Oversigt og vejledning til revisorer og ... - Erhvervsstyrelsen

Oversigt og vejledning til revisorer og ... - Erhvervsstyrelsen

Oversigt og vejledning til revisorer og ... - Erhvervsstyrelsen

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

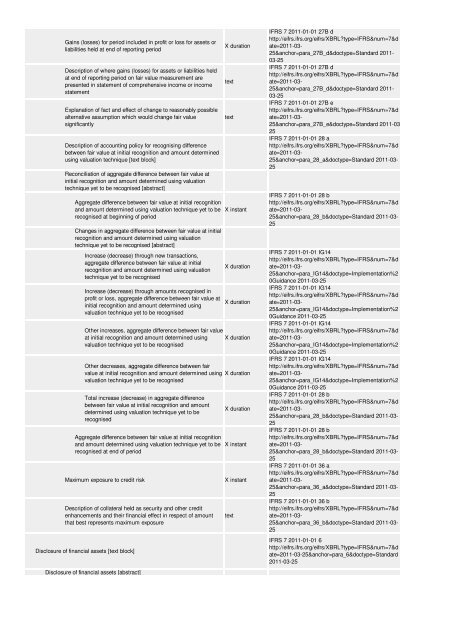

Gains (losses) for period included in profit or loss for assets orliabilities held at end of reporting periodDescription of where gains (losses) for assets or liabilities heldat end of reporting period on fair value measurement arepresented in statement of comprehensive income or incomestatementExplanation of fact and effect of change to reasonably possiblealternative assumption which would change fair valuesignificantlyDescription of accounting policy for rec<strong>og</strong>nising differencebetween fair value at initial rec<strong>og</strong>nition and amount determinedusing valuation technique [text block]Reconciliation of aggregate difference between fair value atinitial rec<strong>og</strong>nition and amount determined using valuationtechnique yet to be rec<strong>og</strong>nised [abstract]Aggregate difference between fair value at initial rec<strong>og</strong>nitionand amount determined using valuation technique yet to berec<strong>og</strong>nised at beginning of periodChanges in aggregate difference between fair value at initialrec<strong>og</strong>nition and amount determined using valuationtechnique yet to be rec<strong>og</strong>nised [abstract]Increase (decrease) through new transactions,aggregate difference between fair value at initialrec<strong>og</strong>nition and amount determined using valuationtechnique yet to be rec<strong>og</strong>nisedIncrease (decrease) through amounts rec<strong>og</strong>nised inprofit or loss, aggregate difference between fair value atinitial rec<strong>og</strong>nition and amount determined usingvaluation technique yet to be rec<strong>og</strong>nisedX durationtexttextX instantX durationX durationOther increases, aggregate difference between fair valueat initial rec<strong>og</strong>nition and amount determined using X durationvaluation technique yet to be rec<strong>og</strong>nisedOther decreases, aggregate difference between fairvalue at initial rec<strong>og</strong>nition and amount determined using X durationvaluation technique yet to be rec<strong>og</strong>nisedTotal increase (decrease) in aggregate differencebetween fair value at initial rec<strong>og</strong>nition and amountdetermined using valuation technique yet to berec<strong>og</strong>nisedAggregate difference between fair value at initial rec<strong>og</strong>nitionand amount determined using valuation technique yet to berec<strong>og</strong>nised at end of periodMaximum exposure to credit riskDescription of collateral held as security and other creditenhancements and their financial effect in respect of amountthat best represents maximum exposureDisclosure of financial assets [text block]Disclosure of financial assets [abstract]X durationX instantX instanttextIFRS 7 2011-01-01 27B dhttp://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_27B_d&doctype=Standard 2011-03-25IFRS 7 2011-01-01 27B dhttp://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_27B_d&doctype=Standard 2011-03-25IFRS 7 2011-01-01 27B ehttp://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_27B_e&doctype=Standard 2011-03-25IFRS 7 2011-01-01 28 ahttp://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_28_a&doctype=Standard 2011-03-25IFRS 7 2011-01-01 28 bhttp://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_28_b&doctype=Standard 2011-03-25IFRS 7 2011-01-01 IG14http://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_IG14&doctype=Implementation%20Guidance 2011-03-25IFRS 7 2011-01-01 IG14http://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_IG14&doctype=Implementation%20Guidance 2011-03-25IFRS 7 2011-01-01 IG14http://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_IG14&doctype=Implementation%20Guidance 2011-03-25IFRS 7 2011-01-01 IG14http://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_IG14&doctype=Implementation%20Guidance 2011-03-25IFRS 7 2011-01-01 28 bhttp://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_28_b&doctype=Standard 2011-03-25IFRS 7 2011-01-01 28 bhttp://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_28_b&doctype=Standard 2011-03-25IFRS 7 2011-01-01 36 ahttp://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_36_a&doctype=Standard 2011-03-25IFRS 7 2011-01-01 36 bhttp://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_36_b&doctype=Standard 2011-03-25IFRS 7 2011-01-01 6http://eifrs.ifrs.org/eifrs/XBRL?type=IFRS&num=7&date=2011-03-25&anchor=para_6&doctype=Standard2011-03-25