M.A.R.C.: an Actuarial Model for Credit Risk - Proceedings ASTIN ...

M.A.R.C.: an Actuarial Model for Credit Risk - Proceedings ASTIN ...

M.A.R.C.: an Actuarial Model for Credit Risk - Proceedings ASTIN ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

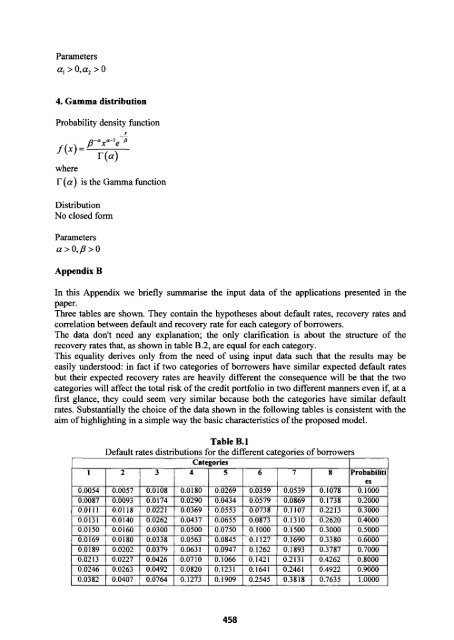

Parametersa, > O,a, > 04. Gamma distributionProbability density functionXwherer (a) is the Gamma functionDistributionNo closed <strong>for</strong>mParametersa > 0,p > 0Appendix BIn this Appendix we briefly summarise the input data of the applications presented in thepaper.Three tables are shown. They contain the hypotheses about default rates, recovery rates <strong>an</strong>dcorrelation between default <strong>an</strong>d recovery rate <strong>for</strong> each category of borrowers.The data don't need <strong>an</strong>y expl<strong>an</strong>ation; the only clarification is about the structure of therecovery rates that, as shown in table B.2, are equal <strong>for</strong> each category.This equality derives only from the need of using input data such that the results may beeasily understood: in fact if two categories of borrowers have similar expected default ratesbut their expected recovery rates are heavily different the consequence will be that the twocategories will affect the total risk of the credit portfolio in two different m<strong>an</strong>ners even if, at afirst gl<strong>an</strong>ce, they could seem very similar because both the categories have similar defaultrates. Subst<strong>an</strong>tially the choice of the data shown in the following tables is consistent with theaim of highlighting in a simple way the basic characteristics of the proposed model.Table B.lDefault rates distributions <strong>for</strong> the different categories of borrowers0.0246 I 0.0263 1 0.0492 1 0.0820 I 0.1231 1 0.1641 I 02461 I 0.4922 I 0.9000.0382 I 0.0407 1 0.0764 I 0.1273 I 0.1909 1 0.2545 I 0.3818 I 0.7635 I 1.0000458