<strong>2006</strong> <strong>Timberlane</strong> <strong>Regional</strong> <strong>School</strong> <strong>District</strong> <strong>Annual</strong> <strong>Report</strong>AUDITOR’S REPORTPLODZIK & SANDERSONProfessional Association/Accountants & Auditors193 North Main Street · Concord · New Hampshire · 03301-5063 ·603-225-6996 · FAX 224-1380To the Members of the <strong>School</strong> Board - <strong>Timberlane</strong> <strong>Regional</strong> <strong>School</strong> <strong>District</strong> - Plaistow, New HampshireWe have audited the accompanying financial statements of the governmental activities, each major fund and theaggregate remaining fund information of the <strong>Timberlane</strong> <strong>Regional</strong> <strong>School</strong> <strong>District</strong> as of and for the year endedJune 30, <strong>2006</strong>, which collectively comprise the <strong>Timberlane</strong> <strong>Regional</strong> <strong>School</strong> <strong>District</strong>’s basic financial statements aslisted in the table of contents. These financial statements are the responsibility of the <strong>School</strong> <strong>District</strong>’smanagement. Our responsibility is to express opinions on these financial statements based on our audit.We conducted our audit in accordance with auditing standards generally accepted in the United States ofAmerica, and the standards applicable to financial audits contained in Government Auditing Standards issued bythe Comptroller General of the United States. Those standards require that we plan and perform the audit toobtain reasonable assurance about whether the financial statements are free of material misstatement. An auditincludes examining, on test basis, evidence supporting the amounts and disclosures in the financial statements.An audit also includes assessing the accounting principles used and significant estimates made by management,as well as evaluating the overall financial statement presentation. We believe that our audit provides areasonable basis for our opinions.The government-wide statement of the net assets does not include any of the <strong>School</strong> <strong>District</strong>’s capital assets northe accumulated depreciation on those assets; and the government-wide statement of activities does not includedepreciation expense related to those assets. These amounts have not been determined. Therefore, in ouropinion, the financial statements referred to above do not present fairly the respective financial position of thegovernmental activities of the <strong>Timberlane</strong> <strong>Regional</strong> <strong>School</strong> <strong>District</strong> at June 30, <strong>2006</strong>, and the respective changesin financial position thereof for the year then ended in conformity with accounting principles generally acceptedin the United States of America.Also, in our opinion, the financial statements referred to above present fairly, in all material respects, therespective financial position of each major fund and the aggregate remaining fund information of the <strong>Timberlane</strong><strong>Regional</strong> <strong>School</strong> <strong>District</strong>, as of June 30, <strong>2006</strong>, and the respective changes in financial position thereof for theyear then ended in conformity with accounting principles generally accepted in the United States of America.In accordance with Government Auditing Standards, we have also issued our report dated August 19, 2005 onour consideration of the <strong>Timberlane</strong> <strong>Regional</strong> <strong>School</strong> <strong>District</strong>’s internal control over financial reporting and ourtests of its compliance with certain provisions of laws, regulations, contracts and grant agreements and othermatters. The purpose of that report is to describe the scope of our testing of internal control over financialreporting and compliance and the results of that testing, and not to provide an opinion on the internal controlover financial reporting or on compliance. That report is an integral part of an audit performed in accordancewith Government Auditing