something to smile about? - Euromoney Institutional Investor PLC

something to smile about? - Euromoney Institutional Investor PLC

something to smile about? - Euromoney Institutional Investor PLC

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

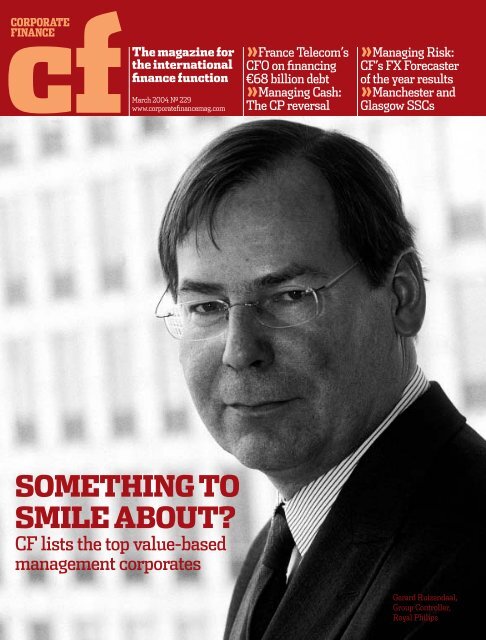

The magazine forthe internationalfinance functionMarch 2004 Nº 229www.corporatefinancemag.com»France Telecom’sCFO on financing€68 billion debt»Managing Cash:The CP reversal»Managing Risk:CF’s FX Forecasterof the year results»Manchester andGlasgow SSCsSOMETHING TOSMILE ABOUT?CF lists the <strong>to</strong>p value-basedmanagement corporatesGerard Ruizendaal,Group Controller,Royal Philips

EDITOR’SNOTEFor the finance executiveMarch 2004Issue 229Edi<strong>to</strong>r Tabitha NevilleDeputy edi<strong>to</strong>r Robert PinkReporters Monica Woodley, Jason EdenProduction edi<strong>to</strong>r Emma PearceResearch edi<strong>to</strong>r Sarah ChuleCover pho<strong>to</strong>graphy Maarten UdemaIllustrations Russ TudorHead of sales Graham CombeAdvertising managersDan Brennan, Jonathan WrightMarketing manager Maeve DohertyPublisher Will GoodhartCorporate FinanceNes<strong>to</strong>r House, Playhouse YardLondon EC4V 5EX, UKSwitchboard: +44 20 7779 8888Advertising: +44 20 7779 8715Fax: +44 20 7779 7971E-mail: gcombe@euromoneyplc.comFor subscription information please contac<strong>to</strong>ur hotline on +44 207 779 8999Corporate Finance is published by<strong>Euromoney</strong> <strong>Institutional</strong> Inves<strong>to</strong>r plc,Nes<strong>to</strong>r House, Playhouse Yard,London EC4V 5EX, UK.Annual subscription rate: US$534/£318(UK only)/€520. ISSN 0958-2053USPS No. 745-890. Periodicals PostagePaid at Rahway, NJThis publication is not included in theCLA license. Copying without permissionof the publisher is prohibited.Direc<strong>to</strong>rs Padraic Fallon (Chairman andedi<strong>to</strong>r-in-chief), The Viscount Rothermere,Sir Patrick Sergeant, Richard Ensor(managing direc<strong>to</strong>r), CJ Sinclair, NeilOsborn, Chris<strong>to</strong>pher Brown, Dan Cohen,Gerard Strahan, JP Williams, John Botts,Edoardo Bounous, Colin Jones, Simon Brady,Tom Lamont, Diane Alfano, Gary Mueller,John Bolsover, Mike Carroll.Printed by The Grange Press in the UK.Cus<strong>to</strong>mer services UK: Tel: +44 20 77798610; Subscription and book sales in NorthAmerica <strong>to</strong>: US hotline, Tel: +1 800 437 9997.©<strong>Euromoney</strong> <strong>Institutional</strong> Inves<strong>to</strong>r plc,London 2002. Although <strong>Euromoney</strong><strong>Institutional</strong> Inves<strong>to</strong>r plc has made everyeffort <strong>to</strong> ensure the accuracy of thispublication, neither it nor any contribu<strong>to</strong>r canaccept any legal responsibility whatsoever forconsequences that may arise from errors oromissions or any opinions or advice given.The publication is not a substitute forprofessional advice on a specific transaction.Next publication date: April 2004Cash, cash and cashShareholder value is a mantrathat gained sway many years ago.But almost as soon as the phrasehad been coined, detrac<strong>to</strong>rs began<strong>to</strong> ridicule the reality of theconcept, claiming that mostcompanies simply paid lip service<strong>to</strong> the idea of building value fortheir shareholders. CF’s covers<strong>to</strong>ry reveals that – for somecompanies at least – shareholdervalue is more than just rhe<strong>to</strong>ric.In association with globalconsultants Stern Stewart, CF hassurveyed corporates in the US,Europe and Japan on a marketvalue-added (MVA) performancebasis. MVA is a measure of excesscash generated by a company andso a positive MVA is a sign that acompany has managed its cashwell and that shareholders canbreathe easy <strong>about</strong> how theircompany is being run.But MVA is more than just ameasure <strong>to</strong> see if a corporate isspending and using money wisely.In a corporate world gripped bygovernance fever, it is just theapproach a company needs <strong>to</strong>adopt <strong>to</strong> prevent money goingastray and accounting scandals.So how do corporates defineand measure shareholder valuecreation? Tabitha Neville talks <strong>to</strong>some of the <strong>to</strong>p 75 companies onpage 22 <strong>to</strong> find out and revealswhich CFOs really know how <strong>to</strong>manage cash.In CF’s Managing Cash featureon page 34 we look at short-termdebt, with a particular focus oncommercial paper. The CP marketis currently a shadow of its formerself. A combination of ratingsdowngrades and the economicslowdown has seen the size of theUS market fall <strong>to</strong> $1.3 trillion - thelowest level since 1999. So whatare corporates doing <strong>to</strong> fund theirshort-term debt? Those who canmuster the ratings are still usingCP – and banks and ratingagencies all claim that an upswingis just around the corner – butalternative short-term debtfinancing solutions are availableas Robert Pink discovers.On page 30, Jason Eden puts FXforecasters <strong>to</strong> the test in CF’sManaging Risk feature and revealsCF’s Forecaster of the year. Howaccurate are the forecasts theyprovide and what currencies havetaken them by surprise over thelast 12 months? cfEdi<strong>to</strong>rial tneville@euromoneyplc.comFor reprints of any article in this issueplease contact Liz Onisiforou:+44 (0)20 7779 8591 or eoni@euromoneyplc.comcorporatefinancemag.com March 2004 cf 1

CONTENTSMARCH 200422 Lead s<strong>to</strong>ryThe value creationequationThe mantra of shareholdervalue gained momentum someyears ago. But whichcompanies have embraced theconcepts behind managing forvalue? And how do youmeasure it anyway? TabithaNeville reports.PHOTOGRAPHY: MAARTEN UDEMA4 Month in ReviewHad a busy month? Then enjoy our bite-sizednews for the over-stretched finance executive.6 Market FocusJapan’s pharmaceutical industry gets M&Ainjection; Invensys engineers financepackage; trends in high-yield debt; globalconsolidation <strong>to</strong> rise.14 Moving OnGoodyear creates assistant treasurer role forCavanaugh; TippingPoint gets Chibib thetechnophile; ProxyMed recruits veteran;Crudele joins the Gibson team.18 CFO Profile“Financing €68 billiondebt was the easy bit.”Michel Combes, the finance chief at the hear<strong>to</strong>f France Telecom’s sensational reversal offortunes, talks <strong>to</strong> Tabitha Neville <strong>about</strong> debt,destiny and getting the French utility back ontrack with the inves<strong>to</strong>rs.21 Treasurer’s ViewThe technology puzzleAs a corporate treasurer, how do you manage<strong>to</strong> stay abreast of developments in the worldof payments and messaging standardization?With so many different organisationsentering the market Robert Pink decided <strong>to</strong>take s<strong>to</strong>ck.2 cf March 2004 corporatefinancemag.com

CONTENTSMARCH 2004Companiesin this issueABB 12Allegiane Telecom 5Als<strong>to</strong>m 12Amaar Properties 4AngloGold 5Ashanti Goldfields 5AstraZeneca 38Balfour Beatty 36Bank of America 35Belgacom 5BMW 34Cazenove 10Chanin Capital Partners 13China Green 4China Telecom 5Citibank 35Clydesdale Bank 41Coca-cola 24Commerzbank 32Credit Suisse 13DEPFA 37Ea<strong>to</strong>n Corporation 40ExxonMobil 24France Telecom 18France Telecom 5Fujian Zijin Mining Industry 4Fujisawa 8Georgia Pacific 38GFI Group 31Gibson Guitars 19Giorgio Armani 4Goodyear 14Heidelberg Cement 8HSBC 10ING 13InvensysInvensys 12JT International 39KO Communications 5Latham & Watkins 41Lexmark 36Lloyds TSB 30Michelin 39MIDAS 38Novartis 24NTGI 35ONGC 10Pacific American Securities 13Petronus 5Philips 24ProxyMed 17ProxyMed 43Randgold 5RBoS 30S&Ps 34Sasol 5Scottish Development International 41SEB 33SG CIB 34Shanghai Forte 4Shell 23Shinsei 4Siemens 24Singapore Computer Systems 15Singapore Telecommunications 4Societe Generale 30ST Assembly Test Services 13Stern Stewart 24Tetra Pak 38The Final Test Reporter 13The Hackett Group 43The Loan Market Association 43TippingPoint 16Total 24Travelex 10Tyco 4, 35Veolia Water 4Visteon 14Wanadoo 5Weatherford 36Worldwide African 5Investment HoldingsYamanouchi 81231 Goodyear finds a brandnew assistant treasurerMoving On, page 142 Working capitalmanagementManaging Cash, page 343 Northern SSCsTreasury Location, page 3830 Managing Risk:FX Forecaster of the yearHow accurate are your forecasts: CF hascollated the results for its FX Forecaster of theyear survey. So which bank <strong>to</strong>pped the tablefor FX forecasts? Jason Eden finds out.34 Managing Cash:Commercial Paper focusHow are you funding your working capitalneeds? The US commercial paper market hasundergone its largest contraction in 40-years.So how are corporates financing their shorttermneeds? Robert Pink looks at alternativeways of financing short-term debt, anddiscovers why CP is still the best financingsolution for corporates.38 Treasury Location:The UKThe Manchester and Glasgow scene:Corporates are increasingly open <strong>to</strong>suggestion when it comes <strong>to</strong> the location oftheir shared service centres. Taking this onboard, Robert Pink and Jason Eden look <strong>to</strong>Manchester and Glasgow as alternative SSCs.42 Cash & TechEurope’s corporate treasurers look <strong>to</strong> acentralised future.43 Legal BriefLMA launches LBO blueprint; SEC delaysSection 40444 M&A and Fee Analysis47 FX Forecastscorporatefinancemag.com March 2004 cf 3

