns to be not incorporatedin the models.Heston (1993) argued that the correlation between the underlying asset return andits volatility affected both the skewness and the leptokurtosis of the distribution ofunderlying returns. This correlation is important in explaining for the skewness thataffects the pricing of in-the-money options. With the zero correlation, the stochasticvolatility is only related to the kurtosis that influences the pricing of near-the-moneyand far-from-the-money options, thus it can induce the pricing errors in options. Bates(1996) offered an empirical study based on the closed form solution of Heston (1993),with a diffusion-jump process. By estimating the parameters in the volatility process onthe Deutsche mark options, Bates (1996) found that the stochastic volatility couldexplain the implicit leptokurtosis only by considering the jump risk. Guo (1998)empirically studied the parameters on the risk-neutral variance process and the marketprice of variance risk implied in the PHLX currency options, based on the model ofHeston (1993). Guo found that the market price of variance risk was nonzero, time4

varying, and of sufficient magnitude to imply that the compensation for variance riskwas a sufficient component of the risk premium in the currency market. On the stockoptions, Bakshi, Cao and Chen (1997) evaluated the relative in-sample fitness,out-of-sample pricing and hedging performances for S&P 500 stocks call optionsamong various options pricing models, including SV, SV with jump, and stochasticinterest option pricing models. However, their results based on stock index optionssuggest that adding jumps or stochastic interest rates to the SV model does notsignificantly improve the hedging performance, although the SV model with jumpsperforms best in out-of-sample pricing performance. Nandi (1998) also pointed out theimportance of the correlation between the underlying return and its volatility. Based onthe options on the S&P 500 index, Nandi (1998) observed a significant improvement onthe pricing performance when considering a nonzero correlation in the empiricalinvestigation. Bates (2000) obtained similar results based on the S&P 500 futuresoptions and demonstrated a negative correlation between index returns and volatilityinnovation. Lin, Strong and Xu (2001) empirically studied how the Heston (1993)model reduced the pricing errors of FTSE 100 index options.Although Bakshi, Cao, and Chen (1997) have evaluated the empiricalperformances of constant volatility and SV option pricing models, their results based onindex options may not hold for currency options. In this paper, we use a 8-year sampleof historical prices of currency options on the Philadelphia Stock Exchange (PHLX),including options on the British pound, Deutsche mark, Japanese yen and Swiss franc,from 1994 to 2001, to compare the pricing performances of constant volatility and SVoptions pricing models. We also extract the parameters implicit in the model of Heston(1993) by allowing an nonzero correlation between the volatility and the underlyingasset return. With different estimation periods, such as weekly, monthly or 6-months5

interval, we compare the different interval-estimated dynamic processes of asset priceand volatility based on these parameters. In this paper, we investigate the exchangerates process implicited in currency options and compare the relative pricingperformance between the model of Garman and Kohlhagen (1983), a modified versionof the Black-Scholes model for the currency option, and the model of Heston (1993)which specifies both the stochastic processes of the underlying asset return andvolatility.There are three major findings in this study. First, we find that the model ofHeston (1993) outperforms the model of Garman and Kohlhagen (1983), in terms of thesum of squared pricing errors for all currency options from 1994 to 2001. Thepercentage difference of the sum of squared pricing errors between the Garman andKohlhagen and the Heston models are from nearly 30% to 70%, suggesting that thespecification of stochastic volatility does improve the pricing accuracy on currencyoptions. Furthermore, we estimate the implicit parameters of the risk-neutral stochasticvariance process in the model of Heston (1993) by using a nonlinear-least-square-errorapproach. We find that, in the currency market, the adjustment speed toward thelong-run mean volatility implicit in currency options is faster than that in the stockmarket. It may be attributed to the fact that there is a larger momentum effect in thestock market than that in the currency market, resulting in the slow mean-revertingspeed in the stock market. Finally, we find that the stock market exhibits a morenegative skewness than that in the currency market. The phenomenon could beexplained based on the fact that the stock market exhibits a stronger ‘trend effect,’especially involved in the bear market. Another explanation could be supported by theexchange-rate target zones hypothesis that states that there exist no extreme values oncurrency returns.6

The remainder of this paper is organized as follows. Section 2 introduces modelsof currency option pricing, including Garman and Kohlhagen (1983) and Heston (1993).Section 3 describes the data of the PHLX currency option prices. Section 4 reports theestimation results of implied parameters and the pricing performance of differentoptions pricing models. Section 5 concludes the paper.2. Models of <strong>Currency</strong> Option PricesBlack and Scholes (1973) assumed that the volatility of the returns is constant andused the concept of hedging portfolios of options and their underlying stocks to derivethe non-dividends European option theoretical valuation formula. Garman andKohlhagen (1983) is one of the versions of the Black-Scholes options pricing model onthe currency option. Similar to the Black-Scholes model, based on the arbitrage-freecondition, Garman and Kohlhagen (1983) compared the advantages of holding aforeign exchange option with those of holding its underlying currency. <strong>Under</strong> theseconditions, spot and options markets are frictionless and the domestic ( r D ), and foreign( r F ) interest rates are constant, Garman and Kohlhagen (1983) applied the interest-rateparity to derive the European currency option valuation formula:−rFτCS ( , τ ) = Se Nd ( ) − Ke Nd ( ), (1)−rDτ1 2whered12ln( S/ K) + [( rD− rF) + 0.5 σ ] τ= ; d2 = d1− σ τ . Symbols S, K, σ , andσ ττ ≡T− t denote the spot rate, exercise price, the constant volatility of the underlyingasset return, and the time to maturity, respectively. By the put-call parity, the Europeanstyle put option can be obtained:−rTDPST ( , ) = Ke N( −d) −Se N( − d). (2)−rTF2 1Many studies, such as Bollerslev, Chou, and Kroner (1992), Heieh (1989), and7

