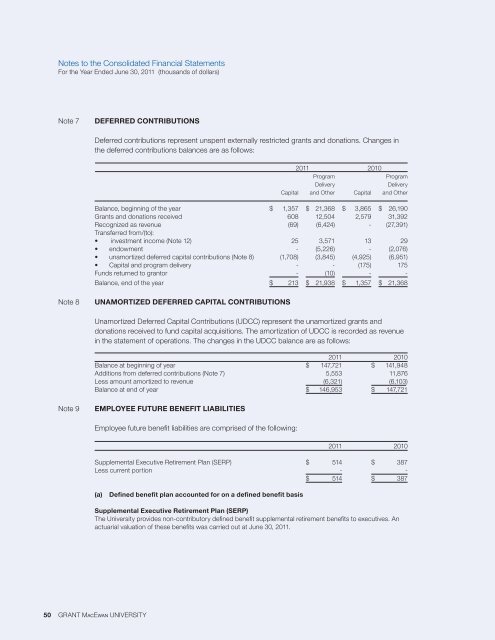

Notes to the Consolidated Financial StatementsFor the Year Ended June 30, 20<strong>11</strong> (thousands of dollars)Note 7Deferred ContributionsDeferred contributions represent unspent externally restricted grants and donations. Changes inthe deferred contributions balances are as follows:20<strong>11</strong> <strong>2010</strong>ProgramProgramDeliveryDeliveryCapital and Other Capital and OtherBalance, beginning of the year $ 1,357 $ 21,368 $ 3,865 $ 26,190Grants and donations received 608 12,504 2,579 31,392Recognized as revenue (69) (6,424) - (27,391)transferred from/(to):• investment income (Note 12) 25 3,571 13 29• endowment - (5,226) - (2,076)• unamortized deferred capital contributions (Note 8) (1,708) (3,845) (4,925) (6,951)• Capital and program delivery - - (175) 175Funds returned to grantor - (10) - -Balance, end of the year $ 213 $ 21,938 $ 1,357 $ 21,368Note 8Unamortized Deferred Capital ContributionsUnamortized Deferred Capital Contributions (UDCC) represent the unamortized grants anddonations received to fund capital acquisitions. The amortization of UDCC is recorded as revenuein the statement of operations. The changes in the UDCC balance are as follows:20<strong>11</strong> <strong>2010</strong>Balance at beginning of year $ 147,721 $ 141,948Additions from deferred contributions (Note 7) 5,553 <strong>11</strong>,876Less amount amortized to revenue (6,321) (6,103)Balance at end of year $ 146,953 $ 147,721Note 9Employee Future Benefit LiabilitiesEmployee future benefit liabilities are comprised of the following:20<strong>11</strong> <strong>2010</strong>Supplemental Executive Retirement Plan (SERP) $ 514 $ 387Less current portion - -$ 514 $ 387(a)Defined benefit plan accounted for on a defined benefit basissupplemental Executive Retirement Plan (SERP)the University provides non-contributory defined benefit supplemental retirement benefits to executives. Anactuarial valuation of these benefits was carried out at June 30, 20<strong>11</strong>.50 grant Macewan university

Notes to the Consolidated Financial StatementsFor the Year Ended June 30, 20<strong>11</strong> (thousands of dollars)The expense and financial position of the supplemental executive retirement plan is as follows:20<strong>11</strong> <strong>2010</strong>expensesCurrent service cost $ 93 $ 91Interest cost 29 21Amortization of net actuarial (gains) losses 4 -Total Expense $ 126 $ <strong>11</strong>2financial PositionAccrued benefit obligation:Balance, beginning of year $ 425 $ 278Current service cost 93 92Interest cost 29 21Actuarial (gain) loss (4) 34Balance, end of year 543 425Unamortized net actuarial loss (29) (38)Accrued benefit liability $ 514 $ 387the University plans to use its working capital to finance these future obligations.the significant actuarial assumptions used to measure the accrued benefit obligations are as follows:20<strong>11</strong> <strong>2010</strong>Discount rate 5.60 % 5.60 %Rate of compensation increase 4.00 % 4.00 %Inflation rate 2.50 % 2.50 %Estimated average remaining service life 8 9(b) Defined benefit plan accounted for on a defined contribution basislocal Authorities Pension Plan (LAPP)the LAPP is a multi-employer contributory defined benefit pension plan for participating staff members andis accounted for on a defined contribution basis. At December 31, <strong>2010</strong>, the LAPP reported an actuarialdeficiency of $4,635,250 (2009 - $3,998,614). An actuarial valuation of the LAPP was carried out onDecember 31, <strong>2010</strong>. The pension expense recorded in these financial statements is $8,8<strong>11</strong> (<strong>2010</strong>: $7,715).Note 10Long-term LIABILITIESMaturity Interest Amount outstandingCollateral Date Rate % 20<strong>11</strong> <strong>2010</strong>Debentures payable to Alberta Capital Finance Authority:Parkade (1) April 2025 6.25 $ 4,692 $ 4,898Student residence (1) June 2030 5.85 35,747 36,754West parkade (1) Sept. 2030 4.39 5,175 5,340Robbins Health Learning Centre parkade (1) Sept. 2032 4.89 1,659 1,70247,273 48,694obligations under capital leases 291 38947,564 49,083Less current portion 1,581 1,518$ 45,983 $ 47,565Collateral: (1) cash flows from facilitythe principal portion of long-term debt repayments required over the next five years is as follows:2012 - $1,581; 2013 - $1,673; 2014 - $1,770; 2015 - $1,815; 2016 - $1,886 and thereafter - $38,839.Interest expense on long term liabilities is $2,748 (<strong>2010</strong> - $2,826).consolidated financial statements <strong>2010</strong>/20<strong>11</strong> 51