Optmization of Treasury

This book is dedicated to companies and students that wish to know about how to optimize treasury and Cash-Management.

This book is dedicated to companies and students that wish to know about how to optimize treasury and Cash-Management.

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

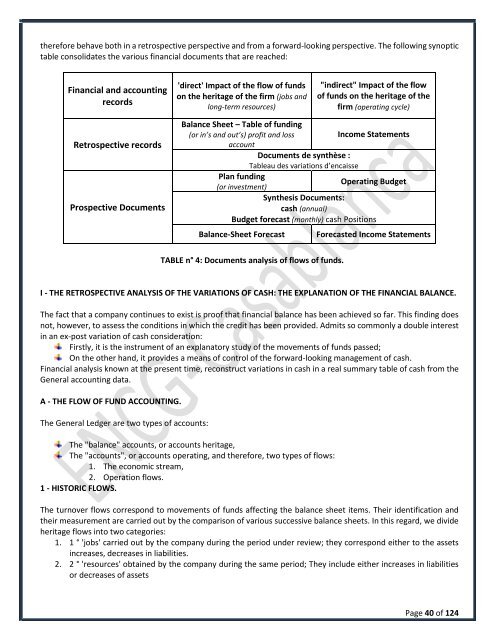

therefore behave both in a retrospective perspective and from a forward-looking perspective. The following synoptic<br />

table consolidates the various financial documents that are reached:<br />

Financial and accounting<br />

records<br />

'direct' Impact <strong>of</strong> the flow <strong>of</strong> funds<br />

on the heritage <strong>of</strong> the firm (jobs and<br />

long-term resources)<br />

"indirect" Impact <strong>of</strong> the flow<br />

<strong>of</strong> funds on the heritage <strong>of</strong> the<br />

firm (operating cycle)<br />

Retrospective records<br />

Prospective Documents<br />

Balance Sheet – Table <strong>of</strong> funding<br />

(or in’s and out’s) pr<strong>of</strong>it and loss<br />

Income Statements<br />

account<br />

Documents de synthèse :<br />

Tableau des variations d’encaisse<br />

Plan funding<br />

Operating Budget<br />

(or investment)<br />

Synthesis Documents:<br />

cash (annual)<br />

Budget forecast (monthly) cash Positions<br />

Balance-Sheet Forecast<br />

Forecasted Income Statements<br />

TABLE n° 4: Documents analysis <strong>of</strong> flows <strong>of</strong> funds.<br />

I - THE RETROSPECTIVE ANALYSIS OF THE VARIATIONS OF CASH: THE EXPLANATION OF THE FINANCIAL BALANCE.<br />

The fact that a company continues to exist is pro<strong>of</strong> that financial balance has been achieved so far. This finding does<br />

not, however, to assess the conditions in which the credit has been provided. Admits so commonly a double interest<br />

in an ex-post variation <strong>of</strong> cash consideration:<br />

Firstly, it is the instrument <strong>of</strong> an explanatory study <strong>of</strong> the movements <strong>of</strong> funds passed;<br />

On the other hand, it provides a means <strong>of</strong> control <strong>of</strong> the forward-looking management <strong>of</strong> cash.<br />

Financial analysis known at the present time, reconstruct variations in cash in a real summary table <strong>of</strong> cash from the<br />

General accounting data.<br />

A - THE FLOW OF FUND ACCOUNTING.<br />

The General Ledger are two types <strong>of</strong> accounts:<br />

The "balance" accounts, or accounts heritage,<br />

The "accounts", or accounts operating, and therefore, two types <strong>of</strong> flows:<br />

1. The economic stream,<br />

2. Operation flows.<br />

1 - HISTORIC FLOWS.<br />

The turnover flows correspond to movements <strong>of</strong> funds affecting the balance sheet items. Their identification and<br />

their measurement are carried out by the comparison <strong>of</strong> various successive balance sheets. In this regard, we divide<br />

heritage flows into two categories:<br />

1. 1 ° 'jobs' carried out by the company during the period under review; they correspond either to the assets<br />

increases, decreases in liabilities.<br />

2. 2 ° 'resources' obtained by the company during the same period; They include either increases in liabilities<br />

or decreases <strong>of</strong> assets<br />

Page 40 <strong>of</strong> 124