Poon and Granger (2003), have argued that the exchange rate volatility follows astochastic process. Specifically, tails of the distribution computed with intraday ordaily market prices are fatter than those of the lognormal distribution, exhibitingleptokurtosis (Gesser and Poncet, 1997). Thus, the estimated implied volatility fromthe constant volatility assumption from the Black-Shcoles or Garman–Kohlhage modelwill be a biased estimate. Various stochastic volatility option pricing models, such asHull and White (1987), Scott (1987), Wiggins (1987), Melino and Turnbull (1991),Heston (1993), and Bates (1996), were developed to solve the unrealistic assumption,the constant return volatility. In this paper, we adopt Heston’s (1993) SV model toinvestigate its relative performance against the model of Garman-Kohlhagen (1983),and explore the exchange rate process implicit in the options based on the model ofHeston (1993).Releasing the assumption that correlation between volatility and the spot return iszero, Heston (1993) obtained a closed-form solution for the European option on anasset, including stock, currency and bond, with mean-reverting square-root stochasticvolatility. Heston (1993) asserted that the correlation between the underlying assetreturns and its volatility affected the skewness and leptokurtosis of the distribution ofthe underlying asset returns. The volatility is specified to follow an Ornstein-Uhlenbeckmean reverting process given below:dSt () = µ Stdt () + VtStdz () () () t, (3)dV () t = κθ ( − V ()) t dt + σ V () t dz () t , (4)where dzS( t ) and dzV( t ) are Wiener processes with instantaneous correlation ρ , i.e.,( (), ())corr dz t dz t = ρdt. The major difference between the model of Hull and WhiteSV(1987) and that of Heston (1993) is the specification of the correlation. TheVSV8

instantaneous variance Vt () follows a square-root process proposed by Cox, Ingersolland Ross (1985). The dynamic process, dV () t , follows a mean-reverting process withlong term mean, θ , mean reversion speed, κ , and volatility of volatility, σV.Following the risk-neutral pricing probabilities derived by Cox, Ingersoll, andRoss (1985), Equation (4) can be rewritten as:* *() ( θ ()) σV()V()dV t = k − V t dt + V t dz t , (5)** kθwhere κ = κ + λ , θ = , and λ is the risk premium parameter compensated fork + λthe volatility risk from σ V. 2 The instantaneous risk-neutral variance process Vt ( )**drifts toward a long-run mean of θ , with the mean-reversion speed dominated by κ .In general, if the risk-neutral probability density function of a future security’s price isf ( ST), the exercise price is K, the time to maturity is τ = T − t, and the price of aEuropean call option can be written as,∞−rτC = e ∫ ( Sτ −K) f( Sτ)dSτ. (6)Heston (1993) derived the density function of S satisfying Equations (3) and (5) byinverting the Fourier transform for the convolution of the lognormal density of S Tconditional on the average variance and the density of average variance. The derivationrelies on properties of the conditional distribution and involves numerical integration ofthe characteristic function of the probability process. The European call option oncurrency is as follows:K−rfτ−rdτ1 2C = Se P − Ke P . (7)C, S, and K have the same meaning in the Balck-Scholes model. In order to get aclosed-form solution, Heston used the Fourier transformation and derived theprobability density function P j : 39

∞ −iϕln( K)1 1 ⎡e fj( x, v, t; ϕ)⎤Pj( x, v, t;ln[ K]) = + Redϕ2 π∫ ⎢ ⎥iϕ0 ⎢⎣⎥, (8)⎦where j=1, 2, Re means the real part of the square bracket, f ( xvtϕ , , ; ) represents thecharacteristic functions of the conditional probability Pj.( ϕ )1 1 ∞ ⎡exp −i ln( K)⋅ f ⎤Pj= + ⎢ ⎥2 π ⎣ iϕ⎦j = 1, 2jj∫ Redϕ0, (9)where fj, j = 1,2 is the characteristic function of the parameters set,Φ= . 4 Given no-arbitrage condition and the price of a call option, C , we* *{ k , θ , σv, ρ}can use the put-call parity to obtain the European put option price as,−rfτ−rdτ= − + . (10)P C Se KeSince the American style currency options traded in the PHLX are used in this study,we employ the quadratic approximation method of Barone-Adesi and Whaley (1987) toadjust the early exercise premium to derive a more accurate empirical study. 53. Data Description and Sample PropertiesWe use the “Foreign <strong>Currency</strong> <strong>Options</strong> <strong>Pricing</strong> History (FCOPH)” database of thePHLX. 6 The FCOPH data of the PHLX contain options on the Australian dollar, Britishpound, Canadian dollar, Deutsche mark, Euro, Japanese yen, Swiss franc and otherrelated customized option contracts. The trade-by-trade option prices cover the periodfrom January 1994 to December 2001. The major advantage of using PHLX databaseis that the daily closing option prices and the simultaneous spot exchange rate quotesare recorded on the same transaction report.The trading hours is from 2:30 a.m. to2:30 p.m., Eastern Time, Monday to Friday. We use the mid-month option, whichexpires in March, June, September, December and the two near-term months and10