Standards and should be considered in assessing the results of our audit.The budgetary comparison information is not a required part of the basic financial statements, but issupplementary information required by the Governmental Accounting Standards Board. We have applied certainlimited procedures, which consisted principally of inquiries of management regarding the methods ofmeasurement and presentation of the required supplementary information. However, we did not audit theinformation and express no opinion on it.The <strong>Timberlane</strong> <strong>Regional</strong> <strong>School</strong> <strong>District</strong> has not presented a management’s discussion and analysis thataccounting principles generally accepted in the United States of America have determined is necessary tosupplement, although not required to be part of, the basic financial statements.Our audit was made for the purpose of forming opinions on the financial statements that collectively comprisethe <strong>Timberlane</strong> <strong>Regional</strong> <strong>School</strong> <strong>District</strong>’s basic financial statements. The combining and individual fundschedules are presented for purposes of additional analysis and are not a required part of the basic financialstatements. The accompanying schedule of expenditures of federal awards is presented for purposes ofadditional analysis as required by the U.S. Office of Management and Budget Circular A-133, Audits of States,Local Governments, and Non-Profit Organizations, and is not a required part of the basic financial statements.The combining and individual fund schedules and the schedule of expenditures of federal awards have beensubjected to the auditing procedures applied in the audit of the basic financial statements and, in our opinion,are fairly stated in all material respects in relation to the basic financial statements taken as a whole.August 17, <strong>2006</strong>36

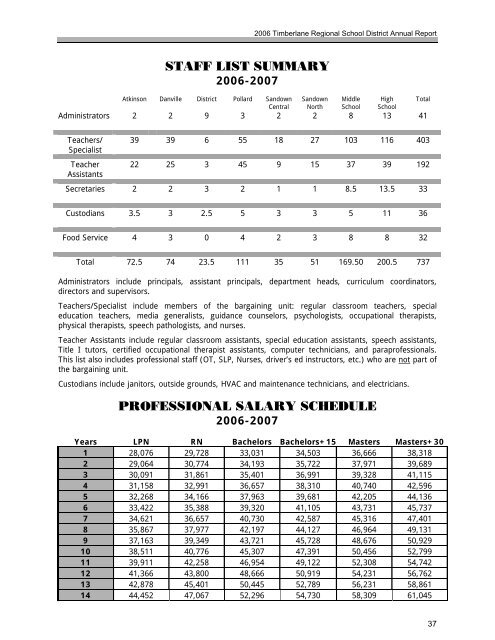

<strong>2006</strong> <strong>Timberlane</strong> <strong>Regional</strong> <strong>School</strong> <strong>District</strong> <strong>Annual</strong> <strong>Report</strong>STAFF LIST SUMMARY<strong>2006</strong>-2007Atkinson Danville <strong>District</strong> Pollard SandownCentralSandownNorthMiddle<strong>School</strong>High<strong>School</strong>Administrators 2 2 9 3 2 2 8 13 41TotalTeachers/SpecialistTeacherAssistants39 39 6 55 18 27 103 116 40322 25 3 45 9 15 37 39 192Secretaries 2 2 3 2 1 1 8.5 13.5 33Custodians 3.5 3 2.5 5 3 3 5 11 36Food Service 4 3 0 4 2 3 8 8 32Total 72.5 74 23.5 111 35 51 169.50 200.5 737Administrators include principals, assistant principals, department heads, curriculum coordinators,directors and supervisors.Teachers/Specialist include members of the bargaining unit: regular classroom teachers, specialeducation teachers, media generalists, guidance counselors, psychologists, occupational therapists,physical therapists, speech pathologists, and nurses.Teacher Assistants include regular classroom assistants, special education assistants, speech assistants,Title I tutors, certified occupational therapist assistants, computer technicians, and paraprofessionals.This list also includes professional staff (OT, SLP, Nurses, driver’s ed instructors, etc.) who are not part ofthe bargaining unit.Custodians include janitors, outside grounds, HVAC and maintenance technicians, and electricians.PROFESSIONAL SALARY SCHEDULE<strong>2006</strong>-2007Years LPN RN Bachelors Bachelors+15 Masters Masters+301 28,076 29,728 33,031 34,503 36,666 38,3182 29,064 30,774 34,193 35,722 37,971 39,6893 30,091 31,861 35,401 36,991 39,328 41,1154 31,158 32,991 36,657 38,310 40,740 42,5965 32,268 34,166 37,963 39,681 42,205 44,1366 33,422 35,388 39,320 41,105 43,731 45,7377 34,621 36,657 40,730 42,587 45,316 47,4018 35,867 37,977 42,197 44,127 46,964 49,1319 37,163 39,349 43,721 45,728 48,676 50,92910 38,511 40,776 45,307 47,391 50,456 52,79911 39,911 42,258 46,954 49,122 52,308 54,74212 41,366 43,800 48,666 50,919 54,231 56,76213 42,878 45,401 50,445 52,789 56,231 58,86114 44,452 47,067 52,296 54,730 58,309 61,04537