The 2005 Aga Khan Agency for Microfinance Annual Report

The 2005 Aga Khan Agency for Microfinance Annual Report

The 2005 Aga Khan Agency for Microfinance Annual Report

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

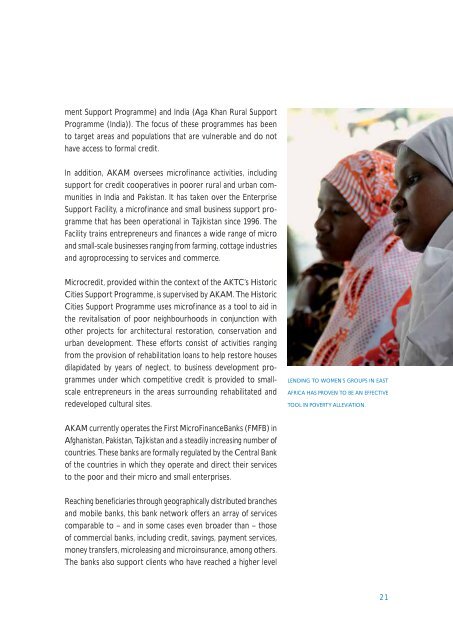

ment Support Programme) and India (<strong>Aga</strong> <strong>Khan</strong> Rural SupportProgramme (India)). <strong>The</strong> focus of these programmes has beento target areas and populations that are vulnerable and do nothave access to <strong>for</strong>mal credit.In addition, AKAM oversees microfinance activities, includingsupport <strong>for</strong> credit cooperatives in poorer rural and urban communitiesin India and Pakistan. It has taken over the EnterpriseSupport Facility, a microfinance and small business support programmethat has been operational in Tajikistan since 1996. <strong>The</strong>Facility trains entrepreneurs and finances a wide range of microand small-scale businesses ranging from farming, cottage industriesand agroprocessing to services and commerce.Microcredit, provided within the context of the AKTC’s HistoricCities Support Programme, is supervised by AKAM. <strong>The</strong> HistoricCities Support Programme uses microfinance as a tool to aid inthe revitalisation of poor neighbourhoods in conjunction withother projects <strong>for</strong> architectural restoration, conservation andurban development. <strong>The</strong>se ef<strong>for</strong>ts consist of activities rangingfrom the provision of rehabilitation loans to help restore housesdilapidated by years of neglect, to business development programmesunder which competitive credit is provided to smallscaleentrepreneurs in the areas surrounding rehabilitated andredeveloped cultural sites.LENDING TO WOMEN’S GROUPS IN EASTAFRICA HAS PROVEN TO BE AN EFFECTIVETOOL IN POVERTY ALLEVIATION.AKAM currently operates the First MicroFinanceBanks (FMFB) inAfghanistan, Pakistan, Tajikistan and a steadily increasing number ofcountries. <strong>The</strong>se banks are <strong>for</strong>mally regulated by the Central Bankof the countries in which they operate and direct their servicesto the poor and their micro and small enterprises.Reaching beneficiaries through geographically distributed branchesand mobile banks, this bank network offers an array of servicescomparable to – and in some cases even broader than – thoseof commercial banks, including credit, savings, payment services,money transfers, microleasing and microinsurance, among others.<strong>The</strong> banks also support clients who have reached a higher level21