conducted an internalinvestigation in<strong>to</strong> Tyco. Incourt it was a different s<strong>to</strong>ry.Swartz claimed the $100million paid in bonuses wasearly payment of annualbonuses that Kozlowski had<strong>to</strong>ld him had been approvedby board member PhilHamp<strong>to</strong>n (deceased). Sixformer Tyco direc<strong>to</strong>rs – allvery much alive – say theynever approved them.»The butterfly-effect ofcorporate scandals has nowmade its way <strong>to</strong> thecorridors of the big fouraccountancy firms. A surveyhas revealed the firms arequietly divesting themselvesof their riskiest corporateclients. The prominence ofsmaller companies in theranks of the culledcorporates from theportfolio’s suggests thatthey may be more willing <strong>to</strong>take on risk when the auditfees are far larger.Oops, silly usCF would like <strong>to</strong> apologise <strong>to</strong>Neil and Neal. You really dolook nothing alike:Neil Pres<strong>to</strong>n, companysecretary, Punch TavernsNeal Neilinger, DresdnerKleinwort WassersteinAFRICAThe South Africangovernment has announcedan easing of its exchangecontrols, which will allowforeign firms <strong>to</strong> access itss<strong>to</strong>ck and bond markets.The JSE has been hit byfalling trading volumes soforeign firms will soon beallowed <strong>to</strong> list on SouthAfrican capital markets <strong>to</strong>raise debt and equity financeon the JSE SecuritiesExchange and the BondExchange.»The Ghanaian parliamenthas approved AngloGold’s$1.55 billion all-sharetakeover offer for AshantiGoldfields after theopposition boycotted thevote, saying the deal willreduce the government’sstake below the 10% levelset by legislation. Ashanti’sboard approved the mergerdespite receiving animproved offer of a €1.6billion share swap fromsmaller South Africanmining group Randgold.»South African oil and gasgroup Sasol and Malaysia’sPetronas have agreed amerger between Sasol’sLiquid Fuels Business andEngen, 80% owned byPetronas. The merger will bea joint venture, with eachcompany holding a 37.5%stake. The remaining 25%will be held by blackpartners - as required underSouth Africa’s BlackEconomic Empowermentrules. This includesWorldwide AfricanInvestment Holdings,which owns 20% of Engen,and former shareholders ofExel, a liquid fuels companythat merged with Sasol inDecember 2004.Top Telecoms GroupsRank Company Home Country Mobile Subscribers(million)1 China Mobile China 153.62 Vodafone UK 118.93 China Unicom China 86.64 Cingular/AT&T Wireless US 67.15 Deutsche Telekom Germany 65.86 NTT DoCoMo Japan 50.87 France Telecom France 41.98 America Movil Mexico 36.79 Telefonica Spain 29.910 Verizon US 28.8Source: FTWhat’s happened <strong>to</strong>the telecoms sec<strong>to</strong>r?A month ago the telecomssec<strong>to</strong>r was bobbing alongquite nicely, then bam!All hell breaks loose.First up was the bustlingfor position in the AT&TWireless deal. CingularWireless and Vodafoneboth made plays for thecompany, but Cingularsnatched AT&T last-minutewith a bid for $41 billion –one of the largest cashtransactions in his<strong>to</strong>ry –making it the fourth largesttelecoms group in theworld (see box).Vodafone claims it wasprudent <strong>to</strong> walk away fromthe auction but rumoursabound of its executivesbeing in bed asleep whenthe deal was struck andalso that loose <strong>to</strong>ngues inthe Vodafone camp blastedits offer from the water (itis alleged Vodafone <strong>to</strong>ldreporters that the Vodafoneboard were going <strong>to</strong>approve a bid of $14.50 pershare; Cingular got hold ofthis information and heypres<strong>to</strong> a bid of $15 pershare). What’s thatexpression? Careless talkcosts acquisitionopportunities.»February also saw Belgianincumbent telecomscompany Belgacom putthe finishing <strong>to</strong>uches <strong>to</strong> itsIPO. The €3.5 billion ($4.4billion) share sale will bethe largest IPO in Europe inthe last three years.»France Telecom gotround <strong>to</strong> launching an offer<strong>to</strong> buyout the remaining29.4% of Wanadoo, itsdirec<strong>to</strong>ries and internetservices division. The €3.9billion offer is awaitingWanadoo’s approval.»XO Communications,which emerged fromChapter 11 a year ago,unveiled plans <strong>to</strong> acquireother distressed telecoms.The company has just wonan auction for the bulk ofAllegiane Telecom’s assetsfor $628 million.»China Telecom may raiseas much as $3 billionthrough a share placing <strong>to</strong>fund the acquisition of 11regional telecom networksfrom its state-owned parentcompany, which would add45 million users <strong>to</strong> itssubscriber base.corporatefinancemag.com March 2004 cf 5

MARKETFOCUSStrike whilehigh yield’s hot»Issue volume hit €16.6billion in 2003»Move from refinancingactivity <strong>to</strong> find M&AThe high yield market inEurope was the turnarounds<strong>to</strong>ry of 2003. New issuevolume hit a record high of€16.3 billion after amiserable two years. Whatcan issuers expect this year?Standard & Poor’s saysthat prospects of a cyclicalrecovery, a continuedaccommodative monetarypolicy stance, decliningdefault rates, and aslowdown in credit qualitydeterioration in theEuropean high yield marketwill mean that corporatesshould have strongconditions in which <strong>to</strong> issuein – though S&P also notesthat corporate downgradescontinue <strong>to</strong> be substantiallyhigher than upgrades.“Conditions remainfavourable in Europe,” saysDiane Vazza, managingdirec<strong>to</strong>r in global fixedincome research at S&P inNew York. “Monetary policyis really helping <strong>to</strong> keep itthat way.” StephaneTremelot, head of creditsyndicate at BNP Paribas inLondon, agrees that “slow[erthan expected] economicgrowth in the eurozone andthe dollar/euro exchangerate mean that it is unlikelythat the ECB will raise ratesin the short term. Thatmeans that there is anopportunity for issuers <strong>to</strong>benefit from issuing bondswith low yields.”Even if rates do rise, itdoesn’t necessarily spell anend <strong>to</strong> issuance, according<strong>to</strong> Nicholas Coates, head ofhigh yield at RBS in London.“Some issuers may makeopportunistic moves <strong>to</strong> dodeals before rate rises takeplace but issuers can alwaysuse the swap market <strong>to</strong> getcomparatively lowerfloating rates.”While spreads in the UShigh yield market havewidened by around 8bpsince the beginning of theyear, in Europe they havecontinued <strong>to</strong> tighten and arearound 38bp tighter than atthe end of 2002, according<strong>to</strong> Tremelot. Indeed, theaverage absolute yield forEuropean issues remainslower in Europe at 7.44%than in the US at 7.87%.Some market observersfear that Europe is <strong>about</strong> <strong>to</strong>succumb <strong>to</strong> the problemstroubling the US market,where fund flowsinformation provider AMGData Services has reportednet outflows from highyield funds in the US forthree of the four weeks <strong>to</strong>February 25. While theseoutflows are specific – andthus far isolated – <strong>to</strong> USfunds, their impact is morewidely felt: many of thosefunds also invest in theEuropean market; andtrends in the US high yieldmarket frequently pre-emptthose in Europe.Nevertheless, S&P’s Vazza– and most market observers– say that this is just ahiccup. “Inves<strong>to</strong>r demand isstill there but there has beena realisation that corporatespreads have tightened <strong>to</strong>ofast compared <strong>to</strong> creditquality and that there was aneed <strong>to</strong> set that right.”Coates adds: “Whilst theEuropean high yield markethas softened over the pastmonth, we believe this <strong>to</strong> bea temporary phenomenon: acorrection <strong>to</strong> a bullishmarket. The long-term trendis for increased liquidity inEurope and demand willremain strong as fundscontinue <strong>to</strong> flow in<strong>to</strong> themarket.” More bullishcommenta<strong>to</strong>rs say that thesoftening of the market hasresulted from inves<strong>to</strong>rsselling bonds in order <strong>to</strong>have cash <strong>to</strong> respond <strong>to</strong> theexpected deluge of newissuance expected.Either way, no-oneexpects the high yieldmarkets in Europe <strong>to</strong>flounder this year. IssuanceYTD has been limited –around €2 billion from 10deals compared <strong>to</strong> $25billion from around 100deals in the US – but BNPParibas’ Tremelot says thatthis is common for thisperiod of the year. “Unlikethe high grade world Januaryand February are quietmonths as issuers and banksprepare new transactions.”While it is impossible <strong>to</strong>know if we are at thebot<strong>to</strong>m of the credit cycle,all the indica<strong>to</strong>rs show thatthe economy is improving,credit quality is improving,and inves<strong>to</strong>r demand isn’t<strong>about</strong> <strong>to</strong> collapse.And while all thesefac<strong>to</strong>rs may be pullingissuers <strong>to</strong> the high yieldmarket, the long-termstructural trend of reducedbank lending – not leastbecause of Basel II – is alsopushing issuers <strong>to</strong>ward it.“European corporatesincreasingly view thehigh yield product as amainstream financing<strong>to</strong>ol.”Nicholas Coates, RBS“Banks have become muchmore focused on the riskadjusted returns of theircredit provision and areoften less resistant than theyhave been in the past <strong>to</strong>corporates diversifying theirsources of funding awayfrom the bank market,” saysRBS’s Coates. “That is asignificant change.”Who’s issuing?The high yield market hastraditionally been driven bythree sources of issuance –leveraged buyouts (LBO),telecom, media andtechnology (TMT) andgeneral corporate issuance.“For the first time thesethree components of theprimary high yield marketin Europe will produce dealssimultaneously this year.That means that we canexpect a strong level ofissuance,” says Coates.LBO issuance is expected<strong>to</strong> provide a quarter of themarket in 2004 while TMTissuance should match lastyear issuance of almost €6billion. But the key <strong>to</strong> thepotential market growth iscorporate issuance.One of the main reasonsfor the growth of theEuropean high yield marketin 2003 was issuance fromfallen angels – issuers thathave fallen <strong>to</strong> speculative(rated BB+ and below by S&Pand Ba1 by Moody’s) frominvestment grade (BBB- andabove by S&P and Baa3 byMoody’s). Of the <strong>to</strong>tal €16.3billion raised in Europe,fallen angels accounted for6 cf March 2004 corporatefinancemag.com