month-end option, which expires at three nearest months call and put options. Theprecise expiration date is the Friday preceding the third Wednesday of the month formid-month options and the last Friday of the month for month-end options.Daily closing prices of options and the simultaneous spot exchange rate quotes onBritish pound, Deutsche mark, Japanese yen and Swiss franc against US dollar areselected as our samples. Two reasons for choosing these four currencies are that theyare highly volatile and are most frequently traded in the PHLX in terms of the tradingvolumes. Since the European Union started using EURO in 1999, the currency optionsof British pound and Deutsche mark were traded less over the period from 1999 to 2001than that from 1994 to 1998. Thus, the selected sample periods are from January, 1994to December, 1998 for the British pound and Deutsche mark and those are from January,1994 to December, 2001 for Japanese yen and Swiss franc. Since the database ofPHLX contains the null values of simultaneous spot rates on Japanese yen over theperiod from October, 1994 to March, 1996, we fill the blank with daily spot rate fromthe DataStream.In this study we use the American-style call and put options and discard theuninformative options records from samples in the following categories. First, since forthe implied volatility of options, the maturity day is less than 5 calendar days that iserratic, we use options with the period from 5 to 90 calendar days to expiration.Second, options violate the European-style boundary conditions, for example, thecondition isC−r F τ −rDτ< Se − Ke for currency call options. And finally, the daily optionswith the strike/spot price ratio (moneyness, denoted as S/K for call options, K/S for putoptions) are from 0.8 to 1.2.We use the daily closing quotes of London Euro-Dollars rates collected fromDataStream, including the U.S. dollar against the British pound, Deutsche mark,11

Japanese yen and Swiss franc as likely riskless interest rates to derive the impliedvolatility from two alternative option models. To match the maturity of currencyoptions, the 30-, 60- and 90-day interest rates are used to be the rates whose maturityare very close to the option expiration. Table 1 summarizes the sample sizes of fourcurrency options. There are a total of 394,940 records in the PHLX database includingthe British pound, Deutsche mark, Japanese yen, Swiss franc and other currencies (suchas, Australian dollar, Canadian dollar and EURO) over the period from 1994 to 2001.From Table 1, we can find that most options traded in the PHLX are American-style,especially on the British pound and Deutsche mark.To investigate the existence of volatility smile of implied volatility, we first dividethe option data into several categories in terms of either moneyness or time to maturity.We classify the money of a call (put) option to three categories, at-the-money (ATM)option, in which its S/K (K/S) is from 0.99 to 1.01, out-of-the-money option (OTM), inwhich its S/K (K/S) is below 0.99, and in-the-money option (ITM), in which its S/K (K/S)is above 1.01. A finer partition resulted in six moneyness categories. According to theterm of expiration, options are classified into (i) short term maturity (5~30 days); (ii)medium term maturity (30~60 days); and (iii) long term maturity (60~90 days). Table2.1 to 2.4 offers the sample properties of PHLX currency options in our studies. Thereported numbers are the average quoted prices, the standard deviations shown in theparentheses, and the total observed options listed in braces, for eachmoneyness-maturity category. The sample period extends from January, 1994 toDecember, 1998 including a total of 30410 options for British pound and 80779 optionsfor Deutsche mark, respectively; and from January, 1994 to December, 2001 includinga total of 63016 for Japanese yen, and a total of 50990 for Swiss franc, respectively.Note that for British pound, OTM, ITM and ATM options take up 45.3 percent, 10.812

percentage and 43.9 percent of the total sample, and the average call price ranges from0.1995 cents for short-term, deep OTM options to 8.0601 cents for long-term, and deepITM calls. Sample properties across moneyness and time to maturity for Deutsch mark,Japanese yen and Swiss franc are similar to that of British pound as shown in Tables 2.2- 2.4.4. Implied Parameters Estimation and In-Sample <strong>Pricing</strong>PerformanceOur analysis intend to present pricing biases of the Black-Scholes model causedby the stochastic volatility of underlying returns and to investigate this volatilityprocess implicit in currency options. First of all, we back up the implied volatility fromGarman and Kohlhagen (1983) model on four currency options. If the volatility patternshowed the effect of smile, the constant-volatility assumption could not be applied forcurrency options and the pricing biases did exist. Furthermore, we could apply a morecomplicit model, the Heston model (1993), to investigate the relative pricingperformance between Garman and Kohlhagen (1983) model, and Heston (1993)stochastic volatility model. Finally, we investigate the volatility process implicit incurrency options.4.1 Implied volatility of Garman and Kohlhagen (1983) modelThere are many currency options traded on the same underlying currency withdifferent maturities and strike prices. To estimate the implied volatility of one currencyon certain period, we follow the approach of Whaley (1982) by using anequally-weighted nonlinear least squares method to estimate the daily impliedvolatility.13

