Exceptions from Subsection 55(2) - CCH Canadian

Exceptions from Subsection 55(2) - CCH Canadian

Exceptions from Subsection 55(2) - CCH Canadian

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

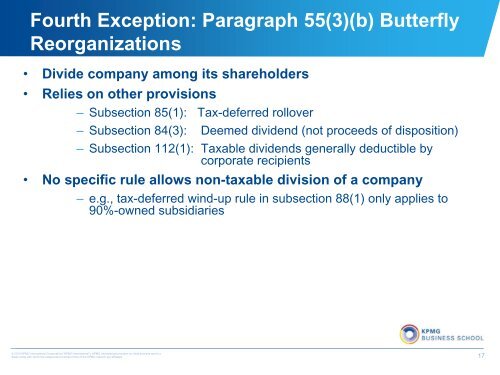

Fourth Exception: Paragraph <strong>55</strong>(3)(b) ButterflyReorganizations• Divide company among its shareholders• Relies on other provisions– <strong>Subsection</strong> 85(1): Tax-deferred rollover– <strong>Subsection</strong> 84(3): Deemed dividend (not proceeds of disposition)– <strong>Subsection</strong> 112(1): Taxable dividends generally deductible bycorporate recipients• No specific rule allows non-taxable division of a company– e.g., tax-deferred wind-up rule in subsection 88(1) only applies to90%-owned subsidiaries© 2010 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is aSwiss entity with which the independent member firms of the KPMG network are affiliated 17