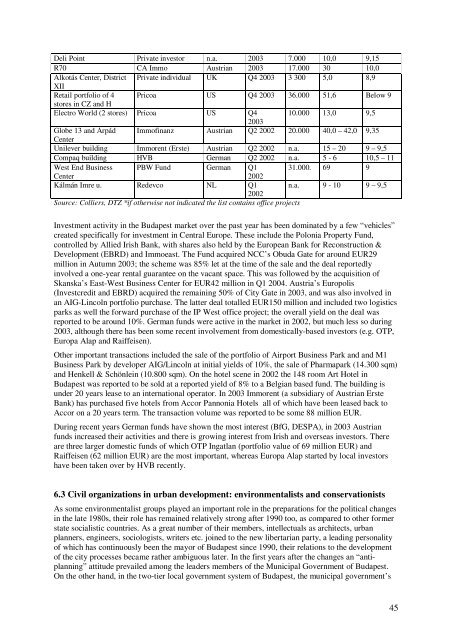

<strong>the</strong> company was able to tide over hard times. Even more important was that through keep<strong>in</strong>g"everyth<strong>in</strong>g <strong>in</strong> one hand" outflow <strong>of</strong> pr<strong>of</strong>its could be evaded, and used for <strong>in</strong>vestments <strong>in</strong>clud<strong>in</strong>g <strong>the</strong>improvement <strong>of</strong> <strong>the</strong> company's technical <strong>in</strong>frastructure. (No <strong>in</strong>terest payments have been done to <strong>the</strong>shareholders, <strong>in</strong>clud<strong>in</strong>g also <strong>the</strong> blew-collar workers <strong>of</strong> <strong>the</strong> company.) In this l<strong>in</strong>e also sell<strong>in</strong>g priceswere kept on an affordable level under <strong>the</strong> circumstances <strong>of</strong> a narrow<strong>in</strong>g hous<strong>in</strong>g market.Quadrat's success was also backed by its fair bus<strong>in</strong>ess relations to <strong>the</strong> newly elected district,government. It was also an important factor that architectural and landscape design cont<strong>in</strong>ued to bedone by <strong>the</strong> same architects and landscape architects who, work<strong>in</strong>g already <strong>in</strong> private bus<strong>in</strong>esses,have ga<strong>in</strong>ed experiences <strong>in</strong> <strong>the</strong> difficult bus<strong>in</strong>ess <strong>of</strong> design<strong>in</strong>g <strong>in</strong> a built up environment. Also <strong>the</strong>sehelped Quadrat to fill <strong>in</strong> <strong>the</strong> "development gap" <strong>in</strong> <strong>the</strong> early 1990s, when <strong>the</strong> old socialist structurescollapsed.Source: Lecture <strong>of</strong> <strong>the</strong> writer at <strong>the</strong> Central European University, <strong>Budapest</strong>, based on <strong>in</strong>terviews with Ms Varjas, manager <strong>of</strong><strong>the</strong> company6.2 <strong>Large</strong> <strong>in</strong>vestors <strong>in</strong> <strong>the</strong> <strong>Budapest</strong> real estate marketThere are no published data on how pr<strong>of</strong>itability has changed dur<strong>in</strong>g recent years <strong>in</strong> <strong>the</strong> real estatedevelopment sector. However <strong>the</strong> grow<strong>in</strong>g number <strong>of</strong> firms and <strong>the</strong> <strong>in</strong>creas<strong>in</strong>g volume <strong>of</strong> constructionshow <strong>in</strong>vestor confidence <strong>in</strong> <strong>the</strong> sector. The times are over when <strong>in</strong>itial <strong>in</strong>vestments could be recoupedwith<strong>in</strong> 5 – 7 years, still pr<strong>of</strong>itability is attractive for developers and <strong>in</strong>vestors com<strong>in</strong>g from Austria,Germany, Switzerland, <strong>the</strong> Benelux, Brita<strong>in</strong>, <strong>the</strong> U.S. and Israel. The annual construction volumes <strong>in</strong><strong>the</strong> sector discussed averaged around 100.000 sqm0 per annum. The construction <strong>in</strong>dustry has seensusta<strong>in</strong>able growth dur<strong>in</strong>g past years and <strong>the</strong> short term trend is positive.In <strong>the</strong> years follow<strong>in</strong>g transition <strong>the</strong> <strong>in</strong>vestment market was immature and prime yields reportedlystood around 14-16%. S<strong>in</strong>ce <strong>the</strong> mid-1990s, prime yields have dropped significantly, and currentestimates put <strong>the</strong>m at around 8.5%-9%. These estimates should be treated with caution: <strong>the</strong>re havebeen only a limited number <strong>of</strong> transactions and, as with rents, <strong>the</strong>re is little transparency. The<strong>in</strong>vestment market so far has limited itself to <strong>Budapest</strong>. Decreas<strong>in</strong>g yields <strong>in</strong> <strong>the</strong> Hungarian capitalcontrasts with <strong>the</strong> movement <strong>in</strong> rents over <strong>the</strong> past decade. It partly reflects grow<strong>in</strong>g stability andanticipation <strong>of</strong> an improved rental performance over com<strong>in</strong>g years, due to expectations <strong>of</strong> economicgrowth follow<strong>in</strong>g EU accession. However, market fundamentals suggest that real rental growth isunlikely <strong>in</strong> <strong>the</strong> short-term, and so it can be contributed more to <strong>the</strong> weight <strong>of</strong> money chas<strong>in</strong>g a veryscarce stock <strong>of</strong> good quality properties let on standard leases to blue chip covenants (Table 8) .Table 8Major transactions <strong>in</strong> <strong>Budapest</strong> between 2002 and 2004Address* Investor Nationality Date Size(sq Price(€m) Yield(%)m)Science Park, District XI Sachsenfonds German To be 32.800 67,5 n.a.GmbH (LandesbankSachsen)annuncedby Q42004IP West, District XI Europolis Invest Austrian Q4 2003 24 000 28,0 9,8(forward purchase)City Gate (50% <strong>in</strong>terest) Europolis Invest Austrian Q3 2003 22 000 40,0APV Headquarters (sale OTP Real Estate Hungarian Q3 2003 16 000 15,0& leaseback)FundEast-West Bus<strong>in</strong>ess Polonia Property Irish Q1 2004 15 825 42,5 9,5CenterFund LPObuda Gate, District II Polonia Property Irish Q4 2003 14 500 29,0 9,1FundHerm<strong>in</strong>a Towers Private <strong>in</strong>vestor n.a. Q4 2003 11 250 22,0 10,0Eurocenter Óbuda(shopp<strong>in</strong>g centre)ManhattanPropertiesAustrian. Q4 2003 24.000 36 n.a.44