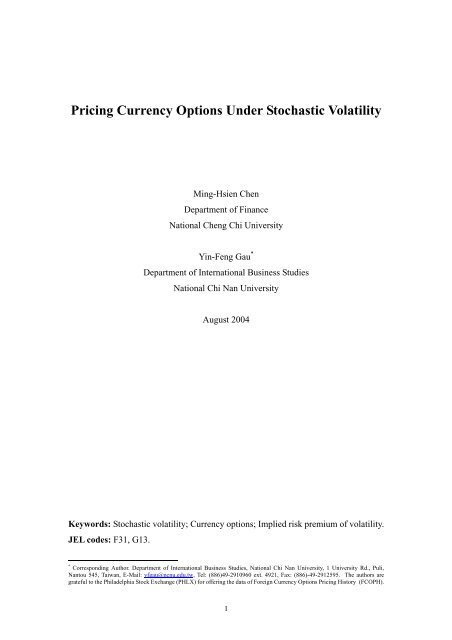

GKit ,NGKGKit ,=it ,−it ,i=1, tmin SSE( σ ) ∑ [ C C ] , (11)σ2where Cit,is the currency i option’s market price, N is the trading call/put options insample period t in each moneyness-maturity category, andKohlhagen’s theory call/put price derived from equation (1).GKCit,is Garman andTable 3 reports the average Garman and Kohlhagen implied volatility estimated byminimizing the sum of squared errors across six moneyness and three maturitycategories. It is obvious that the Garman and Kohlhagen’s implied volatility exhibits asmile pattern as shown in Figure 1, especially in the deep OTM options. The samepattern can also be found across the maturity, but in some cases the pattern exhibits aslight smirk effect, as the term to expiration increases. For example, the impliedvolatility of deep-OTM and short maturity category on Japanese yen options, is from0.141, 0.128 to 0.105. A non-flat implied volatility curve across moneyness is anindication of model misspecification. These findings of moneyness-related andmaturity-related biases resulted from the constant volatility assumption are consistentwith the prior empirical studies (e.g., on stock options, Bakshi, Cao and Chen (1997);on currency options, Bates (1996)). Therefore any improvement offered by analternative model must be able to show the ability to price OTM and ITM options moreaccurately. As the smile effect is indicative of negative-skewed implicit returndistributions with leptokurtosis, a better model, such as Heston (1993), must take thephenomenon of the negative-skewed and leptokurtic distributions of underlying returnsinto account.4.2 Implied risk-neutral parameters from Heston (1993) modelWe use a nonlinear-least-square-error approach to estimate the implicit parameters14

of the risk-neutralized stochastic variance process in Equation (4). Similar to theprocess of backing up the implied volatility from Garman and Kohlhagen in Equation(11), we follow Whaley (1982) to use an equally weighted nonlinear least square toestimate the implied parameters. The principle is that the estimated parameters arechosen to minimize the sum of square pricing errors between the quoted options pricesand theoretical option prices from the Heston (1993) model. Specifically, for eachsample period in the sample, we collect all the call and put option i and trading onperiod t, then solve the following optimization function which minimizes the sum ofsquared errors between model prices and observed premiums,vt,T NH2∑∑ Cit ,Cit ,vt, (12)t 1 i 1min [ − ( , Φ)]Φ = =andΦ= is the parameters set in Heston’s return and volatility processes.* *{ κ , θ , σv, ρ}T is the number of trading days in an estimating period, N is the number of options onHperiod t; Cit ,and C,( v , Φ ) are the traded options prices and Heston’s option price,ittrespectively. The computational intensity makes the direct estimation of the entireparameter vector* *Φ= { κ , θ , σv, ρ}andtv . Therefore, the parameters in Φ and vtare estimated simultaneously until the parameter estimates converge within a desiredtolerance level. 7Summary statistics for volatilities and risk-neutral parameter estimates from theHeston model implicit in options prices are shown in Tables 4 and 5, respectively.Implied volatility smile graphs show the cross-sectional pricing ability of an optionpricing model. The information on implied volatility taken from an option model isdirectly related to the option trader’s expectations of the underlying volatility over theremaining life of the option. In other words, implied volatilities over substantiallydifferent horizons indicate different market perceptions of the underlying volatility.15

