<strong>The</strong> Growing CompanyInsuranceConversationStartersHelp your advisors helpyou by asking them . . .■ Do I need to expandcoverages as mybusiness grows? Howcan I best prioritizecoverages?■ How about acomprehensive riskmanagement program?■ Do I need to considerKey Person Insurance,Employment PracticesLiability Insurance andDirectors & OfficersLiability Insurance?Protecting Key EmployeesOnly one-quarterof companies withfewer than 100employees have keyperson insurance.Source: <strong>The</strong> <strong>Hartford</strong><strong>Business</strong> Owners Survey,October 2006Prioritize and expandyour coverages.As your company grows, youshould have more resources todevote to insurance – and youmay find that you need additionalcoverages to protect your businessagainst the increased risk thatoften comes with growth.Whether your growth has takenthe form of investment inexpensive equipment or thehiring of key staff people, youneed to understand the value ofyour expansion and plan to protectit. And be sure you know whatcoverages your clients, investorsor creditors require. Some mightinsist on higher limits than youmight choose on your own.As you add employees, it becomesincreasingly important to haveemployment practices liabilityinsurance, which can help protectyour business from certainemployment-related claims; andkey person insurance, which canhelp protect against a significantloss resulting from the death ordisability of a key employee. Ifyou have investors, customers,suppliers or others with a significantfinancial stake in the successof your company, you may wantto consider directors and officersliability insurance, which canhelp protect the company and itsleadership against allegations ofbreach of fiduciary duty in themanagement of the company.Devise a comprehensiverisk management program.Managing risk is about morethan just having the rightcoverages, although that’s whereit starts. You need to be sure youknow where your risks lie andwhat steps you can take—beyondinsurance—to limit them. You canhelp your insurance agent thinkabout risk in a holistic fashionand build a plan to address it. Atypical risk management programhas many aspects, such asemployment screening, proactiveloss control, comprehensive safetyand ergonomic training, a formalreturn-to-work program forinjured employees (with light-dutyjobs pre-determined), specialequipment (such as a state-ofthe-artfire suppression system),business contingency planningand, increasingly, technology andinformation protection. To theextent that other professionalexpertise is required to implementYour AnnualInsuranceCheckupIt’s wise to sit down withan insurance professionalfor a yearly review of yourpicture. Make sure youreview all of your coverages –even if some were purchasedthrough another professionalor carrier. Also prepare anoverview of changes thatoccurred in your businessover the previous year –fluctuations in revenue,increases or reductions ininventory, new or upgradedreal estate or facilities,physical plant and equipmentor office equipment, fleetchanges and additions tostaff. Add an up-to-dateinventory of your assets—real estate, physical plant,inventory, office equipmentand furnishings andstaff. <strong>The</strong>n your insuranceagent will have a full pictureof your business that willhelp you get the protectionyou need.Insurance asCredit ProtectionOwning the proper type ofinsurance can accomplishother goals, such asprotecting your credit ratingwhen earnings are impairedand funding deferred compensationarrangements.With certain coverages, if anemergency strikes, you haveaccess to your policy’s cashvalues through loans andwithdrawals; the cash valueof the policy is a companyasset. Speak to aninsurance professionalabout the details.your program, your insuranceadvisor can help you arrangefor these services. And don’tforget to ask him or her aboutcredits that might be available fora comprehensive risk managementprogram in a business like yours.Ensure that your businesscan carry on in the event ofdisaster.Be it from the wrath of MotherNature or man-made threats, youneed to protect your company’sphysical and intellectual assets.Work with an IT professionalto ensure that you have securestorage of important records andsufficient backup of sensitivecompany data. Proper planningcan get your company back onits feet in short time.20

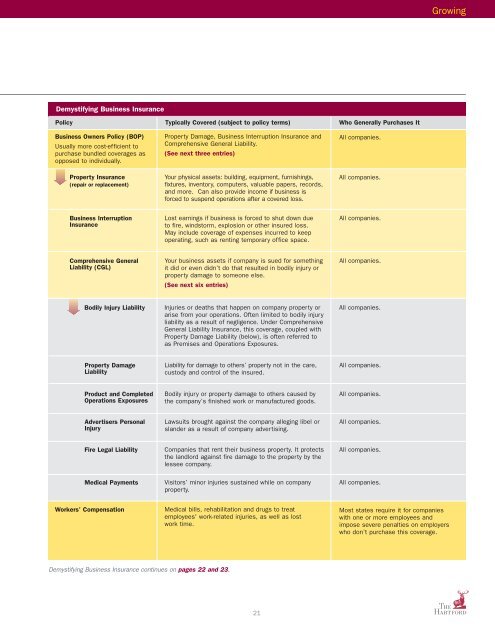

GrowingDemystifying <strong>Business</strong> InsurancePolicy Typically Covered (subject to policy terms) Who Generally Purchases It<strong>Business</strong> Owners Policy (BOP)Usually more cost-efficient topurchase bundled coverages asopposed to individually.Property Insurance(repair or replacement)Property Damage, <strong>Business</strong> Interruption Insurance andComprehensive General Liability.(See next three entries)Your physical assets: building, equipment, furnishings,fixtures, inventory, computers, valuable papers, records,and more. Can also provide income if business isforced to suspend operations after a covered loss.All companies.All companies.<strong>Business</strong> InterruptionInsuranceLost earnings if business is forced to shut down dueto fire, windstorm, explosion or other insured loss.May include coverage of expenses incurred to keepoperating, such as renting temporary office space.All companies.Comprehensive GeneralLiability (CGL)Your business assets if company is sued for somethingit did or even didn’t do that resulted in bodily injury orproperty damage to someone else.(See next six entries)All companies.Bodily Injury LiabilityInjuries or deaths that happen on company property orarise from your operations. Often limited to bodily injuryliability as a result of negligence. Under ComprehensiveGeneral Liability Insurance, this coverage, coupled withProperty Damage Liability (below), is often referred toas Premises and Operations Exposures.All companies.Property DamageLiabilityLiability for damage to others’ property not in the care,custody and control of the insured.All companies.Product and CompletedOperations ExposuresBodily injury or property damage to others caused bythe company’s finished work or manufactured goods.All companies.Advertisers PersonalInjuryLawsuits brought against the company alleging libel orslander as a result of company advertising.All companies.Fire Legal LiabilityCompanies that rent their business property. It protectsthe landlord against fire damage to the property by thelessee company.All companies.Medical PaymentsVisitors’ minor injuries sustained while on companyproperty.All companies.Workers’ CompensationMedical bills, rehabilitation and drugs to treatemployees' work-related injuries, as well as lostwork time.Most states require it for companieswith one or more employees andimpose severe penalties on employerswho don’t purchase this coverage.Demystifying <strong>Business</strong> Insurance continues on pages 22 and 23.21