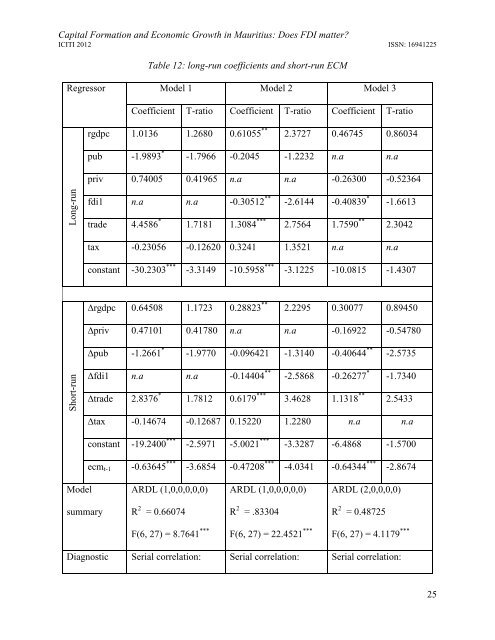

Short-runLong-run<strong>Capital</strong> <strong>Formation</strong> <strong>and</strong> <strong>Economic</strong> <strong>Growth</strong> <strong>in</strong> <strong>Mauritius</strong>: Does FDI matter?ICITI 2012 ISSN: 16941225Table 12: long-run coefficients <strong>and</strong> short-run ECMRegressor Model 1 Model 2 Model 3Coefficient T-ratio Coefficient T-ratio Coefficient T-ratiorgdpc 1.0136 1.2680 0.61055 ** 2.3727 0.46745 0.86034pub -1.9893 * -1.7966 -0.2045 -1.2232 n.a n.apriv 0.74005 0.41965 n.a n.a -0.26300 -0.52364fdi1 n.a n.a -0.30512 ** -2.6144 -0.40839 * -1.6613trade 4.4586 * 1.7181 1.3084 *** 2.7564 1.7590 ** 2.3042tax -0.23056 -0.12620 0.3241 1.3521 n.a n.aconstant -30.2303 *** -3.3149 -10.5958 *** -3.1225 -10.0815 -1.4307∆rgdpc 0.64508 1.1723 0.28823 ** 2.2295 0.30077 0.89450∆priv 0.47101 0.41780 n.a n.a -0.16922 -0.54780∆pub -1.2661 * -1.9770 -0.096421 -1.3140 -0.40644 ** -2.5735∆fdi1 n.a n.a -0.14404 ** -2.5868 -0.26277 * -1.7340∆trade 2.8376 * 1.7812 0.6179 *** 3.4628 1.1318 ** 2.5433∆tax -0.14674 -0.12687 0.15220 1.2280 n.a n.aconstant -19.2400 *** -2.5971 -5.0021 *** -3.3287 -6.4868 -1.5700ecm t-1 -0.63645 *** -3.6854 -0.47208 *** -4.0341 -0.64344 *** -2.8674ModelsummaryARDL (1,0,0,0,0,0)R 2 = 0.66074F(6, 27) = 8.7641 *** ARDL (1,0,0,0,0,0)R 2 = .83304F(6, 27) = 22.4521 *** ARDL (2,0,0,0,0)R 2 = 0.48725F(6, 27) = 4.1179 ***Diagnostic Serial correlation: Serial correlation: Serial correlation:25

<strong>Capital</strong> <strong>Formation</strong> <strong>and</strong> <strong>Economic</strong> <strong>Growth</strong> <strong>in</strong> <strong>Mauritius</strong>: Does FDI matter?ICITI 2012 ISSN: 16941225tests F(1, 26) = 0.82833Functional Form:F(1, 26) = 0.0054376F(1, 26) = 0.010141Functional Form:F(1, 26) = 1.1261F(1, 26) = .081478Functional Form:F(1, 26) = 6.3159 **Note: * 10%, ** 5%, *** 1% <strong>and</strong> n.a not applicableLong-run positive accelerator effects are established for all three measures of capital formation,whereby a percentage <strong>in</strong>crease <strong>in</strong> real average <strong>in</strong>come contributes to the respective <strong>in</strong>crease <strong>in</strong>FDI, private <strong>and</strong> public <strong>in</strong>vestment by 1.0136, 0.61055 <strong>and</strong> 0.46745 percents. And, short-runaccelerator effects st<strong>and</strong> at 0.64508, 0.28823, <strong>and</strong> 0.30077, respectively. However, significantaccelerator effects are only established for private capital formation, whereas for foreign <strong>and</strong>public capital formation the accelerator effects are weak both <strong>in</strong> size <strong>and</strong> significance.Analys<strong>in</strong>g the impact of FDI on domestic fixed capital formation, vice-versa. First, crowd<strong>in</strong>g-outeffects are reported from FDI to private capital formation, where short- <strong>and</strong> long-run impactsst<strong>and</strong> at -0.14404 <strong>and</strong> -0.30512, respectively. From private <strong>in</strong>vestment to FDI, although evidenceof crowd<strong>in</strong>g-<strong>in</strong> is detected, the results are statistically weak or <strong>in</strong>significant. Second, two-waycrowd<strong>in</strong>g-out is established between public <strong>in</strong>vestment <strong>and</strong> FDI. From FDI to public <strong>in</strong>vestmentthe elasticity coefficient is significantly negative at around -0.41 for both short- <strong>and</strong> long-run.And, the impact of public <strong>in</strong>vestment on FDI is significantly negative <strong>and</strong> more important -1.2661 (short-run) <strong>and</strong> -1.9893 (long-run).The nexus between domestic private <strong>and</strong> public capital formation for <strong>Mauritius</strong> conforms to thecrowd<strong>in</strong>g-out hypothesis. The results yield a two-way crowd<strong>in</strong>g out between the two variables ofaround -0.2, however, the coefficients are not statistically significant. Thus, weak crowd<strong>in</strong>g-outis established between private <strong>and</strong> public capital formation, vice-versa.26