Therefore, alternative volatility smiles should be compared for a given trading horizon.Figure 2 presents the implied volatility curves associated with the Garman andKohlhagen as well as Heston models, backed out from the four PHLX currency optionsacross moneyness. It shows that the implied volatilities of Heston model display a flatcurve across moneyness than that of Garman and Kohlhagen model. Figure 2 illustratesa rough idea that for currency options, the stochastic volatility model provides asuperior pricing fitness as the constant volatility model does, though the sharps ofHeston’s implied volatilities across moneyness still exhibit a slight smirk-pattern,especially for short-maturity out-of-money options.The risk-neutral mean-reverting volatility process is controlled by threeparameters: the long-term mean*θ to which volatility reverts, the speed of reversion*κ , and the variation coefficient σv. For example, the parameters of British pound in1994 are estimated to the values of { κ * ,*θ , σv} = {10.469, 0.2243, 0.1491}, andvolatility takes about 24 days to revert halfway towards a long-term mean of 22.43%.Based on the whole sample period, average reverting speed of the volatility on fourcurrencies are 10.376%, 8.1663%, 13.330%, and 7.8516% for British pound, Deutschemark, Japanese yen, and Swiss franc, respectively. The range of average half-life ofshocks is from 19 to 33 days. Compared with Guo’s (1998) findings on Deutsche marktraded in the PHLX from 1987 to 1992, our estimates of the parameter on the speed of*reversion κ (an average value 8.1663) is similar. However, we find that the speed ofreversion on the volatility shock in the currency market is faster than that in stockmarkets. Bakshi, Cao and Chen (1997) found that the value of speed of reversion forS&P 500 index options during the period from 1988 to 1991 is equal to 1.15, similar tothe finding of 1.49 for the period from 1988 to 1993 in Bates (2000), while Nandi (1998)found it on stock futures options as equal to 3.29. This phenomenon could be16

contributed to the more resourceful information and more frequent trading session inthe currency market than those in the stock markets. Thus, the adjusting speed towardthe long-run mean volatility in the currency market is quicker than that in the stockmarket. Another story is that the momentum effect could be large in the stock marketresulting in a slow mean-reverting speed.The average variation coefficients, σ vwhich catch leptokurtosis effect of thereturn process, are 0.1494, 0.1090, 0.1008, and 0.2012 for British pound, Deutschemark, Japanese yen, and Swiss franc, respectively, during each sample period. Whilethe correlation coefficients, which responde to the negative skewness of the returndistribution, between the two Brownian motions in return and volatility process areestimated to be -0.0090, -0.0143, -0.0097, and -0.0071 (average) on the four currenciesin Table 5. These empirical findings show that the stochastic volatility model doesprovide a flexible structure to consider both skewness and leptokurtosis effects on thedistribution on the underlying returns, which is oversimplifiedly assumed to follow thelog-normal distribution in the Black-Scholes type option models. Previous studies, e.g.Bakshi, Cao and Chen (1997), Nandi (1998) and Bates (2000), show that in the stockmarket, coefficients range from -0.54 to -0.79 which suffer more series skewnesseffects than that in the currency market. A potential explanation for this differencebetween the stock and currency markets may be attributed to the former that owns thestronger ‘trend effect’ especially involved in the bear market. It also could be supportedby the exchange-rate target zones hypothesis, causing that there does not exist extremevalues on currency returns, in foreign exchange markets.4.3 In-sample pricing fitnessFor each year in the sample, the structural parameters of the Garman and17

Kohlhagen model as well as the Heston model are estimated by minimizing the sum ofsquared errors between the market price and the theoretical price. The daily averagesum of squared errors, as shown in Table 6, are calculated by collecting each optionpricing squared errors and then are divided by the 365 calendar days for each model.These reported statistics are quite informative about the internal working of the models.As such, several observations are in order. First, from Table 6, it can be easily foundthat the Heston model performs better than the model of Garman and Kohlhagen interms of sum of squared pricing errors for all currency options. The percentagedifference of the sum of squared pricing errors between Garman and Kohlhagen modeland Heston model are 38.64%, 28.80%, 41.05%, and 68.11% for the British pound,Deutsche mark, Japanese yen, and Swiss franc, respectively.The improved pricing accuracy could be attributed to two major modifications, theskewness and the high kurtosis in the Heston model. Comparing Tables 5 and 6, we canfind that the largest improved pricing performance occurred in 1996 for the Britishpound, 1996 for the Deutsche mark, and 2000 for Japanese yen, respectively. FromTable 5, these years also show the largest negative skewness effects among the threecurrencies. (The values of ρ are -0.0099, -0.0149, and -0.107.) Among the fourcurrency options, Heston SV model performs better than the Garman-Kohlhagen model,especially in Swiss franc. This result shows another source, the estimated σv, whichcatches the leptokurtosis effect, that could improve the pricing performance. The valueof the largest improved pricing performance in Swiss franc is almost twice as that ofJapanese yen (84% larger than that of Deutsche mark), and is near 35% larger than thatof British pound. Similar to the studies of Guo (1998) in currency options, and ofBakshi, Cao and Chen (1997) in the stock index options, our results support thatincluding the stochastic volatility process in the option pricing model can catch the18