Deli Po<strong>in</strong>t Private <strong>in</strong>vestor n.a. 2003 7.000 10,0 9,15R70 CA Immo Austrian 2003 17.000 30 10,0Alkotás Center, District Private <strong>in</strong>dividual UK Q4 2003 3 300 5,0 8,9XIIRetail portfolio <strong>of</strong> 4 Pricoa US Q4 2003 36.000 51,6 Below 9stores <strong>in</strong> CZ and HElectro World (2 stores) Pricoa US Q4 10.000 13,0 9,52003Globe 13 and Árpád Imm<strong>of</strong><strong>in</strong>anz Austrian Q2 2002 20.000 40,0 – 42,0 9,35CenterUnilever build<strong>in</strong>g Immorent (Erste) Austrian Q2 2002 n.a. 15 – 20 9 – 9,5Compaq build<strong>in</strong>g HVB German Q2 2002 n.a. 5 - 6 10,5 – 11West End Bus<strong>in</strong>ess PBW Fund German Q1 31.000. 69 9Center2002Kálmán Imre u. Redevco NL Q1 n.a. 9 - 10 9 – 9,52002Source: Colliers, DTZ *if o<strong>the</strong>rwise not <strong>in</strong>dicated <strong>the</strong> list conta<strong>in</strong>s <strong>of</strong>fice projectsInvestment activity <strong>in</strong> <strong>the</strong> <strong>Budapest</strong> market over <strong>the</strong> past year has been dom<strong>in</strong>ated by a few “vehicles”created specifically for <strong>in</strong>vestment <strong>in</strong> Central Europe. These <strong>in</strong>clude <strong>the</strong> Polonia Property Fund,controlled by Allied Irish Bank, with shares also held by <strong>the</strong> European Bank for Reconstruction &Development (EBRD) and Immoeast. The Fund acquired NCC’s Obuda Gate for around EUR29million <strong>in</strong> Autumn 2003; <strong>the</strong> scheme was 85% let at <strong>the</strong> time <strong>of</strong> <strong>the</strong> sale and <strong>the</strong> deal reportedly<strong>in</strong>volved a one-year rental guarantee on <strong>the</strong> vacant <strong>space</strong>. This was followed by <strong>the</strong> acquisition <strong>of</strong>Skanska’s East-West Bus<strong>in</strong>ess Center for EUR42 million <strong>in</strong> Q1 2004. Austria’s Europolis(Investcredit and EBRD) acquired <strong>the</strong> rema<strong>in</strong><strong>in</strong>g 50% <strong>of</strong> City Gate <strong>in</strong> 2003, and was also <strong>in</strong>volved <strong>in</strong>an AIG-L<strong>in</strong>coln portfolio purchase. The latter deal totalled EUR150 million and <strong>in</strong>cluded two logisticsparks as well <strong>the</strong> forward purchase <strong>of</strong> <strong>the</strong> IP West <strong>of</strong>fice project; <strong>the</strong> overall yield on <strong>the</strong> deal wasreported to be around 10%. German funds were active <strong>in</strong> <strong>the</strong> market <strong>in</strong> 2002, but much less so dur<strong>in</strong>g2003, although <strong>the</strong>re has been some recent <strong>in</strong>volvement from domestically-based <strong>in</strong>vestors (e.g. OTP,Europa Alap and Raiffeisen).O<strong>the</strong>r important transactions <strong>in</strong>cluded <strong>the</strong> sale <strong>of</strong> <strong>the</strong> portfolio <strong>of</strong> Airport Bus<strong>in</strong>ess Park and and M1Bus<strong>in</strong>ess Park by