€6.4 billion or 40%. S&Ppoints out that that is a 25%increase on 2002 figures. Asa direct consequence ofincreased fallen angelissuance the average dealsize in the European highyield market increased from€251 million in 2002 <strong>to</strong> €286million in 2003.Inves<strong>to</strong>rs have beenunderstandably eager <strong>to</strong> buypaper from such issuers.“HeidelbergCement came <strong>to</strong>the market at a time wheninves<strong>to</strong>rs were looking for away <strong>to</strong> get a better yield ontheir investments,” saysChristian Kammann, grouptreasurer at the company.“HeidelbergCement alsostrongly pointed out thecommitment <strong>to</strong> go back <strong>to</strong>investment grade. The dealbrought by us was thelargest European high yielddeal then and in many waysset a market standard.”Issuance from fallenangels has not only swollenthe market’s overall size ithas coaxed other issuers in<strong>to</strong>the market. “Issuance fromhigh quality borrowers suchas HeidelbergCement andVivendi in 2003 helped <strong>to</strong>‘destigmatise’ the marketand it’s now a lot easier forCFOs <strong>to</strong> justify using themarket <strong>to</strong> their boards,” saysCoates. “The corporatesec<strong>to</strong>r will continue <strong>to</strong> bebuoyant as Europeancorporates increasingly viewthe high yield product as amainstream financing <strong>to</strong>ol.”The use of that financingis expected <strong>to</strong> change, saysS&P’s Vazza. “The focus isshifting from refinancing <strong>to</strong>capital spending. It can beexpected that the Europeanmarket will follow the US inthe move away fromrefinancing activity <strong>to</strong> fundexpenditure and M&Aactivity.” LNEurope – Structure changes benefit issuersThe European high yieldmarket has traditionallybeen dominated by 10-yearbonds with a five-year noncall.If issuers wanted <strong>to</strong>redeem before that five-yearcall they would have <strong>to</strong>tender for the bonds – acostly process most wereeager <strong>to</strong> avoid. The rationalewas that a five-year call gaveissuers reasonable flexibility<strong>to</strong> get their finances inorder and work their wayback <strong>to</strong> investment gradewhile inves<strong>to</strong>rs would notget unduly punished bycompanies eager <strong>to</strong>refinance debt once theircredit quality hadimproved.Issuers are now in poleposition, with vastly moredemand than new issuesupply. As a consequence,issuers have been able <strong>to</strong>get better terms frominves<strong>to</strong>rs. Instead of 10-yeardeals, issuers have begun <strong>to</strong>bring seven- or eight-yeardeals. Crucially, the calls onthese bonds are also shorter– giving finance executives’greater flexibility <strong>to</strong>refinance should theirfinancial and ratingposition improve.There has been a move<strong>to</strong>ward seven-year bondswith a four-year non-call athalf-coupon meaning thatinves<strong>to</strong>rs get half thecoupon rate if the bonds arecalled. A number of issueshave also come with threeyearnon-calls at fullTimetable of a high yield bondHigh yield bonds takelonger <strong>to</strong> come <strong>to</strong> marketthan investment gradebonds for a number ofreasons. Chief among theseis that issuers arefrequently unrated beforethey issue. Meanwhile, thedocumentation andoffering circular must beput <strong>to</strong>gether by the issuer’sinvestment bank.Choosing your market isa key decision saysChristian Kammann, grouptreasurer atHeidelbergCement. He saysissuers should weigh upboth the cost and inves<strong>to</strong>rfamiliarity benefits. “TheEuropean inves<strong>to</strong>r base wasmore familiar <strong>to</strong> theHeidelbergCement credit.”He adds that the complexlegal environment in theUS market dissuaded thecompany from issuingthere. Simply printing a“144A issue [allowing thesale of a non-US marketbond <strong>to</strong> qualified USinves<strong>to</strong>rs] makes the duediligence process moreextensive”. Although itallows issuers <strong>to</strong> benefitfrom the price tension thatreaching a broader inves<strong>to</strong>rbase creates.A further timeconsuming element of highyield bonds is that thecovenant package offered<strong>to</strong> inves<strong>to</strong>rs is frequentlymore complex than withinvestment grade issues.High yield issuers have ahigher risk of default andtherefore inves<strong>to</strong>rs requiregreater protection, asKammann explains. “Highcoupon. Issuers might have<strong>to</strong> pay a bit more <strong>to</strong> get thiseven shorter call, but i<strong>to</strong>ffers them an enormousflexibility advantage over atraditional 10 year non-callfive bond. Understandably,inves<strong>to</strong>rs are unhappy withthe changes but concedethat they are a function ofan efficient market.S&P notes the near-termoutlook for European highyield is benign “with theoutlook and CreditWatchdistribution indicating animprovement in creditquality relative <strong>to</strong> a yearago”. Only 25% ofspeculative rated issuerscurrently have a negativebias, compared <strong>to</strong> 30% ayear earlier.yield inves<strong>to</strong>rs are morefocused on covenants andprotecting or keeping thecash flow in the companyfor debt reduction thatresults in a much moredetailed indenture.”The less developednature of the market alsomeans that some covenantpackages become a matterof negotiation withinves<strong>to</strong>rs rather thansimply being drafted by theissuer. “Familiarity with thehigh-yield style ofdocumentation and crosscheckingwithoperational/strategic needsof the issuer group arevital,” Kammann says.From the awarding ofthe mandate <strong>to</strong> completion,a high yield issue shouldtake around two months.corporatefinancemag.com March 2004 cf 7

MARKETFOCUSDeal of the month: Yamanouchi PharmaceuticalPharma’s strength in numbersDEAL AT A GLANCE» $8 billion merger ofJapanese pharmas» Pharma consolidation inJapan set <strong>to</strong> risePharmaceutical companiesYamanouchi and Fujisawaagreed an $8 billion mergercreating Japan’s secondlargest pharma entity inFebruary.Yamanouchi andFujisawa PharmaceuticalsJapan’s third- and fifthrankeddrug makersrespectively, aim <strong>to</strong> reachan agreement by March2004 and integrateoperations by early 2005.Enhancing R&D andmarketing opportunitiesare the principal fac<strong>to</strong>rsbehind the merger whichwill see each Fujisawa shareexchanged for 0.71Yamanouchi shares. Thedeal will create the 17thlargest firm in the globalmarket. “From a businesspoint of view most peoplehave said it’s a very goodcombination, as well asfrom a geographic point ofview,” said a bankingsource close <strong>to</strong> the deal.Japan is the secondlargest pharmaceuticalmarket after the US, withsales of around $52 billionin 2002. Yet Japanesepharmas have never beenviewed as global players.Yamanouchi , for example,has been struggling in theUnited States. A core reasonfor this, is R&D spend. Theratio of R&D <strong>to</strong> <strong>to</strong>tal sales in2002 was 12.8% for Japan’spharmaceuticals,compared <strong>to</strong> an average ofover 17% for Westerncounterparts. And bylimiting the influence offoreign competition inJapan, governmentprotection has furtherlimited R&D investment <strong>to</strong>below that of foreign rivals.The merger will, analystshope, address the imbalance.(The acquisition of Pfizer byPharmacia in 2002 createdan R&D budget worth $6.5billion. The combined R&Dbudget for Yamanouchi andFujisawa will be ¥150 billion($1.3 billion)).“The merger shouldimprove the competitivenessof the new entity,”comments ShinsukeTanimo<strong>to</strong>, an analyst forMoody’s Japan. “The increasein the size of the businesswill, on a global basis,broaden sales coverage andstrengthen R&D capabilities.”It may also spark off moresec<strong>to</strong>r consolidation.Yamanouchi and Fujisawahave both admitted thatthey needed <strong>to</strong> merge <strong>to</strong>fend off overseascompetition in the world’ssecond-largest drugs market.And with the governmentactively promoting foreignshare-ownership andcompetition in the marketand western companiessuch as Merck, GSK andPfizer expanding theirmarketing in Japan, it islikely other Japanesecompanies will follow in itsfootsteps. Tanimo<strong>to</strong> agrees:“The merger of Yamanouchiand Fujisawa could affectthe balance of the marketcompetitiveness in the <strong>to</strong>ptier players and mightaccelerate marketreorganisation.”Japan’s government isalso in the mood for change.It is has publicly stated thatit wants <strong>to</strong> see consolidationin the industry. It is slashingboth the number of drugswhich can be sold only byprescription, and theamount paid for drugsthrough the national healthsystem, both changes whichweaken domestic drugmakers in their battle withforeign drug companies.Yamanouchi’s president,Toichi Takenaka, willbecome chief executive ofthe new company, whichwill retain his company’sname. Fujisawa’s president,Hatsuo Aoki, will becomechairman.Morgan Stanley Japanadvised Yamanouchi;Lehman Brothers Japanadvised Fujisawa. RPGlobal Pharmaceutical sales by Region, 2002 (US$ bn)World Audited Market Sales Global Sales % Growth %North America 203.6 51 12Europe (EU) 90.6 22 8Rest of Europe 11.3 3 9Japan 46.9 12 1Asia, Africa and Australia 31.6 8 11Latin America 16.5 4 -10Total 400.6 100 8Source: IMS World Review 2003 and IMS ConsultingCOMPANY INFOYamanouchi is strong in ulcerand urinary treatments and isbest known for Harnal, amedicine for urinaryproblems. It was founded in1923; has capital ¥99,760million; <strong>to</strong>tal assets ¥890,525million; and 8,957 employees.»Fujisawa makes theimmuno-suppressant drugPrograf, and focuses onimmune-related treatments. Itwas founded in 1930; hascapital ¥38,589 million; <strong>to</strong>talassets ¥508,354 million; and8,059 employees.»Combined sales ofYamanouchi and Fujisawa inthe current financial year <strong>to</strong>March 2004 will likely reach¥920 billion ($8.4 billiondollars).»The two companies have¥890 billion in combinedsales, and the deal will allowthem <strong>to</strong> surpass the onetrillion mark. It will have thelargest market share amongJapanese pharmaceuticalcompanies.»It will be 17th in the globalpharmaceutical market»The combined companywill: have an annual R&Dbudget in excess of ¥150billion;have more than onetrillion yen for sales; and 25%as an operating margin.»In 1995 overseasshareholders held 17.1% ofYamanouchi s<strong>to</strong>ck. By 2002the figure had risen <strong>to</strong> 44.7%.Takeda, Japan’s leadingpharmaceutical, has seenforeign share ownership risefrom 10.1% <strong>to</strong> 29.6% in thesame period.8 cf March 2004 corporatefinancemag.com

