M.A.R.C.: an Actuarial Model for Credit Risk - Proceedings ASTIN ...

M.A.R.C.: an Actuarial Model for Credit Risk - Proceedings ASTIN ...

M.A.R.C.: an Actuarial Model for Credit Risk - Proceedings ASTIN ...

SHOW LESS

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

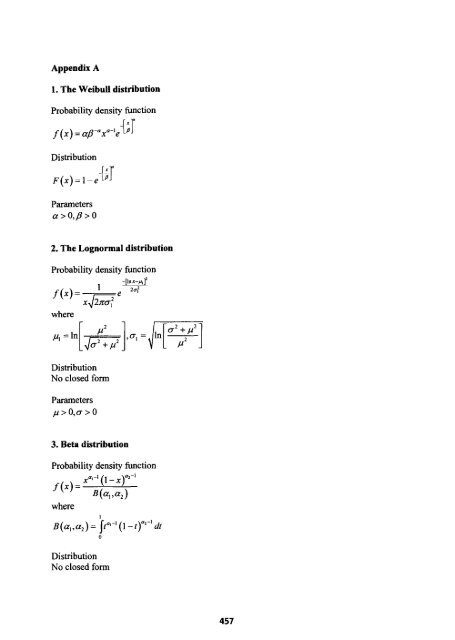

Appendix A1. The Weibull distributionProbability density hctionf(x)=a;O -n x a-l e -[;JDistribution~(x)= 1 - e -[STParametersa > 0,p > 02. The Lognormal distributionProbability density functionwhere-[lnx-wT1 -~~2u;DistributionNo closed <strong>for</strong>mParametersp > 0,cr > 03. Beta distributionProbability density functionDistributionNo closed <strong>for</strong>m457