40 | | DEUTSCHE BAHN GroupBusiness unitsAnticipated development [ € million ] Revenues EBIT adjusted2010 2011 2010 2011DB <strong>Bahn</strong> Long-Distance 3,729 e 117 qDB <strong>Bahn</strong> Regional 1) 8,603 q 789 qDB Arriva 1) 1,236 q 57 qDB Schenker Rail 4,584 q 12 qDB Schenker Logistics 14,310 q 304 qDB Services 1,274 q 129 wDB Netze Track 4,580 e 601 qDB Netze Stations 1,044 q 217 eDB Netze Energy 2,501 q 82 eq above previous year’s figure, e on previous year’s level, w below previous year’s figure1)2010 figures were adjusted to reflect the new business unit structure.Based on the level of business noted thus far in the 2011 financialyear for the DB <strong>Bahn</strong> Long-Distance business unit, we havechanged our forecast for the business unit’s anticipated developmentof revenues and currently anticipate that they willremain at the previous year’s level.Based on the level of business noted thus far in the 2011financial year for the DB Services business unit, we currentlyexpect that the business unit will record a slight increase inrevenues, while we expect revenues to remain unchanged in theDB Netze Track business unit.We confirm the revenue forecasts stated on page 136 ofthe 2010 Annual Report for the following business units: DB <strong>Bahn</strong>Regional, DB Arriva, DB Schenker Rail, DB Schenker Logistics,DB Netze Stations and DB Netze Energy.Based on the level of business noted thus far in the 2011financial year for the DB Netze Stations business unit, we havechanged our forecast for the business unit’s adjusted EBIT andcurrently anticipate that this figure will remain at the previousyear’s level.We confirm the adjusted EBIT forecasts stated on page136 of the 2010 Annual Report for the following businessunits: DB <strong>Bahn</strong> Long-Distance, DB <strong>Bahn</strong> Regional, DB Arriva,DB Schenker Rail, DB Schenker Logistics and DB Netze Track.Anticipated financial situationDB Group’s anticipated financial position is described on page137 of the 2010 Annual Report. We do not expect changes in themain focus of our capital expenditures or the financing of ournet capital expenditures.We anticipate that we will also tap the capital and moneymarkets in the second half of 2011 to partially refinance maturingbonds. We have unchanged and appropriate financing scope toaccomplish this based on our debt issuance program, our commercialpaper program and existing, hitherto untapped, creditfacilities. Thus, the short-term and medium-term liquidity supplyfor DB Group is assured.We will continue our M& A activities in a selective andfocused way in the second half of 2011. We do not expect theseactivities to have any significant effects on our financial situationfor the 2011 financial year.FORWARD-LOOKING STATEMENTSThis Management Report contains statements and forecasts pertaining to the futuredevelopment of DB Group, its business units and individual companies. These forecastsare estimates we made based on information that was available at the currenttime. Actual developments and currently expected results may vary in the event thatassumptions that form the basis for the forecasts do not take place, or risks – forexample, those presented in the Risk Report – actually occur. DB Group does notintend or assume any obligation to update the statements contained in thisManagement Report.

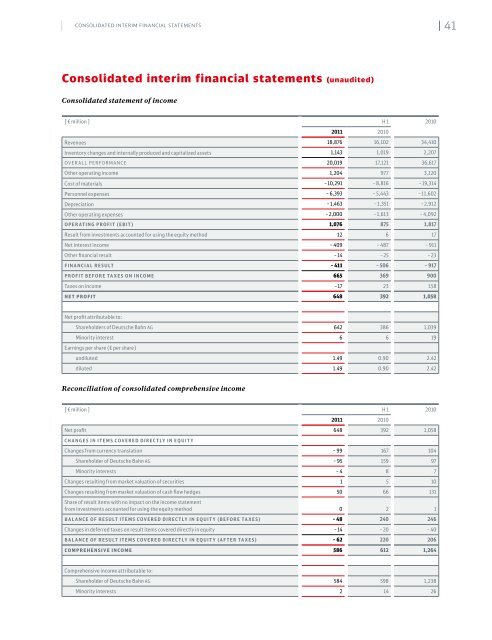

| | Consolidated Interim Financial Statements41Consolidated interim financial statements (unaudited)Consolidated statement of income[ € million ] H 1 20102011 2010Revenues 18,876 16,102 34,410Inventory changes and internally produced and capitalized assets 1,143 1,019 2,207overall performance 20,019 17,121 36,617Other operating income 1,204 977 3,120Cost of materials –10,291 – 8,816 – 19,314Personnel expenses – 6,393 – 5,443 –11,602Depreciation –1,463 –1,351 –2,912Other operating expenses –2,000 –1,613 – 4,092operating profit (EBIT) 1,076 875 1,817Result from investments accounted for using the equity method 12 6 17Net interest income – 409 – 487 – 911Other financial result –14 –25 –23Financial result – 411 – 506 – 917Profit before taxes on income 665 369 900Taxes on income –17 23 158Net profit 648 392 1,058Net profit attributable to:Shareholders of <strong>Deutsche</strong> <strong>Bahn</strong> <strong>AG</strong> 642 386 1,039Minority interest 6 6 19Earnings per share (€ per share)undiluted 1.49 0.90 2.42diluted 1.49 0.90 2.42Reconciliation of consolidated comprehensive income[ € million ] H 1 20102011 2010Net profit 648 392 1,058changes in items covered directly in equityChanges from currency translation – 99 167 104Shareholder of <strong>Deutsche</strong> <strong>Bahn</strong> <strong>AG</strong> – 95 159 97Minority interests –4 8 7Changes resulting from market valuation of securities 1 5 10Changes resulting from market valuation of cash flow hedges 50 66 131Share of result items with no impact on the income statementfrom investments accounted for using the equity method 0 2 1Balance of result items covered directly in equity (before taxes) – 48 240 246Changes in deferred taxes on result items covered directly in equity –14 –20 – 40Balance of result items covered directly in equity (after taxes) – 62 220 206comprehensive income 586 612 1,264Comprehensive income attributable to:Shareholder of <strong>Deutsche</strong> <strong>Bahn</strong> <strong>AG</strong> 584 598 1,238Minority interests 2 14 26