Global consolidationefforts set <strong>to</strong> rise»Increased earningsencourage acquisitions»389 deals <strong>to</strong>talling $21.5billion in tech sec<strong>to</strong>r YTDIn a scene akin <strong>to</strong> the lastdance at a disco witheveryone scrambling <strong>to</strong> finda partner, corporates can beseen scanning the landscapefor acquisition opportunitieshoping <strong>to</strong> cherry pickvictims before the M&Aspree really kicks off.Year-<strong>to</strong>-date more than$350 billion of proposedacquisitions have beenannounced - more thanthree times the amount inthe same period for 2003.Some of this can beaccounted for by deals thathave been moving throughthe investment bankingpipeline for some time andare finally coming <strong>to</strong> a close,but s<strong>to</strong>ck market rallies, lowinterest rates and renewedoptimism in the dealmakingenvironment are allhelping <strong>to</strong> push corporates<strong>to</strong> make M&A decisions.“Companies have beenfocused on their balancesheets and earnings for thelast few years, but now thatearnings are growing againand their internal problemsare fixed, they are looking <strong>to</strong>grow and the best way <strong>to</strong>grow and the best way <strong>to</strong> dothat quickly is throughM&A,” says RichardMorgner, head of mergersand acquisitions atinvestment bankingboutique Chanin CapitalPartners. It seems the boardsof technology and telecomsfirms as well as of financialinstitutions are of the samemind. The tech sec<strong>to</strong>r hasseen 389 deals <strong>to</strong>talling$21.5 billion YTD, while inthe finance sec<strong>to</strong>r, therehave been 132 deals<strong>to</strong>talling $111.6 billion YTD.TechnologyWithin the tech sec<strong>to</strong>r, thesemiconduc<strong>to</strong>r industry hasseen a spate of acquisitionssuch as Singapore statecontrolledST Assembly TestServices (Stats) purchase ofUS-based ChipPAC for $1.6billion in February.“The wholesemiconduc<strong>to</strong>rmanufacturing side of thebusiness is getting <strong>to</strong> wherethe investments <strong>to</strong> domanufacturing are so high,you’ve just got <strong>to</strong> have a bigcompany <strong>to</strong> play in thegame,” says industryobserver Jim Mulady,publisher of The Final TestReporter, a semiconduc<strong>to</strong>rindustry newsletter.Consolidation in thesemiconduc<strong>to</strong>rmanufacturing industry isnecessary <strong>to</strong> contain costsand increase efficiency, headds.Acquisitions in thesemiconduc<strong>to</strong>r sec<strong>to</strong>r arefollowing an increasingtrend <strong>to</strong>wards outsourcingby integrated devicemanufacturers (IDMs) - largechip companies that havetraditionally designed,manufactured, tested andassembled semiconduc<strong>to</strong>rs -who now need <strong>to</strong> streamlinetheir operations <strong>to</strong> helptheir cost competitiveness.A recent report fromMorgan Stanley’s GlobalSemiconduc<strong>to</strong>r ResearchTeam says that by 2010, thesemiconduc<strong>to</strong>r industry willgrow <strong>to</strong> $360 billion with34% of the industry drivenby outsourcing revenue.“Streamlining can bedone easily throughoutsourcing and assemblyand testing are good areas <strong>to</strong>outsource because theyrequire less disclosure ofproprietary information,”says Chris Hsieh, regionalhead of Asian technologyresearch at ING in Taipei.Outside of thesemiconduc<strong>to</strong>r industry,there have been severalother major acquisitions,such as US Internet systemsprovider Juniper Networks’spurchase of US networksecurity provider Netscreenfor $3.6 billion. The dealinvolves 1,404 shares ofs<strong>to</strong>ck for each of Netscreen’sshares.Michael Cohen, direc<strong>to</strong>rof research for PacificAmerican Securities, saysthe Juniper acquisition is aperfect example of howsome larger tech companiesare willing <strong>to</strong> use theirshares <strong>to</strong> do deals. As such,he predicts “there will bemore acquisitions <strong>to</strong> comesince many tech s<strong>to</strong>ckssurged last year.”Financial InstitutionsFollowing the announced$58 billion merger ofJPMorgan Chase andBankOne, and Bank ofAmerica’s acquisition ofFleetBos<strong>to</strong>n Financial for$43 billion, the financialSo begins the consolidationinstitutions sec<strong>to</strong>r is rifewith speculation of moreM&A activity <strong>to</strong> come.In a recent pan-Europeanstudy, Credit Suisse analystssaid that with economiesrecovering, capital buildingup and questions over futureearnings growth “somemanagement teams maynow feel under pressure <strong>to</strong>turn <strong>to</strong> acquisitions as a wayof boosting earnings”.Co-CEO of Credit SuisseOswald Grubel has said hesees opportunities foracquisition-led expansion inGermany and MBNA EuropeCEO General Charles Krulakis expecting furtherconsolidation in the creditcard business, following hiscompany’s purchase of thecredit card books of UKbanks Abbey and Alliance &Leicester (A&L).“Over a period of timethere will be banks whoissue credit cards right nowwho say maybe the ideawould be <strong>to</strong> do <strong>something</strong>like Abbey and A&L havedone. I think you will seeconsolidation.“The questions regardingEgg [which has been put upfor auction by Prudential]are an example of that,where you have a very nicebusiness that is owned by ashareholder who is sayingmaybe someone else can dothis,” adds Krulak.Meanwhile, BNP ParibasCEO Baudouin Prot says heis “actively searching” foracquisitions <strong>to</strong> follow thepattern set by the €9 billionof deals done by the banksince the merger of BNP andParibas in 1999. MWcorporatefinancemag.com March 2004 cf 10

