Auditor independence and non-audit services - ICAEW

Auditor independence and non-audit services - ICAEW

Auditor independence and non-audit services - ICAEW

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

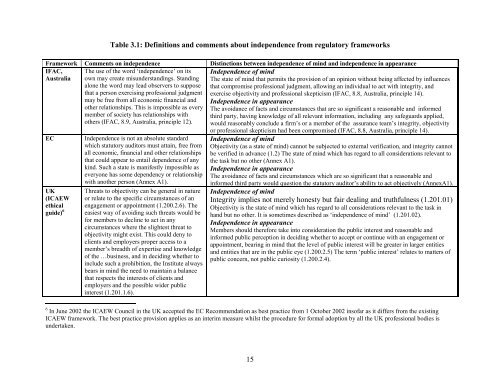

Table 3.1: Definitions <strong>and</strong> comments about <strong>independence</strong> from regulatory frameworksFramework Comments on <strong>independence</strong> Distinctions between <strong>independence</strong> of mind <strong>and</strong> <strong>independence</strong> in appearanceIFAC,AustraliaECUK(<strong>ICAEW</strong>ethicalguide) 6The use of the word ‘<strong>independence</strong>’ on itsown may create misunderst<strong>and</strong>ings. St<strong>and</strong>ingalone the word may lead observers to supposethat a person exercising professional judgmentmay be free from all economic financial <strong>and</strong>other relationships. This is impossible as everymember of society has relationships withothers (IFAC, 8.9, Australia, principle 12).Independence is not an absolute st<strong>and</strong>ardwhich statutory <strong>audit</strong>ors must attain, free fromall economic, financial <strong>and</strong> other relationshipsthat could appear to entail dependence of anykind. Such a state is manifestly impossible aseveryone has some dependency or relationshipwith another person (Annex A1).Threats to objectivity can be general in natureor relate to the specific circumstances of anengagement or appointment (1.200.2.6). Theeasiest way of avoiding such threats would befor members to decline to act in anycircumstances where the slightest threat toobjectivity might exist. This could deny toclients <strong>and</strong> employers proper access to amember’s breadth of expertise <strong>and</strong> knowledgeof the …business, <strong>and</strong> in deciding whether toinclude such a prohibition, the Institute alwaysbears in mind the need to maintain a balancethat respects the interests of clients <strong>and</strong>employers <strong>and</strong> the possible wider publicinterest (1.201.1.6).Independence of mindThe state of mind that permits the provision of an opinion without being affected by influencesthat compromise professional judgment, allowing an individual to act with integrity, <strong>and</strong>exercise objectivity <strong>and</strong> professional skepticism (IFAC, 8.8, Australia, principle 14).Independence in appearanceThe avoidance of facts <strong>and</strong> circumstances that are so significant a reasonable <strong>and</strong> informedthird party, having knowledge of all relevant information, including any safeguards applied,would reasonably conclude a firm’s or a member of the assurance team’s integrity, objectivityor professional skepticism had been compromised (IFAC, 8.8, Australia, principle 14).Independence of mindObjectivity (as a state of mind) cannot be subjected to external verification, <strong>and</strong> integrity cannotbe verified in advance (1.2) The state of mind which has regard to all considerations relevant tothe task but no other (Annex A1).Independence in appearanceThe avoidance of facts <strong>and</strong> circumstances which are so significant that a reasonable <strong>and</strong>informed third party would question the statutory <strong>audit</strong>or’s ability to act objectively (AnnexA1).Independence of mindIntegrity implies not merely honesty but fair dealing <strong>and</strong> truthfulness (1.201.01)Objectivity is the state of mind which has regard to all considerations relevant to the task inh<strong>and</strong> but no other. It is sometimes described as ‘<strong>independence</strong> of mind’ (1.201.02).Independence in appearanceMembers should therefore take into consideration the public interest <strong>and</strong> reasonable <strong>and</strong>informed public perception in deciding whether to accept or continue with an engagement orappointment, bearing in mind that the level of public interest will be greater in larger entities<strong>and</strong> entities that are in the public eye (1.200.2.5) The term ‘public interest’ relates to matters ofpublic concern, not public curiosity (1.200.2.4).6 In June 2002 the <strong>ICAEW</strong> Council in the UK accepted the EC Recommendation as best practice from 1 October 2002 insofar as it differs from the existing<strong>ICAEW</strong> framework. The best practice provision applies as an interim measure whilst the procedure for formal adoption by all the UK professional bodies isundertaken.15