developer AIG/L<strong>in</strong>coln at <strong>in</strong>itial yields <strong>of</strong> 10%, <strong>the</strong> sale <strong>of</strong> Pharmapark (14.300 sqm)and Henkell & Schönle<strong>in</strong> (10.800 sqm). On <strong>the</strong> hotel scene <strong>in</strong> 2002 <strong>the</strong> 148 room Art Hotel <strong>in</strong><strong>Budapest</strong> was reported to be sold at a reported yield <strong>of</strong> 8% to a Belgian based fund. The build<strong>in</strong>g isunder 20 years lease to an <strong>in</strong>ternational operator. In 2003 Immorent (a subsidiary <strong>of</strong> Austrian ErsteBank) has purchased five hotels from Accor Pannonia Hotels all <strong>of</strong> which have been leased back toAccor on a 20 years term. The transaction volume was reported to be some 88 million EUR.Dur<strong>in</strong>g recent years German funds have shown <strong>the</strong> most <strong>in</strong>terest (BfG, DESPA), <strong>in</strong> 2003 Austrianfunds <strong>in</strong>creased <strong>the</strong>ir activities and <strong>the</strong>re is grow<strong>in</strong>g <strong>in</strong>terest from Irish and overseas <strong>in</strong>vestors. Thereare three larger domestic funds <strong>of</strong> which OTP Ingatlan (portfolio value <strong>of</strong> 69 million EUR) andRaiffeisen (62 million EUR) are <strong>the</strong> most important, whereas Europa Alap started by local <strong>in</strong>vestorshave been taken over by HVB recently.6.3 Civil organizations <strong>in</strong> <strong>urban</strong> development: environmentalists and conservationistsAs some environmentalist groups played an important role <strong>in</strong> <strong>the</strong> preparations for <strong>the</strong> political changes<strong>in</strong> <strong>the</strong> late 1980s, <strong>the</strong>ir role has rema<strong>in</strong>ed relatively strong after 1990 too, as compared to o<strong>the</strong>r formerstate socialistic countries. As a great number <strong>of</strong> <strong>the</strong>ir members, <strong>in</strong>tellectuals as architects, <strong>urban</strong>planners, eng<strong>in</strong>eers, sociologists, writers etc. jo<strong>in</strong>ed to <strong>the</strong> new libertarian party, a lead<strong>in</strong>g personality<strong>of</strong> which has cont<strong>in</strong>uously been <strong>the</strong> mayor <strong>of</strong> <strong>Budapest</strong> s<strong>in</strong>ce 1990, <strong>the</strong>ir relations to <strong>the</strong> development<strong>of</strong> <strong>the</strong> city <strong>processes</strong> became ra<strong>the</strong>r ambiguous later. In <strong>the</strong> first years after <strong>the</strong> changes an “antiplann<strong>in</strong>g”attitude prevailed among <strong>the</strong> leaders members <strong>of</strong> <strong>the</strong> Municipal Government <strong>of</strong> <strong>Budapest</strong>.On <strong>the</strong> o<strong>the</strong>r hand, <strong>in</strong> <strong>the</strong> two-tier local government system <strong>of</strong> <strong>Budapest</strong>, <strong>the</strong> municipal government’s45