actual return distribution better than the log-normal distribution specification inBlack-Scholes type models, in terms of in sample pricing fitness.5. ConclusionUsing a comprehensive sample of the PHLX currency options, including theBritish pound, Deutsche mark, Japanese yen, and Swiss franc, we find that consideringthe skewness and kurtosis of the underlying asset returns significantly improve theaccuracy of option pricing, especially for the out-of-money options.There are three principal contributions in this paper. First, we employ currencyoptions on the British pound, Deutsche mark, Japanese yen, and Swiss franc to examinethe pricing performances of the constant volatility option pricing model of Garman andKohlhagen (1983) and the stochastic volatility option pricing model of Heston (1993).Second, we back out the volatility implied in the foreign-currency option market via themodels of Garman and Kohlhagen as well as Heston (1993) and identify whether theimplied volatility is characterized by a smile. The results show that the volatility smileeffects are significant especially in the deep OTM options across moneyness and timeto maturity in the PHLX currency option market. Third, utilizing thenonlinear-least-square method we estimate the parameters of Garman and Kohlhagen(1983) model and Heston (1993) model. Similar to the related studies in stock markets,we find that Heston model does provide a superior pricing fitness than the constantvolatility model, though the sharps of Heston’s implied volatilities across moneynessstill exhibit a slight smirk-pattern, especially for short-maturity out-of-money options.Moreover, we estimate the parameters of the underlying process implicit in Hestonmodel, based on four foreign-currency options. We find that the speed of reversion onthe volatility shock in the currency market is faster than that in stock markets proposed19

y Bakshi, Cao and Chen (1997) and Bates (2000) for S&P 500 index options, andNandi (1998) for stock futures options. We think that the divergence could be caused bythe degree of efficiency differing from stock market to the currency market. Wepresume the different reverting speed between the stock and currency markets could beattributed to the more resourceful information and more frequent trading sessions in thecurrency market than those in the stock market. Another reason may be due to themomentum effect. It could be larger in the stock market than in the currency marketresulting in the slow mean-reverting speed in the later market. Regarding the negativecorrelation parameter, we find that prior studies on stock markets suffer more seriesskewness effects than our results in the currency market. A potential reason to explainthis difference between stock and currency market may be attributed to the former thatowns the stronger ‘trend effect’ especially involved in the bear market. It could also besupported by the exchange-rate target zones hypothesis, which states that there does notexist extreme values on currency returns, in foreign exchange markets. Finding outfactors that result in the different behaviors between the stock market and currencymarket is an interesting direction of future research. A further exanimation byout-of-sample pricing performance and hedging efficiency will be considered in ourfuture investigation.20

Footnotes1. Although the SV option pricing models with jumps could price options better, Bakshiet al. (1997) found that adding jumps or stochastic interest rates does not improve theperformance of the SV model. Therefore, the focus of this paper is on the improvementof considering stochastic volatility in pricing foreign-currency options.2. Since there is no traded security that can be used to hedge the risk of exchange ratevolatility, the volatility of variance, the valuation of the option is no longer preferencefree, and the market prices of volatility risks need to be determined. Similar to theargument of Breeden (1979), the risk premium can be set as proportional to thevolatility V, that is, λ( SVt , , ) = λV.3. It assumes that the moment-generating function M(t) of a random variable X is finiteon an interval –a < t < a. If M(t) is finite on such an interval, thenkEX is finite for all k;in particular, if EX does not exist or is infinite, then M(t) does not exist on such aninterval. To handle such a distribution, the characteristic function is often used. Thecharacteristic function of a random variable X is defined byiXtc( t)= E(e ) = E[cos(Xt)+ iE(sin(Xt)]. In the applied mathematics, the characteristicfunction is often called the Fourier transform of the density function. See Arnold(1990), Mathematical Statistics, Prentice-Hall Englewood Cliffs, New Jersey, pp.117-122, for details.4. See Heston (1993) for more details on the derivation of the characteristic functions.5. Barone-Adesi and Whaley (1987) used the quadratic approximation method to priceAmerican call and put options on an underlying asset with cost-of-carry rate b. Whenb≥ r (r is the domestic risky-free interest rate, and the cost-of-carry rate b is equal tothe difference between domestic risky-free rate and foreign risky-free rate, i.e.,b= r − r ), the American call value is equal to the European call value and can bedf21

found by using the generalized Black-Scholes formula.6. PHLX provide two kinds of currency options traded in exchange, the standardizedand customized options. In the present paper, we just use the standardized contracts.7. We use the Nelder-Mead simplex algorithm, which is the most widely used directsearch method for nonlinear unconstrained optimization problems to solve the problemin Equation (12).22

ReferencesArnold (1990), Mathematical Statistics, Prentice-Hall Englewood Cliffs, New Jersey.Bakshi, G., Cao, C. and Chen, Z. (1997), “Empirical Performance of Alternative Option<strong>Pricing</strong> Models,” Journal of Finance, 52, 2003-2049.Barone-Adesi, G., and Whaley, R. (1987), “Efficient Analytic Approximation ofAmerican Option Values,” Journal of Finance, 42, 301-320.Bates, D. (1996), “Jumps and <strong>Stochastic</strong> <strong>Volatility</strong>: Exchange Rate Processes Implicitin Deutsche Market <strong>Options</strong>,” Reviews of Financial Studies, 9, 69-107.Bates, D. (2000), "Post-'87 Crash Fears in the S&P 500 Futures Option Market,"Journal of Econometrics, 94, 181-238.Bates, D. (2003), "Empirical Option <strong>Pricing</strong>: A Retrospection," Journal ofEconometrics, 116, 387-404.Black, F. and Scholes, M., (1973), “The <strong>Pricing</strong> of <strong>Options</strong> and Corporate Liabilities,”Journal of Political Economy, 81, 637-659.Bollerslev, T., R. Y. Chou, and K. F. Kroner (1992), “ARCH Modeling in Finance: AReview of the Theory and Empirical Evidence,” Journal of Econometrics, 52,5-59.Cox, J. C., Ingersoll, J. E, and Ross, S. A. (1985), “An Intertemporal GeneralEquilibrium Model of Asset Prices,” Econometrica, 53, 363-384.Day, T. E., and Lewis, C. M. (1992), “Stock Market <strong>Volatility</strong> and the InformationContent of Stock Index <strong>Options</strong>,” Journal of Econometrics, 52, 267-287.Fleming, J. (1998), “The Quality of Market <strong>Volatility</strong> Forecasts Implied by S&P 100Index Option Prices,” Journal of Empirical Finance, 5, 317-345.Garman, M. B., and Kohlhagen, S. W., (1983), “Foreign <strong>Currency</strong> Option Values,”Journal of International Money and Finance, 2, 231-237.23

