NOTES TO AND FORMING PART OF THE UNCONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED DECEMBER 31, 201143.3Capital Adequacy RatioThe capital adequacy ratio, calculated in accordance with the SBP's guidelines on capital adequacy was as follows:2011 2010Regulatory capital base--------- (Rupees in '000) ---------Tier 1 Capital- Fully paid-up capital 12,241,798 12,241,798- Statutory reserves 15,996,864 14,446,898- Un-appropriated profit 33,534,116 26,250,489Total Tier 1 Capital 61,772,778 52,939,185Deductions:- Book value of intangibles 1,603,587 1,440,826- Shortfall in provisions irrespective of relaxation provided 756,000 261,637- Reciprocal cross holdings by banks 5,998 5,999- 50% of investments in equity and other regulatory capital of majority owned - -securities or other financial subsidiaries not consolidated in the statementof financial position 1,224,465 1,224,4653,590,050 2,932,927Total eligible Tier 1 Capital 58,182,728 50,006,258Supplementary CapitalTier 2 Capital- General provisions or general reserves for loan losses - upto a maximumof 1.25% of risk weighted assets 1,008,694 1,425,496- Revaluation reserves up to 45% 5,701,125 5,496,317- Foreign exchange translation reserves 8,912,150 7,370,891- Subordinated loans - upto a maximum of 50% of total eligible Tier 1 capital 6,783,480 7,852,176- Cash flow hedge reserve (95,377) (198,695)Total Tier 2 Capital 22,310,072 21,946,185Deductions:- 50 % of investments in equity and other regulatory capital of majority ownedsecurities or other financial subsidiaries not consolidated in the statementof financial position 1,224,465 1,224,465Total eligible Tier 2 Capital 21,085,607 20,721,720Total eligible Capital 79,268,335 70,727,978Risk weighted exposuresCapital requirementsRisk weighted assetsNote 2011 2010 2011 2010Credit risk--------------------------------- (Rupees in '000) ---------------------------------Claims on:Federal and Provincial Governments, SBPand other sovereigns – in foreign currency2,912,091 1,806,245 29,120,906 18,062,446Public Sector Enterprises 894,849 1,285,319 8,948,485 12,853,191<strong>Bank</strong>s 3,945,216 3,197,031 39,452,164 31,970,310Corporates 22,290,315 22,086,826 222,903,149 220,868,255Retail portfolio 2,586,963 3,428,589 25,869,631 34,285,894Secured by residential property 164,803 174,425 1,648,031 1,744,250Past due loans 1,874,084 1,944,316 18,740,841 19,443,160Listed equity investments 134,042 900,932 1,340,416 9,009,323Unlisted equity investments 2,588,180 83,307 25,881,796 833,073Investments in fixed assets 2,137,829 2,098,325 21,378,291 20,983,246Other assets 803,222 530,330 8,032,224 5,303,29940,331,594 37,535,645 403,315,934 375,356,447Market riskInterest rate risk 3,580,837 2,268,723 44,760,466 28,359,037Equity exposure risk 955,828 296,776 11,947,850 3,709,701Foreign exchange risk 627,128 40,273 7,839,103 503,4135,163,793 2,605,772 64,547,419 32,572,151Operational risk 6,992,693 6,356,450 87,408,658 79,455,62652,488,080 46,497,867 555,272,011 487,384,224Capital adequacy ratioTotal eligible regulatory capital held 79,268,335 70,727,978Total risk weighted assets 555,272,011 487,384,224Capital adequacy ratio 14.28% 14.51%42

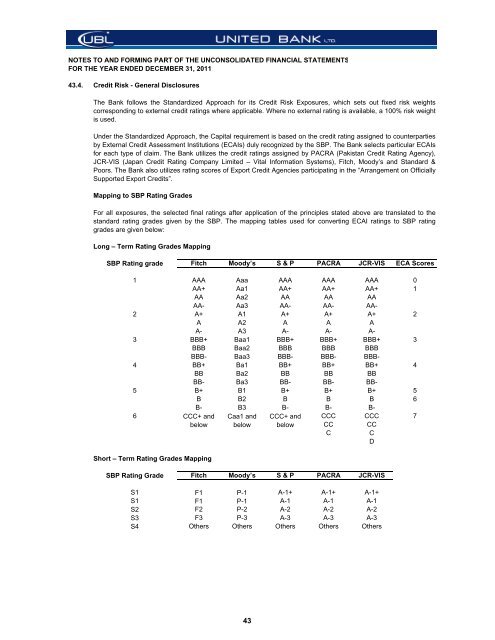

NOTES TO AND FORMING PART OF THE UNCONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED DECEMBER 31, 201143.4. Credit Risk - General DisclosuresThe <strong>Bank</strong> follows the Standardized Approach for its Credit Risk Exposures, which sets out fixed risk weightscorresponding to external credit ratings where applicable. Where no external rating is available, a 100% risk weightis used.Under the Standardized Approach, the Capital requirement is based on the credit rating assigned to counterpartiesby External Credit Assessment Institutions (ECAIs) duly recognized by the SBP. The <strong>Bank</strong> selects particular ECAIsfor each type of claim. The <strong>Bank</strong> utilizes the credit ratings assigned by PACRA (Pakistan Credit Rating Agency),JCR-VIS (Japan Credit Rating Company <strong>Limited</strong> – Vital Information Systems), Fitch, Moody’s and Standard &Poors. The <strong>Bank</strong> also utilizes rating scores of Export Credit Agencies participating in the “Arrangement on OfficiallySupported Export Credits”.Mapping to SBP Rating GradesFor all exposures, the selected final ratings after application of the principles stated above are translated to thestandard rating grades given by the SBP. The mapping tables used for converting ECAI ratings to SBP ratinggrades are given below:Long – Term Rating Grades MappingSBP Rating grade123456Fitch Moody’s S & P PACRA JCR-VIS ECA ScoresAAA Aaa AAA AAA AAA 0AA+ Aa1 AA+ AA+ AA+ 1AA Aa2 AA AA AAAA- Aa3 AA- AA- AA-A+ A1 A+ A+ A+ 2A A2 A A AA- A3 A- A- A-BBB+ Baa1 BBB+ BBB+ BBB+ 3BBB Baa2 BBB BBB BBBBBB- Baa3 BBB- BBB- BBB-BB+ Ba1 BB+ BB+ BB+ 4BB Ba2 BB BB BBBB- Ba3 BB- BB- BB-B+ B1 B+ B+ B+ 5B B2 B B B 6B- B3 B- B- B-CCC+ andbelowCaa1 andbelowCCC+ andbelowCCC CCC 7CCCCCCDShort – Term Rating Grades MappingSBP Rating GradeS1S1S2S3S4Fitch Moody’s S & P PACRA JCR-VISF1 P-1 A-1+ A-1+ A-1+F1 P-1 A-1 A-1 A-1F2 P-2 A-2 A-2 A-2F3 P-3 A-3 A-3 A-3Others Others Others Others Others43