- Page 1 and 2: Large-scale restructuring processes

- Page 3 and 4: 7. Inner-Erzsébetváros, restructu

- Page 5 and 6: 1. An overall gentrification proces

- Page 7 and 8: Józsefváros’s (8 th district) l

- Page 9 and 10: no, or only very short “time-span

- Page 11 and 12: A special population group in Budap

- Page 13 and 14: 2. Other specific factors influenci

- Page 15 and 16: Only in few cases this expectation

- Page 17 and 18: (1.017,4 million non-repayable subs

- Page 19 and 20: Table 3Location of „A” and „B

- Page 21 and 22: investors has proved to be rather s

- Page 23 and 24: they were sold to Hungarian and for

- Page 25 and 26: offers a 5 thousand sq metre “bon

- Page 27 and 28: ambitious programs of relocation of

- Page 29 and 30: district, North-East Csepel: 21 st

- Page 31 and 32: 4.6 Brown-field areas with limited

- Page 33 and 34: see”. It holds its more then 10 h

- Page 35 and 36: Map 4Restructuring processes in Bud

- Page 37: severe in Ferencváros where the Di

- Page 40 and 41: emain exemptions as nowhere else in

- Page 42 and 43: XVII, along Pesti road was the firs

- Page 46 and 47: principal task remained the develop

- Page 48 and 49: Two plans of Madách (Erzsébet) Av

- Page 50 and 51: the share of Jewish people grew fas

- Page 52 and 53: study (Coopers & Lybrand). Accordin

- Page 54 and 55: this principle caused serious confu

- Page 56 and 57: external, that is private, sources.

- Page 58 and 59: in 2005 and 2006. Instead of puttin

- Page 60 and 61: per cent by blocks). Social status

- Page 62 and 63: 7.9 Management of renewal by the Di

- Page 64 and 65: The effort to concentrate subsidies

- Page 66 and 67: • management of the publicly owne

- Page 68 and 69: The system of pedestrian streets in

- Page 70 and 71: Figure 11/BPartnership relations in

- Page 72 and 73: uilding industries was only 17,7 pe

- Page 74 and 75: ather promising. (As part of the la

- Page 76: Musterd, S, and Weesep, J. (1991) E