Gesser, V. and P. Poncet (1997), “<strong>Volatility</strong> Patterns: Theory and Some Evidence fromthe Dollar-Mark Option Market,” Journal of Derivatives, 5, 46-65.Guo, D. (1996), “The Predictive Power of Implied <strong>Stochastic</strong> Variance From <strong>Currency</strong><strong>Options</strong>,” Journal of Futures Markets, 16, 915-942.Guo, D. (1998), “The Risk Premium of <strong>Volatility</strong> Implicit in <strong>Currency</strong> <strong>Options</strong>,”Journal of Business & Economic Statistics, 16, 498-507.Heston, S. (1993), “A Closed Form Solution for <strong>Options</strong> With <strong>Stochastic</strong> <strong>Volatility</strong>,”Review of Financial Studies, 6, 327-343.Hsieh, D. A. (1989), “Modeling Heteroscedasticity in Daily Foreign Exchange Rates,”Journal of Business and Economic Statistics, 7, 307-317.Hull, J., and White, A. (1987), “The <strong>Pricing</strong> of <strong>Options</strong> on Assets With <strong>Stochastic</strong><strong>Volatility</strong>,” Journal of Finance, 42,281-300.Lin, Y. N., Strong, N., and Xu, X. (2001), “<strong>Pricing</strong> FTSE 100 Index <strong>Options</strong> <strong>Under</strong><strong>Stochastic</strong> <strong>Volatility</strong>,” Journal of Futures Markets, 21, 197-211.Melino, A., and Turnbull, S. (1990), “<strong>Pricing</strong> Foreign <strong>Currency</strong> <strong>Options</strong> With<strong>Stochastic</strong> <strong>Volatility</strong>,” Journal of Econometrics, 45, 7-39.Nandi, S. (1998), “How Important Is the Correlation Between Returns and <strong>Volatility</strong> inA <strong>Stochastic</strong> <strong>Volatility</strong> Model? Empirical Evidence from <strong>Pricing</strong> and Hedging inthe S&P 500 Index <strong>Options</strong> Market,” Journal of Banking and Finance, 22,589-610.Rubinstein, M. (1994), “Implied Binomial Trees”, Journal of Finance 49, 771-818.Scott, L. O. (1987), “Option <strong>Pricing</strong> When the Variance Changes Randomly: Theory,Estimation, and an Application,” Journal of Financial and Quantitative Analysis,22, 419-439.Stein, E. M., and Stein, J. C. (1991), “Stock Price Distributions with <strong>Stochastic</strong>24

<strong>Volatility</strong>: An Analytic Approach,” Reviews of Financial Studies, 4, 727-752.Whaley, R. E. (1982), “Valuation of American Call <strong>Options</strong> on Dividend Paying Stocks:Empirical Tests,” Journal of Financial Economics, 10, 29-58Wiggins, J. (1987), “Option Values <strong>Under</strong> <strong>Stochastic</strong> <strong>Volatility</strong>: Theory and EmpiricalEstimates,” Journal of Financial Economics, 19, 351-372.25

Table 1. Samples of <strong>Currency</strong> <strong>Options</strong>BritishPoundDeutscheMarkJapaneseYenSwissFrancEuropean Styles 8,580 18,401 12,929 46,733American Styles 32,810 81,724 26,714 51,416Total 41,390 100,125 39,643 98,149Note: The sample periods begin from January, 1994 through December, 1998 for the British pound andthe Deutsche mark, and from January, 1994 through December, 2001 for the Japanese yen and the Swissfranc. The American-style options include mid-month and month-end options for the four currencies.26

Table 2.1 Sample Properties of PHLX <strong>Currency</strong> <strong>Options</strong> (British pound)MoneynessCalendar Days to Maturity

Table 2.2 Sample Properties of PHLX <strong>Currency</strong> <strong>Options</strong> (Deutsche mark)Moneyness(S/K)Calendar Days to Maturity

Table 2.3 Sample Properties of PHLX <strong>Currency</strong> <strong>Options</strong> (Japanese yen)MoneynessCalendar Days to Maturity

Table 2.4 Sample Properties of PHLX <strong>Currency</strong> <strong>Options</strong> (Swiss franc)MoneynessDays to Maturity

