Audit Report (Q1 2016)

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Oman National Engineering & Investment Co. (SAOG)<br />

Internal <strong>Audit</strong> <strong>Report</strong> (1 st Quarter, <strong>2016</strong>)<br />

Apr-<strong>2016</strong><br />

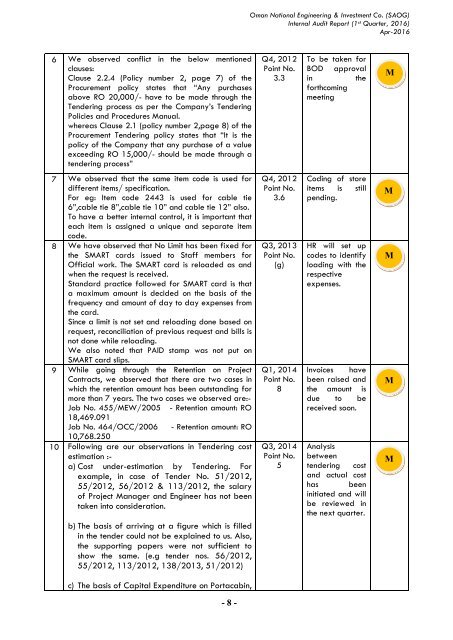

6 We observed conflict in the below mentioned<br />

clauses:<br />

Clause 2.2.4 (Policy number 2, page 7) of the<br />

Procurement policy states that “Any purchases<br />

above RO 20,000/- have to be made through the<br />

Tendering process as per the Company’s Tendering<br />

Policies and Procedures Manual.<br />

whereas Clause 2.1 (policy number 2,page 8) of the<br />

Procurement Tendering policy states that “It is the<br />

policy of the Company that any purchase of a value<br />

exceeding RO 15,000/- should be made through a<br />

tendering process”<br />

Q4, 2012<br />

Point No.<br />

3.3<br />

To be taken for<br />

BOD approval<br />

in the<br />

forthcoming<br />

meeting<br />

M<br />

7 We observed that the same item code is used for<br />

different items/ specification.<br />

For eg: Item code 2443 is used for cable tie<br />

6”,cable tie 8”,cable tie 10” and cable tie 12” also.<br />

To have a better internal control, it is important that<br />

each item is assigned a unique and separate item<br />

code.<br />

8 We have observed that No Limit has been fixed for<br />

the SMART cards issued to Staff members for<br />

Official work. The SMART card is reloaded as and<br />

when the request is received.<br />

Standard practice followed for SMART card is that<br />

a maximum amount is decided on the basis of the<br />

frequency and amount of day to day expenses from<br />

the card.<br />

Since a limit is not set and reloading done based on<br />

request, reconciliation of previous request and bills is<br />

not done while reloading.<br />

We also noted that PAID stamp was not put on<br />

SMART card slips.<br />

9 While going through the Retention on Project<br />

Contracts, we observed that there are two cases in<br />

which the retention amount has been outstanding for<br />

more than 7 years. The two cases we observed are:-<br />

Job No. 455/MEW/2005 - Retention amount: RO<br />

18,469.091<br />

Job No. 464/OCC/2006 - Retention amount: RO<br />

10,768.250<br />

10 Following are our observations in Tendering cost<br />

estimation :-<br />

a) Cost under-estimation by Tendering. For<br />

example, in case of Tender No. 51/2012,<br />

55/2012, 56/2012 & 113/2012, the salary<br />

of Project Manager and Engineer has not been<br />

taken into consideration.<br />

b) The basis of arriving at a figure which is filled<br />

in the tender could not be explained to us. Also,<br />

the supporting papers were not sufficient to<br />

show the same. (e.g tender nos. 56/2012,<br />

55/2012, 113/2012, 138/2013, 51/2012)<br />

Q4, 2012<br />

Point No.<br />

3.6<br />

Q3, 2013<br />

Point No.<br />

(g)<br />

<strong>Q1</strong>, 2014<br />

Point No.<br />

8<br />

Q3, 2014<br />

Point No.<br />

5<br />

Coding of store<br />

items is still<br />

pending.<br />

HR will set up<br />

codes to identify<br />

loading with the<br />

respective<br />

expenses.<br />

Invoices have<br />

been raised and<br />

the amount is<br />

due to be<br />

received soon.<br />

Analysis<br />

between<br />

tendering cost<br />

and actual cost<br />

has been<br />

initiated and will<br />

be reviewed in<br />

the next quarter.<br />

M<br />

M<br />

M<br />

M<br />

c) The basis of Capital Expenditure on Portacabin,<br />

- 8 -