MARKETFOCUSIndian government pavesway for privatisation» Biggest off-loading ofshares undertaken» Privatisation <strong>to</strong>regenerate state-ownedindustry» ONGC 10% stake saleMarch 2004 is gearing up <strong>to</strong>be a busy month in theIndian equity markets. Somuch so that inves<strong>to</strong>rs havealready nicknamed itprivatization month.Privatization month willsee the biggest off-loading ofshares ever undertaken bythe Indian government (orany government worldwide)– it will divest more than $3billion of state-owned s<strong>to</strong>ck.If the part-privatization isIn brief»Nokia plans <strong>to</strong> buy outPsion’s share in Symbian,in a move <strong>to</strong> consolidate itsinfluence on the operatingsystem used in mostEuropean smart phones.The £135.7 million dealwould increase Nokia’sstake from 32.2% <strong>to</strong> 63.3%,but it is facing strongopposition from Psion’slargest shareholder whosays an IPO of Symbianshould be consideredinstead.»Juniper Networks is <strong>to</strong>acquire network-securitysoftware maker NetScreenTechnologies for $3.6billion in s<strong>to</strong>ck. Juniper hasbeen buoyed by a recoveryin the telecoms sec<strong>to</strong>r. Itfully subscribed it willbecome the largest equityplacement in India’s capitalmarket his<strong>to</strong>ry.The equity sale formspart of a governmentinitiative designed <strong>to</strong>regenerate a percentage ofthe country’s hither<strong>to</strong>traditionally state-ownedand controlled industries.By selling a proportion oftheir share holdings,expanding the capitalmarket base and increasingliquidity, the IndianGovernment hopes <strong>to</strong>attract foreign investmentand intellectual expertise.“The government islooking <strong>to</strong> establishreported fourth quarter netincome of $14.7 million upfrom $8.5 million.»Singapore-based STAssembly Test Servicesmade a $1.6 billion bid forSilicon Valley’s ChiPAC. Thedeal will create the thirdlargestcompany in the chipassembly and test services“back-end” service providermarket behind Amkortechnologies and AdvancedSemiconduc<strong>to</strong>r Engineering.»Diners Club Malaysiaannounced the first assetbackedsecuritization for itscharge card receivables inMalaysia with the issuanceof Domayne AssetCorporation Bhd’s (DACB)RM132 million ($34.7million) Medium TermNotes of 3.5 years tenure.widespread ownership, andeventually, a <strong>to</strong>taldivestment in companiesthat it perceives as being innon-core areas, i.e. sec<strong>to</strong>rsthat are not classified asaffecting national security,”says Ravi Menon, direc<strong>to</strong>r ofinvestment banking atHSBC in Mumbai.“This is all part of agovernment initiative thatreally kicked off in June2003, when the IPO fromMaruti began <strong>to</strong> open up thedomestic equity markets <strong>to</strong>foreign institutionalinves<strong>to</strong>rs,” says YogeshShetty, group direc<strong>to</strong>r ofcommercial foreignexchange at Travelex.Diners Club Malaysia willsell its charge cardreceivables on a revolvingbasis <strong>to</strong> DACB which will, inturn, raise the financing bydeclaring a trust over thesereceivables and issuingMTNs. This is the firstsecuritization deal of itskind in Malaysia.»Russia’s sixth-largest oilcompany, OAO Tatneft,won approval from theTurkish government <strong>to</strong> buya majority of oil refinerTupras for $1.3 billion.Tupras controls 87% ofTurkey’s refining market.»Enersur, the Peruvianbasedsubsidiary of Belgianenergy company Tractebel,won a 30-year concessionfrom the Peruviangovernment for the 130MWThe government’s jewelin the crown, and ahighlight of privatisationmonth, will be the publicoffering of a 10% stake inthe Oil and Natural GasCorporation (ONGC) India’slargest domestic companyby market capitalisation,worth an estimated $2.5billion. The governmen<strong>to</strong>wns 84% of ONGC atpresent and will retain amajority stake in thecompany, along witheffective control after thesale is completed.Other state-ownedheavyweights hitting themarkets in March includeGail, the largest gasdistribu<strong>to</strong>r, the Bank ofMaharashtra, IBP, the oilretailer, and the DredgingCorporation.The Government hastried and failed in the past<strong>to</strong> partly privatise some ofIndia’s largest state-ownedYuncan hydroelectricproject. Enersur bid $53million. Norway’s statepower company Statkraftand the US-based PSEGdeclined <strong>to</strong> take part in thebid.»Financing for the largestpipeline project in his<strong>to</strong>ry –the $3.65 billion Baku-Tbilisi-Cayhan – wascompleted in February. Thefinancing for the projectwhich spans threejurisdictions and over 1700km, needed 17,000signatures <strong>to</strong> be finalised.The project is beingdeveloped <strong>to</strong> provide aprimary export route for oilproduced off-shoreAzerbaijan.»Suez-Tractebel ofBelgium and Mimag of11 cf March 2004 corporatefinancemag.com

Follow-ons by Indian Issuers 01/01/00 - 20/02/04Amt. m (US$)Iss.2000 1st Quarter 499.49 42000 2nd Quarter 108.75 12000 3rd Quarter 86.38 22000 4th Quarter 130.85 12001 1st Quarter 0.00 02001 2nd Quarter 294.69 22001 3rd Quarter 172.50 12001 4th Quarter 0.00 02002 1st Quarter 0.00 02002 2nd Quarter 0.00 02002 3rd Quarter 50.00 12003 1st Quarter 0.00 02003 2nd Quarter 0.00 02003 3rd Quarter 346.25 22003 4th Quarter 87.97 22004 1st Quarter 0.00 0companies – in February2002 it privatised VNSL(Videsh Sanchar NigamLimited), one of India’slargest ISP providers, withonly limited success. Menonbelieves the government’stiming is better this timearound.India is emerging as oneof the fastest growingeconomies in the world,propelled by risingIn briefTurkey, closed a $475million financing for theBaymina power projectnear Ankara, Turkey.»Fiat’s asset sale programwas completed in Februarywith the sale of 70% of FiatEngineering <strong>to</strong> privatelyheld Maire Holding for€80.5 million ($101.7million). In 2003 thecompany sold insurancecompany ToroAssicurazioni <strong>to</strong> publisherDe Agostini for €2.4 billionand Fiat Avio for €1.4billion <strong>to</strong> the CarlyleGroup and Finmeccanica.»Singapore saw its largestIPO of the year in February.UTAC’s offer was 32.5consumption, and therecord inflow of foreigninvestment. GDP is expected<strong>to</strong> hit 7.5% in the fiscal year<strong>to</strong> March. This figure is wayabove anything theEurozone or America canhope <strong>to</strong> achieve. As for thetiming of the sell-offs, itcould not be better: theequity capital markets haveexperienced anunprecedented bull run intimes oversubscribed. Thesemiconduc<strong>to</strong>r test andassembly company raisedS$182.6 million ($107million).»Las Vegas-based BoydGaming is <strong>to</strong> buy rival CoastCasinos for $1.3 billion incash, s<strong>to</strong>ck and debt.»Brazil’s two largestairlines Varig and Tamhave decided againstmerging. They spent a yearnegotiating, unsuccessfully,<strong>to</strong> deal with a complexownership structure, largedebt and legal challenges.They will instead form asmall joint venture andexpand their code-sharingarrangement.»The Mexican governmenthas approved Spanish bankSOURCE: DEALOGICIndian IPO Quarterly Breakdown 01/01/00 - 20/02/04Amt. m (US$)Iss.2000 1st Quarter 29.78 32000 2nd Quarter 66.34 32000 3rd Quarter 22.37 12000 4th Quarter 50.85 62001 1st Quarter 44.83 52001 3rd Quarter 0.96 12002 1st Quarter 205.72 22002 2nd Quarter 42.85 12002 3rd Quarter 59.19 12002 4th Quarter 92.51 22003 1st Quarter 9.91 12003 2nd Quarter 213.66 12003 3rd Quarter 63.15 42003 4th Quarter 72.38 22004 1st Quarter 150.18 3the last six months (theysaw a 60% rise in 2003). “It’sa great time for thegovernment <strong>to</strong> act. Thesefac<strong>to</strong>rs ensure that inves<strong>to</strong>rsare subscribing, and thegovernment gets a greatprice for its divested s<strong>to</strong>ck,”says Menon.The performance of oneof the first deals <strong>to</strong> hit themarkets certainly bodeswell. PetrochemicalBBVA’s $4.2 billion offer <strong>to</strong>buy the remaining 40.6% ofMexico’s BBVA Bancomerthat it does not own. Thiswill take BBVA Bancomerout of the Mexico City s<strong>to</strong>ckmarket, where it is thelargest financial servicess<strong>to</strong>ck accounting for 85% ofthe financial services index.This deal, in combinationwith the recent buyout ofMexican cement firmApasco by Swiss Holcim,will reduce the liquidity ofthe Mexican s<strong>to</strong>ck exchangeby 10%, according <strong>to</strong>analysis by UBS Warburg.»PwC expects the volumeof IPOs in China <strong>to</strong> grow by70% in 2004. The firmbelieves 100 companies willgo public in Hong Kong in2004, raising approximatelyHK$100 billion ($12.9company IPCL’s shares havesoared 97.8% over the last 12months and the offeringwas healthilyoversubscribed by 10% asinves<strong>to</strong>rs flocked <strong>to</strong> whatthey see as stable companieswith under-valuationmandates. “Many of thesecompanies are extremelyhealthy and are blue-chip intheir own right,” saysMenon. JEbillion) compared <strong>to</strong> HK$59billion raised in 2003. IPOsby Chinese companiescould account for 80% offunds raised in Hong Kong,with large listings expectedfrom China ConstructionBank and Minsheng Bank.»Aventis, the Franco-German pharmaceuticalcompany fending off a €46billion bid from Sanofi-Synthelabo, has gone onthe offensive. It hasannounced plans <strong>to</strong> buybackbetween €2 <strong>to</strong>3 billionof shares, and dispose ofnon-strategic products inan effort <strong>to</strong> streamline thebusiness. Aventis’schairman, Igor Landau,says that Sanofi’s €46billion offer hadfundamentallyundervalued the group.SOURCE: DEALOGICcorporatefinancemag.com March 2004 cf 12