Table 3. Implied <strong>Volatility</strong> from the Garman and Kohlhagen (1983) ModelTime to MaturityBritish pound Deutsche mark Japanese yen Swiss francMoneyness

Table 4. Implied <strong>Volatility</strong> from the Heston (1993) ModelTime to MaturityBritish pound Deutsche mark Japanese yen Swiss francMoneyness

Table 5. Return and <strong>Volatility</strong> Processes Parameters Implicit in Heston Model*Year κ*θBritish pound Deutsche mark Japanese yen Swiss francσ ρHalfvLife*κ*θσ ρHalfvLife*κ*θσ ρHalfvLife*κ*θσ ρHalfvLife1994 10.469 0.0503 0.1491 -0.0090 24.167 8.8247 0.0110 0.1109 -0.0145 28.669 13.335 0.0092 0.1041 -0.0102 18.972 8.1639 0.0204 0.2041 -0.0071 30.9901995 9.817 0.0202 0.1483 -0.0088 25.771 8.0808 0.0111 0.1131 -0.0146 31.309 13.304 0.0099 0.1008 -0.0100 19.016 8.3475 0.0103 0.1999 -0.0069 30.3081996 10.528 0.0201 0.1497 -0.0099 24.031 8.3108 0.0112 0.1119 -0.0149 30.442 12.7230.0091 0.1012 -0.0071 19.885 8.3808 0.0202 0.2090 -0.0073 30.1881997 10.835 0.0216 0.1482 -0.0085 23.349 8.2401 0.0092 0.1031 -0.0132 30.704 12.445 0.0103 0.1027 -0.0096 20.329 9.3496 0.0184 0.2046 -0.0060 27.0601998 10.232 0.0203 0.1518 -0.0091 24.727 7.3751 0.0104 0.1062 -0.0146 34.304 13.858 0.0101 0.1037 -0.0102 18.256 8.4215 0.0191 0.2017 -0.0068 30.0421999 13.3300.0096 0.1007 -0.0097 18.979 4.8961 0.0202 0.1992 -0.0091 51.6732000 12.760 0.0101 0.1003 -0.0107 19.827 7.4487 0.0195 0.1936 -0.0068 33.9652001 14.886 0.0088 0.0927 -0.0104 16.996 7.8047 0.0200 0.1974 -0.0071 32.416Average 10.376 0.0265 0.1494-0.009024.409 8.1663 0.0106 0.1090 -0.0143 31.086 13.3300.0096 0.1008 -0.0097 19.032 7.8516 0.0185 0.2012 -0.007133.33033

Table 6. In-Sample <strong>Pricing</strong> FitnessSampleperiodSum of Square <strong>Pricing</strong> ErrorsBritish pound Deutsche mark Japanese yen Swiss francG&K Heston Difference % G&K Heston Difference % G&K Heston Difference % G&K Heston Difference %1994 17.626 11.698 5.928 33.63 18.592 16.923 1.669 8.97 38.715 28.355 10.360 26.76 15.592 13.401 2.191 14.051995 18.086 13.239 4.847 26.99 19.056 14.776 4.280 22.46 25.608 19.865 5.743 22.43 15.624 14.953 0.671 4.291996 32.309 14.013 18.296 56.63 34.067 21.841 12.226 35.89 21.896 10.768 11.128 50.82 17.639 14.076 3.563 20.191997 26.377 18.847 7.530 28.55 35.521 24.559 10.962 30.86 15.639 5.035 10.604 67.80 29.593 13.838 15.755 53.241998 19.078 11.837 7.241 37.95 33.278 21.944 11.334 34.06 15.572 8.036 7.536 48.39 16.403 12.784 3.619 22.061999 16.083 11.184 4.899 30.46 19.007 11.641 7.366 38.752000 30.732 15.066 15.666 50.97 17.449 15.636 1.813 10.392001 15.702 7.774 7.928 50.49 13.999 13.625 0.374 2.67Total 113.48 69.63 113.48 69.63 140.51 100.04 43.85 38.64 179.94 106.08 73.86 41.05 125.30 39.96 85.34 68.11Average 22.695 13.926 28.103 20.009 22.493 13.260 15.663 4.994 Note: For each year in the sample, the structural parameters of models of Garman and Kohlhagen (G&K) as well as Heston (1987) are estimated byminimizing the sum of squared errors between the market price and theoretical price. The daily average sum of squared errors is calculated bycollecting each option’s squared pricing errors and then is divided by the 365 calendar days for each model.34

Figure 1. Implied <strong>Volatility</strong> of Garman-Kohlhagen (G&K) Model AcrossMoneyness and MaturityBritish poundDeutsche markJapanese yenSwiss franc35

Figure 2. Implied <strong>Volatility</strong> Pattern: Garman-Kohlhagen (G&K) Model versusHeston Model Across MaturityShort-term Maturity< 30 daysMiddle-term Maturity30 ~ 60 daysBritishpoundDeutschemark36

Figure 2. (continued) Implied <strong>Volatility</strong> Pattern: Garman-Kohlhagen (G&K)Model versus Heston Model Across MaturityShort-term Maturity< 30 daysMiddle-term Maturity30 ~ 60 daysJapaneseyenSwissfranc37