Commentary on the Results continuedfor the period ended 31 December 2011Commercial and Residential property, which includes the wholly owned Leighton Properties and a 50.28% stake in listedproperty developer Devine Limited, recorded a segment profit of $1 million for the transitional financial year to 31 December2011 (loss of $93 million for tshe twelve month period to 30 June 2011). This was achieved on segment revenue of $528million. Leighton Properties recorded a number of successes during the period achieving some significant sales including HQNorth Tower in Brisbane. The Leighton Properties / Devine joint venture Hamilton Harbour development in Brisbane wascompleted in November and is almost sold out. Both sales have helped in the recycling of the Group’s capital. Commercial andResidential’s work in hand fell slightly to $1.3 billion at 31 December 2011, compared to $1.7 billion at 30 June 2011.The Leighton Group has maintained a strong balance sheet which remains a strategic priority. This is essential for the Group tocontinue to support its global operations through the funding of bonds and guarantees, provision of working capital, andmaking investments in plant and equipment. At 31 December 2011 the Group’s capital structure was sound with shareholder’sequity of $2.8 billion, total assets of $9.9 billion, and net debt of $641 million. Off balance sheet operating leases totalled $668million.Cash at the end of the transitional financial year remained high at $1.5 billion, boosted by $452 million from the sale of HWEMining’s iron ore business. Cash generated from operating activities of $328 million was lower than a normal period due topayment of the cost overruns on Airport Link and Victorian Desalination Plant projects. Primary uses of cash during the periodwere loan repayments totalling $200 million, shareholder loans to HLG of $122 million, and plant and equipment purchases of$502 million. In addition, $219 million of cash pledged as security against bank loans secured by HLG was reclassified asnon‐current receivables during the period.Gross debt, including recourse and non‐recourse loans, stood at $2.1 billion at 31 December 2011. The Group’s debt maturityprofile remains relatively long term despite $670 million of loans and other facilities falling due within the next twelve months.Plant and equipment purchases for the 6 month period to 31 December 2011 totalled $502 million, including $179 million formajor component parts. Although the sale of the HWE Mining iron ore business in the Pilbara resulted in a reduction ofproperty, plant and equipment on the balance sheet by $229 million, other contract mining operations continue to require thepurchase of new plant and equipment to undertake new and existing projects.Depreciation of plant and equipment was $505 million, including $235 million for major component parts. The Group’s plantfleet is now worth a combined $3.1 billion comprising $1.9 billion of owned plant and equipment, $0.5 billion under financeleases and $0.7 billion under operating leases.Gearing, expressed as net debt plus operating leases to net debt plus operating leases plus shareholder equity, reduced overthe period from 35% at 30 June 2011 to 32% at 31 December 2011. This was due to the receipt of cash from the sale of theHWE Mining iron ore businesses and good cash flow management.Bonds and guarantees at 31 December 2011 totalled $3.6 billion, in line with the Group’s high levels of construction work. Inaddition to this amount, $308 million was undrawn.During the 6 months to 31 December 2011, a total of 572,000 options were exercised, bringing the total number of ordinaryshares on issue to 337,087,596.The earnings per share for the 6 month period of 101 cents compares to earnings per share of negative (133.1) cents for thetwelve month period to 30 June 2011. An unfranked final dividend of 60 cents per share was announced by the Directors forthe transitional financial year to 31 December 2011. This compares with 60 cents per share fully franked for the 12 monthperiod ended 30 June 2011.Leighton Holdings LimitedAppendix 4E and Consolidated <strong>Preliminary</strong> <strong>Final</strong> <strong>Report</strong> for the Period Ended 31 December 2011 4

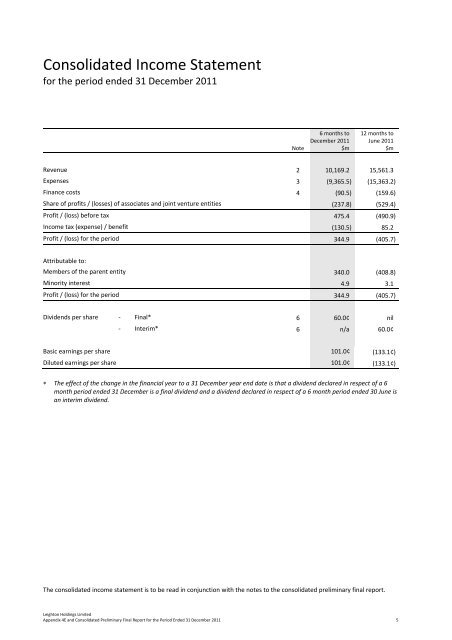

Consolidated Income Statementfor the period ended 31 December 2011Note6 months toDecember 2011$m12 months toJune 2011$mRevenue 2 10,169.2 15,561.3Expenses 3 (9,365.5) (15,363.2)Finance costs 4 (90.5) (159.6)Share of profits / (losses) of associates and joint venture entities (237.8) (529.4)Profit / (loss) before tax 475.4 (490.9)Income tax (expense) / benefit (130.5) 85.2Profit / (loss) for the period 344.9 (405.7)Attributable to:Members of the parent entity 340.0 (408.8)Minority interest 4.9 3.1Profit / (loss) for the period 344.9 (405.7)Dividends per share ‐ <strong>Final</strong>* 6 60.0¢ nil‐ Interim* 6 n/a 60.0¢Basic earnings per share 101.0¢ (133.1¢)Diluted earnings per share 101.0¢ (133.1¢)∗ The effect of the change in the financial year to a 31 December year end date is that a dividend declared in respect of a 6month period ended 31 December is a final dividend and a dividend declared in respect of a 6 month period ended 30 June isan interim dividend.The consolidated income statement is to be read in conjunction with the notes to the consolidated preliminary final report.Leighton Holdings LimitedAppendix 4E and Consolidated <strong>Preliminary</strong> <strong>Final</strong> <strong>Report</strong> for the Period Ended 31 December 2011 5