MOVINGONMover of the month: John Cavanaugh, Goodyear‘New’ assistant treasurerpost for CavanaughWhen CF spoke <strong>to</strong> JohnCavanaugh in February, itwas surprised <strong>to</strong> learn thattwo weeks in<strong>to</strong> his newlycreatedrole of assistanttreasurer for Goodyear TireCompany, he didn’t have anoffice or a phone.Cavanaugh, 33, a formerUS marine, joined Goodyearin July 2003 as direc<strong>to</strong>r offinancial strategy beforebeing promoted <strong>to</strong> assistanttreasurer by Goodyear’streasurer Darren Wells, whorecognised there was a needfor a skilled andexperienced assistanttreasurer <strong>to</strong> assist with thethe restructuring.The past two years havebeen difficult for the tyrecompany. It has lost $1.3billion in revenue and facedconsiderable difficultycutting costs because ofprotracted trade union talksin the US. Things picked upin April 2003, when a threeyear$1 billion cost-cuttingdeal was agreed on with theunions and there wasfurther good news inSeptember when it achievedthe partial restructuring ofits corporate debt with thereplacement of a largelyunsecured portion of $2.94billion in financing with$3.3 billion in secured creditlines. Reports of accountingerrors, uncovered inOc<strong>to</strong>ber worth $84.7 millionsince 1998, and an SECinvestigation, set it back.“The move <strong>to</strong> assistanttreasurer is at the forefron<strong>to</strong>f Goodyear’s refinancingplans,” says Cavanaugh.There was an assistanttreasurer at Goodyear 10years ago, but the positionwas deemed surplus <strong>to</strong>necessity as the company’sfortunes grew. “As thecompany ran in <strong>to</strong> problemsthe need <strong>to</strong> reorganise thetreasury <strong>to</strong> deal with thecomplexities it facedbecame more important.”So how does his role differ<strong>to</strong> that of direc<strong>to</strong>r offinancial strategy?More responsibility, saysCavanaugh. “As direc<strong>to</strong>r offinancial strategy, I wasresponsible for domesticand international financing,foreign currency, and <strong>to</strong>some degree corporatereporting. Now I managecash management and thebanking and rating agencyrelationships <strong>to</strong>o.” Not aneasy task. Goodyear’s plan<strong>to</strong> operate a $650 millioncredit line has promptedS&P <strong>to</strong> downgrade itsexisting bank loan andnotes from BB- <strong>to</strong> B+. Fitchalso downgradedGoodyear’s seniorunsecured rating <strong>to</strong> CCC+from B, affecting around $5billion worth of debt.“Obviously, coming fromKmart, which is aninvestment grade company,the finances at Goodyearwill be more of a challenge.In an investment gradecompany, there is much lessreliance on the banks <strong>to</strong>provide liquidity and cash.You can access the CPmarkets or put up an assetbackedreceivablesprogramme, for example. Ata sub-investment gradecompany you are reliant onthe banks for a liquidityfunding line <strong>to</strong> draw on.”Cavanaugh’s immediateconcern is <strong>to</strong> help turn thecompany round, a processthat will take some years, hesays, but that’s not <strong>to</strong> sayhe’s not looking ahead <strong>to</strong>Goodyear’s rejuvenation.“After we have stabilised thecompany, the next bigchallenge is <strong>to</strong> manage cashglobally. His<strong>to</strong>rically,Goodyear has beendecentralised but we plan <strong>to</strong>put a system in place whichwill allow us <strong>to</strong> move cashacross borders more easilyand that provides capitalwhen it is needed. Wewould also like <strong>to</strong> be able <strong>to</strong>manage the costs ofmanaging the cash.”The ‘we’ here isCavanaugh and DarrenWells, Goodyear’s treasurerand a past colleague ofCavanaugh’s. The pairworked <strong>to</strong>gether at Visteon -the principal supplier ofparts <strong>to</strong> Ford and fromwhere both joinedGoodyear. Wells joinedGoodyear in the summer of2002 as vice-president andtreasurer and obviouslyrates Cavanaugh’sexperience enough <strong>to</strong> bringhim on board.“I have worked withtalented people, and I verymuch enjoyed working forDarren. When he left wekept in <strong>to</strong>uch. The move <strong>to</strong>“The finances at Goodyearwill be a challenge. In aninvestment grade companythere is much less relianceon the banks <strong>to</strong> provideliquidity and cash.”Goodyear was an obviousone. I was the direc<strong>to</strong>r ofcapital markets at Visteon,and so was familiar with therefinancing procedurebefore I joined,” explainsCavanaugh. “As such, I wasable <strong>to</strong> come in <strong>to</strong> thecompany and help rightaway.” RPAT 33, CAVANAUGH ISCLIMBING QUICKLYJohn Cavanaugh spent fiveyears in the US Marine Corps,before opting for a careerchange. “Smartening up,” hecalls it. An MBA stimulatedhis interest in finance and aCFA qualification followedbefore a position at Kmart. “Ienjoy the financial engineeringaspect <strong>to</strong> treasury, I enjoy therelationships you develop withlenders and optimizing thecapital structure of thecompany.”»Feb 2004: appointedassistant treasurer atGoodyear»2003 – Jan 2004:direc<strong>to</strong>r of financial strategy atGoodyear»2000 – 2003: direc<strong>to</strong>r ofcapital markets at Visteon»1998 – 2000: involved infinancial analysis and treasuryat Kmart14 cf March 2004 corporatefinancemag.com

Crudele strikes a chordwith Gibson GuitarsRock stars can be quitehard <strong>to</strong> find in the world ofcorporate finance,although we did once speak<strong>to</strong> the accountant for PinkFloyd. And CF isn’t <strong>about</strong> <strong>to</strong>deliver a rock profile but ithas found a strong link <strong>to</strong>the world of pop withAnthony Crudele, therecently appointed CFO ofGibson Guitar.CF: So what’s it like <strong>to</strong> be afinance man in theentertainment industry?AC: Although we are anentertainment company,our core business unitcentres on themanufacturing of frettedinstruments.CF: But manufacturing Gibsonguitars is surely more sexy thantraditional manufacturing,isn’t it?AC: Technology is a greatchange agent and our CEO,[Henry Juszkiewicz], hasutilized technology <strong>to</strong>improve our businessprocesses in manufacturingas well as <strong>to</strong> bring thepower of the Gibson brand<strong>to</strong> bear in other areas andparts of the world. In justthe last few years, we haveexpanded the Gibson namein<strong>to</strong> web based retail,bricks and mortar retail,artist showcases and mostrecently in digital audio.CF: You bring 25 yearsexperience <strong>to</strong> Gibson. How willyou use it?AC: By working in thetrenches [Crudele wascontroller at SportsAuthority before beingappointed <strong>to</strong> CFO] you gaina thorough understandingof the critical nature ofcontrols and how abreakdown can have acrippling effect. It alsoprovides a more disciplinedand organized approach <strong>to</strong>project management andday-<strong>to</strong>-day administration.This allows you <strong>to</strong>understand your businessand grow it. As you gainexperience, then you canlead. The glitz – IPO, M&A,debt deals – is greatexperience, but it’sworking with the opera<strong>to</strong>rsthat is the foundation s<strong>to</strong>neof a strong CFO.CF: So how will you spend theearly months at Gibson?AC: In my first year I willbe focusing on harnessingthe full power of oursystems <strong>to</strong> providefinancial information forreal-time decision making. Ialso want <strong>to</strong> provideleadership <strong>to</strong> the financearea so that it is perceivedas a value add partner. Weare a decentralisedorganisation and I believethat we can highlightefficiencies throughout theorganisation and enhanceproductivity.Our sec<strong>to</strong>r hasconsistently had steadygrowth; but at Gibson wewant <strong>to</strong> be a leader. We areconstantly looking atadvancements and have <strong>to</strong>be selective in how weallocate our resources. Wehave made a significantinvestment in two areas –developing the technologyfor a digital guitar anddeveloping an extremelyuser friendly digitaljukebox. Making sure weare properly capitalizedand have the appropriatebusiness partners <strong>to</strong> movethese ventures forwardwas/is a priority.CF: What does ‘properlycapitalized’ mean?AC: We have alwaysleveraged our growth andhave continued <strong>to</strong> do so. Werecently completed arefinancing with twopremier partners – FleetCapital and Blacks<strong>to</strong>nePartners. We look at ourbankers as businesspartners. I consult withthem on business issues andtheir varied backgroundsprovide a strong experiencebase which is invaluable.Blacks<strong>to</strong>ne’s equity anddebt groups are premierWall Street professionalsand have access <strong>to</strong> resourcesthat otherwise may not beaccessible.CF: Do the scandals at publiccorporations affect the world ofprivate corporations?AC: A lot has been said<strong>about</strong> accountingmisappropriations and SECscrutiny, but as a privatecompany, we are focusedon growing a business.CF: And do private inves<strong>to</strong>rsdiffer from their publiccounterparts?“As you gain experience,then you can lead. The glitzof an IPO, M&A and debtdeals is great, but it’sworking with the opera<strong>to</strong>rsthat is the foundation s<strong>to</strong>neof a strong CFO.”AC: We have limitedoutside inves<strong>to</strong>rs, butreacting <strong>to</strong> our board ofdirec<strong>to</strong>rs and lenders isquite similar <strong>to</strong> dealing withoutside inves<strong>to</strong>rs. Questionswill vary from generalquestions <strong>about</strong> thebusiness <strong>to</strong> deep probinginterrogations whichrequire extensive analysis.The most significantdifference between us and apublicly traded company isthe ability <strong>to</strong> shareinformation more openlywith our business partnersand inves<strong>to</strong>rs. In the publicarena, you must ensureequitable dissemination ofdata <strong>to</strong> all parties; andtherefore, you must beguarded in your commentsprior <strong>to</strong> a general pressrelease of the information.CF: So as the CFO of GibsonGuitars, can CF assume youplay the instrument yourself?AC: I enjoy all types ofmusic and would neverwant <strong>to</strong> do anything <strong>to</strong>harm the industry;therefore, I do not play anytype of instrument!Growing up, my brotherhad a Gibson and a GibsonAmplifier. So my musicalcareer ended on the bestequipment. RPcorporatefinancemag.com March 2004 cf 15

MOVINGONTechnophile CFO turns <strong>to</strong>TippingPointAdam Chibib, recentlyappointed CFO ofTippingPoint Technologies,a provider of intrusionprevention technology -network securitymanagement <strong>to</strong> the ITilliterate - has made asuccessful career for himselfin technology all withoutleaving Austin, Texas, hishome<strong>to</strong>wn since age 10.Following a degree inbusiness administrationfrom the University of Texasat Austin, Chibib started hiscareer in accountancyworking for FranklinFederal Bancorp. But eventhen he had an inclination<strong>to</strong>wards technology and wasresponsible for thecompany’s successfulconversion <strong>to</strong> newaccounting software.“Public accountancy wasa great starting point for mycareer,” says Chibib. “Ittaught me how <strong>to</strong>effectively solve differenttypes of problems, atdifferent companies, indifferent industries. Fromthese collective experiencesI was able <strong>to</strong> learn the bestway <strong>to</strong> build operationalinfrastructure.”After stints at Coopers &Lybrand and PriceWaterhouse where he wasTechnology Industry groupmanager, Chibib made thejump <strong>to</strong> software companyTivoli Systems. He wascontroller and responsiblefor the worldwideaccounting functions of themulti-billion dollarcompany.“What attracted me <strong>to</strong>technology companies wasthe chance <strong>to</strong> apply thetechniques I had learned inpublic accountancy <strong>to</strong> thetechnology start-upenvironment. Technologycompanies provided mewith the opportunity <strong>to</strong>build <strong>something</strong> from theground up and have theresponsibility for thesuccess or failure of thecompanies that I work for.”That entrepreneurialspirit was given full reinwhen Chibib co-foundedbroadband softwareprovider BroadJump in1998. There he shaped thecompany by creating andimplementing the businessmodel, product licensingstrategies and all internalpolicies and procedures.Under his guidance, thecompany maintainedsequential quarter afterquarter revenue growth,from its first revenuequarter in late 1999, andwas profitable for the lastthree quarters of 2002 – twoquarters ahead of schedule.BroadJump earned revenuesof $50 million in 2002 – a137% increase over 2001 – invery challenging economictimes.Those kind of resultsearned Chibib the 2002Ernst & Young Entrepreneurof the Year Award andhelped BroadJump achievemention in Deloitte &Touche’s “50 FastestGrowing Companies” list in2001. They also made itpossible for Chibib and histeam <strong>to</strong> sell the company inNovember 2002 <strong>to</strong> MotiveCommunications, in a s<strong>to</strong>ckfor s<strong>to</strong>ck transaction.Not one <strong>to</strong> take themoney and run, Chibib <strong>to</strong>okover as CFO at WaveSetTechnologies in May 2003.Seven months later WaveSetmerged with SunMicrosystems and he movedon again. So why the move<strong>to</strong> TippingPoint which is,after all, a listed companyand not a start-up? It comesdown <strong>to</strong> his entrepreneurialpersonality, says Chibib.“The entrepreneurialspirit is alive and well atTippingPoint,” says Chibib.“The company is in agrowth phase so the keyfundamentals of my rolehave not really changed. Iam still focused onshareholder value, accurateand timely internal andexternal financial reporting,compliance with applicablelaws and smart growth. Theopportunity at TippingPointis as exciting andchallenging as any start-upthat I have worked for.”Chibib has spent most ofhis first four weeks atTippingPoint looking at thecompany’s internal controls– “making sure that we areable <strong>to</strong> grow the companyefficiently and effectively[by] having the right team inplace, operational readiness,streamlined businessprocesses and the right levelof infrastructure.”Looking ahead, Chibibsays that his financial goalfor the company is <strong>to</strong> create“What attracted me <strong>to</strong>technology companies wasthe chance <strong>to</strong> apply thetechniques I learned inpublic accountancy <strong>to</strong> atechnology start-up.”shareholder value. He says:“Because we are an earlystage revenue company,shareholder value will mostlikely be created through<strong>to</strong>p-line revenue growth anddriving the company <strong>to</strong>profitability. Our focus willbe creating the rightbalance of investments <strong>to</strong>accomplish this.”But can TippingPointever achieve the amazinggrowth that BroadJump did?“The extraordinary growthat BroadJump was certainlyatypical for the economicclimate at that time.[However] I do see severalsimilarities betweenBroadJump andTippingPoint that, coupledwith an improvingeconomy, may provideTippingPoint with growthopportunities.“TippingPoint has done atremendous job of definingthe intrusion preventionmarket and creating aworld-class product inUnityOne. [And] I think tha<strong>to</strong>ur sec<strong>to</strong>r will see bothvalidation and growth in2004. Corporations willbegin allocating budgetdollars <strong>to</strong> intrusionprevention solutions and wewill benefit from thematuration of our market,”says Chibib. MW16 cf March 2004 corporatefinancemag.com

ProxyMed recruitshealthcare veteranStarting a new job in themiddle of a merger isprobably every CFO’snightmare, but for GregoryEisenhauer, newlyappointed CFO of ProxyMed,the electronic healthcaretransaction servicescompany, its all real.Denied the luxury of ahoneymoon period, he hasspent his first two months atProxyMed dealing with anaudit, and figuring out how<strong>to</strong> manage Sarbanes-Oxley.“It’s a lot <strong>to</strong> get up <strong>to</strong>speed on and the wholecompany is in a state ofchange. Anytime you movein<strong>to</strong> a new field there is awhole new language <strong>to</strong> learnbut I must say that everyoneis very excited <strong>about</strong> theopportunities this mergerwill bring, and they havereally helped my transitiongo quite smoothly.”In brief»The New York S<strong>to</strong>ckExchange board ofdirec<strong>to</strong>rs has appointedAmy Butte as executivevice president with plansfor her <strong>to</strong> succeed KeithHelsby as CFO when heretires in April. Mostrecently Butte was chiefstrategist and CFO of CreditSuisse First Bos<strong>to</strong>n’sfinancial-services division.»Uniform providerAngelica Corporation’s CFOTheodore Armstrong hasretired after 18 years withthe company. JamesThe merger is withPlanVista Solutions, anotherhealthcare claims serviceprovider. The twocompanies signed a threeyearjoint marketingagreement in June 2003, aprelude <strong>to</strong> merging, butcomplemented each otherso well they decided <strong>to</strong>complete the merger early.Eisenhauer saw thebenefits of the mergerstraight away. “It is cheaperand more efficient <strong>to</strong>process claims electronicallyrather than manually. Butno one in the industry hasput this <strong>to</strong>gether before,selling certain aspects of ourservices <strong>to</strong> providers andother aspects <strong>to</strong> payers.With PlanVista we will havea unique footprint.“The merger allows us <strong>to</strong>expand the range of savings<strong>to</strong> medical costShaffer, who has been withAngelica for nearly fiveyears as vice president andtreasurer, will succeedArmstrong as CFO.»Generic drug makerAndrx has promoted formerfinance VP John Hanson <strong>to</strong>CFO. Former CFO AngeloMalahias has becomepresident.»United Technologies, aprovider of products andservices <strong>to</strong> the buildingsystems and aerospaceindustries, has appointedtwo vice presidents <strong>to</strong>assume the responsibilitiesof CFO Stephen Page whenmanagement solutions.”The merger also putsboth companies at thecutting edge when dealingwith healthcare claims.“Healthcare lags behindother industries in usingtechnology <strong>to</strong> make itsprocesses more efficient. Butthe government willcontinue <strong>to</strong> apply pressure<strong>to</strong> the industry <strong>to</strong> increasethe au<strong>to</strong>mation <strong>to</strong> reducecosts and errors.”Prior <strong>to</strong> ProxyMed,Eisenhauer worked for moretraditional healthcarecompanies. He worked atRehabCare Group, aprovider of therapyprogramme managementand temporary healthcarestaffing, ultimatelybecoming its CFO inSeptember 2000. Eisenhauerwas with RehabCare foralmost 10 years and duringhe retires on April 14.James Geisler has beennamed vice president,finance and Gregory Hayeshas been named VP,accounting and control.»Discount retailer TJXCompanies has namedJeffrey Naylor, former CFOof Big Lots, CFO. FormerCFO Donald Campbellassumes the newly createdposition of executive vicepresident, chiefadministrative and businessdevelopment officer.»Mary Wins<strong>to</strong>n, mostrecently vice president andcontroller of Visteonhis tenure there, revenuesgrew from $40 million <strong>to</strong>over $500 million.Eisenhauer left in May 2002<strong>to</strong> became CFO for USHealthworks, a nationaloccupational healthcareservices company.Eisenhauer is ahealthcare veteran but likeall the best career choices, itwasn’t planned. His first jobwas with APEX Oil andSverdrup Corporation, aprovider of technologyengineering services. Hemoved <strong>to</strong> RehabCare whenhis boss at Sverdrup becameRehabCare’s CFO.Similarly, Eisenhauerknew ProxyMed CEO MikeHoover and Nancy Ham,president and COO, beforemoving there. He is content<strong>to</strong> stay. “Healthcare is agrowing field. [At ProxyMed]I liked the space, the growthopportunities and themanagement. It was theright time <strong>to</strong> join. I amfortunate <strong>to</strong> be joining acompany that representssuch an exceptional growthopportunity.” MWCorporation, has beennamed as CFO of ScholasticCorporation. KevinMcEnery, who held thisposition since l995,resigned <strong>to</strong> pursue newcareer opportunities.»Apple executive vicepresident and CFO FredAnderson will retire onJune 1 2004 and hand thereins over <strong>to</strong> senior vicepresident of finance andcorporate controller PeterOppenheimer. Andersonwill be appointed <strong>to</strong> theboard of direc<strong>to</strong>rs upon hisretirement. He currentlyserves on the board of eBayand E.piphany.corporatefinancemag.com March 2004 cf 17

CFOPROFILE“Financing €68 billiondebt was the easy bit.”In December 2002 France Telecom had €68 billion in debt andwas being bailed out by the French Government. A year laterdebt has reduced by a third and the company is successfullyplaying the capital markets. Tabitha Neville talks <strong>to</strong> MichelCombes, the modest finance chief at the centre of it all.ILLUSTRATION: RUSS TUDOR“2003 was a good year in terms of revenue growth. It was ayear in which France Telecom <strong>to</strong>ok control of its destiny again.“18 cf March 2004 corporatefinancemag.com

It is fair <strong>to</strong> say that France Telecomhas had a difficult couple of years.In fact, it is probably an understatementwhen you look closelyat how far the company hadfallen down the financial black holeand how far it has had <strong>to</strong> travel <strong>to</strong> ge<strong>to</strong>ut of it. There isn’t a better turnarounds<strong>to</strong>ry around.The teleocm company spent <strong>about</strong>€80 billion ($97.5 billion) in cash onexpansion between 1999 and 2000 (ithas 11.7 million cus<strong>to</strong>mers over fivecontinents) and racked up more than€100 billion debt. Plans <strong>to</strong> refinanceand reduce the company’s debt werenot implemented due <strong>to</strong> the marketturnaround and by April 2001 the company’sshare price had fallen 70% anddebt had ballooned <strong>to</strong> €60 billion (precedingthe fall, France Telecom’s (FT)shares had climbed 200% in less thansix months).In December 2002, the French governmentadvanced a €9 billion loan <strong>to</strong>help the company out of its deepeningfinancial crisis, and <strong>to</strong> prevent it missinga €15 billion debt repayment in2003. For 2002, FT reported a record fullyear loss of €20.7 billion.In February 2004, the companyreported revenues of €46.1 billion. Thecompany’s full-year net profit was €3.2billion a €23.9 billion turnaround from2002. Group debt amounted <strong>to</strong> €45 billionat the end of 2003 compared <strong>to</strong> €68billion a year earlier.CF caught up with Michel Combes,CFO of France Telecom, on the day thecompany issued a €2.5 billion threetranche deal in euros and sterling. Aftera year’s absence the company’s bondswere oversubscribed across all threematurities – the £500 million tranchewas three times oversubscribed and the€750 million eight-year tranche fourtimes – which enabled the company’sbookrunners DrKW, HSBC, JPMorgan,SG and Natexis <strong>to</strong> increase all threetranches. The banks were delightedwith the deal’s reception but Combesplays its success down.“Markets are generally good at thebeginning of the year, and the receptionour issuance received is areflection of this and of the scarcity ofcorporate bonds coming <strong>to</strong> market.”FT 2005:break downFrance Telecomlaunched FT 2005, inDecember 2002. It wasan initiative comprisingfour components:»TOP: a program <strong>to</strong>improve operationalperformance, whichwill generate more than€15 billion in free cashflow <strong>to</strong> reduce debt forthe period 2003-2005;»“15+15+15”: a plan <strong>to</strong>strengthen the group’sfinancial structure;»€15 billion via the TOPprogram;»€15 billion in freshequity, with theparticipation of theFrench State in itscapacity as shareholderThe €2.5 billion issue was atechnical refinancing move, and a liabilitymanagement exercise, saysCombes; a debt optimisation process.“The conditions of the three tranchesare better than the average cost of debtfor FT at the tme and it was not a questionof liquidity but a question ofreprofiling debt and rebalancingcurrencies. We had low reimbursementin 2007 and 2008 and no reimbursementin 2012, 2013 and 2014. The bondimproves this maturity profile. It wasan opportunistic move by us [FT is cashflow generative and positive and has noneed for funds] and allowed us <strong>to</strong> strikea better balance between our euro andsterling debt. Our sterling cash generationis rising and it seemed anappropriate time for increase insterling denominated debt.”More importantly, the success of thebond demonstrated the quality of FT’scredit and the financial markets’ voteof confidence in FT’s financial health. Itwas also further vindication of the company’smanagement, turnaround plansand execution. It is a long way from thepro rata <strong>to</strong> itsshareholding interest,i.e. for approximately €9billion;»€15 billion euros fromrefinancing debt;»A strategy focused oncus<strong>to</strong>mer satisfactionand integratedoperationalmanagement of aportfolio of assetscomprising businessesthat are leaders in theirprincipal markets, withstrong brands such asFrance Telecom,Orange, Wanadoo andEquant. Assets withweak strategic andfinancial positions orthose for whichmajority control is notpossible will beconsidered fordivestment. FranceTelecom will pursuestrategic partnerships inareas outside its coreactivities or those whereit cannot achieve criticalmass;»A completely newmanagement team ledby Thierry Bre<strong>to</strong>n,with asimplified organizationand greaterresponsibility assigned<strong>to</strong> managers.Just over a year later,the company hasreduced its on-balancesheetnet debt by €23.8billion <strong>to</strong> €44.2 billion.The TOP indica<strong>to</strong>r“Operating incomebefore depreciation andamortization lessCapex” increased by66.1% on a comparablebasis (63.4% on ahis<strong>to</strong>rical basis), <strong>to</strong>reach €12.2 billion atDecember 31, 2003.state of affairs in December 2002, whenFT struggled <strong>to</strong> raise financing in thecapital markets and avoid a liquiditycrisis. “We were facing such huge reimbursementamounts that the marketswere effectively closed <strong>to</strong> us.“What has been achieved in the last12 months is due <strong>to</strong> a dedicatedmanagement team with clear strategicgoals and strong execution skills,” saysCombes.On December 4 2002, the same daythe French government agreed its €9billion bailout of the company, ThierryBre<strong>to</strong>n, CEO, announced the initiativethat was <strong>to</strong> turn the company around.Called the FT2005, the initiativeincluded: TOP – a program <strong>to</strong> improveoperational performance and generatemore than €15 billion in free cash flow<strong>to</strong> reduce debt; and 15+15+15 – a plan<strong>to</strong> strengthen the group’s financialstructure through the TOP program,raising €15 billion in equity and €15billion from refinancing the company’sdebt (see box). The majority of savingsin 2003 concerned optimization ofinvestments and working capitalcorporatefinancemag.com March 2004 cf 19

CFOPROFILE“The rating in itself is not acommitment of themanagement team. Ourobjective is a netdebt/EBITDA ratio ofbetween 1.5 and two by theend of 2005.“requirements. Additional free cashflow would be generated from fixedlineactivities in France (40% <strong>to</strong> 45%) andby Orange (35% <strong>to</strong> 45%). Wanadoo willaccount for less than three per cent ofthe <strong>to</strong>tal.The company also aimed <strong>to</strong> achievegreater strategic and financialflexibility with the aim of a net debt/EBITDA ratio of between 1.5 and two bythe end of 2005.It was an ambitious plan, admitsCombes, but the market believed in itand, as a consequence, reopened <strong>to</strong> thecompany in December 2002.France Telecom wasted no time inacting upon the new initiative andaddressing its liquidity crisis. On 11December 2002, it issued a €2.5 billion,seven year eurobond. This was followedup in January 2003 with a €5.5 billionbond which covered the refinancing ofdebt maturing in 2003. In February, thecompany secured the signing of a newthree-year syndicated credit facility for€5 billion. It was a turning point for thecompany.“The liquidity crisis that was facingus at the end of 2002 was over by February2003.” In late February, FT’sshareholders approved plans for equityissuance of up <strong>to</strong> €30 billion and onMarch 24, the company launched itslong-awaited €15bn ($15.9bn) rightsissue, representing the third tranche ofits €45bn rescue plan. Some €9bn of theissue was taken up by Erap, a publicbody that holds the industrial stakes ofthe French state, which owns 54.5% ofFrance Telecom.In its Q1 2003 results, released inApril 2003, FT achieved an EBITDA marginof 36.2% (32% 2002) and EBITDA ne<strong>to</strong>f capital expenditure reached 27% ofsales compared <strong>to</strong> 15% in 2002. Almostimmediately, S&P raised its long andOrange &Wanadoobuy-outsFrance Telecom is one ofthe few telecomopera<strong>to</strong>rs with apresence in wireless(Orange), the internet(Wanadoo), fixed-lineservices and corporatesolutions. It hasmanaged this throughan aggressiveacquisition policy whichsurfaced late in 2003,when it bought outOrange shareholdersand in February when itput forward a proposal<strong>to</strong> do the same forWanadoo shareholders.In September 2003,FT agreed <strong>to</strong> pay €7.1billion in s<strong>to</strong>ck <strong>to</strong> buyoutminorityshareholders in Orange– just 30 months after itshort-term corporate credit rating on FT<strong>to</strong> BBB from BBB- and A-2 <strong>to</strong> A-3 ( S&P hasjust raised its long-term outlook <strong>to</strong>BBB+). Fitch swiftly followed. For a companythat saw its credit rating go fromthe <strong>to</strong>p <strong>to</strong> the bot<strong>to</strong>m of the investmentgrade scale between 1996 and 2002, thiswas a tremendous achievement.“The rating in itself is not a commitmen<strong>to</strong>f the management team,” saysCombe, who reemphasizes that the.company’s objective and commitmentvis a vis the financial markets is <strong>to</strong>reach a net debt/EBITDA ratio ofbetween 1.5 and two by the end of 2005.“This level of leverage will mean wehave the same leverage as a single Arated company. The rating therefore isonly a result of our commitment. Thespreads we got on our bond issue thisJanuary reflects the good assessment ofFT credit quality by the market.“It signals that the company is operatingas a normal company again andthat the market believes in FT andspun its mobilesubsidiary off.This move reflectedthe rapid return <strong>to</strong>health of FT and themove <strong>to</strong> reverse thedecentralised make-upof the company which,CEO Thierry Bre<strong>to</strong>nclaims, did not let thegroup take maximumadvantage of thepotential synergiesacross different businesslines.“Orange is core <strong>to</strong>FT’s strategy and that iswhy we decided <strong>to</strong>buyout Orange minorityshareholders and takeover full ownership ofthe company,” saysCombes.In February, FTlaunched a $4.9 billionoffer of cash and s<strong>to</strong>ckfor the remaining 29.4%of Wanadoo – itcurrently owns 71% ofthe company.Wanadoo has seen itsshares rise over 60% inthe last year andreported net income of€159 million in 2003, upfrom €30 million in2002 and it has longbeen expected that FTwould make moves <strong>to</strong>squeeze out theminority shareholders.The deal, <strong>to</strong> befollowed by a listing ofWanadoo’s Yellow Pagesdirec<strong>to</strong>ry business, willenable the French State<strong>to</strong> reduce its stake in FT<strong>to</strong> 50% from 54.5%. ( Alaw was passed inDecember 2003allowing the FrenchGovernment <strong>to</strong> decreaseits stake in FranceTelecom. It has yet <strong>to</strong>declare its intention <strong>to</strong>do so).The offer put forwardby the company valuesWanadoo at €13.25billion ($16.56 billion).believes in our future in telecoms. I amproud <strong>to</strong> be working for one of themain European players again.” cfCOMBES’S CAREER PATH»Michel Combes, 40, began his career atFrance Telecom in 1986 working onexternal networks and industrial andinternational affairs. In January 2003, hewas appointed CFO.»In February 2004, Combes steppeddown as non-executive direc<strong>to</strong>r ofEurotunnel citing an increased workload atFrance Telecom.»In 1991 he was appointed technicaladvisor <strong>to</strong> the Minister of Post,Telecommunications and Space, then <strong>to</strong> theMinister of Public Works, Transport andTourism. He returned <strong>to</strong> France Telecom inJune 1995.»Combes was executive vice president ofthe Nouvelles Frontières Group fromDecember 1999 <strong>to</strong> the end of 2001.20 cf March 2004 corporatefinancemag.com