CMI Annual Report 2022

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

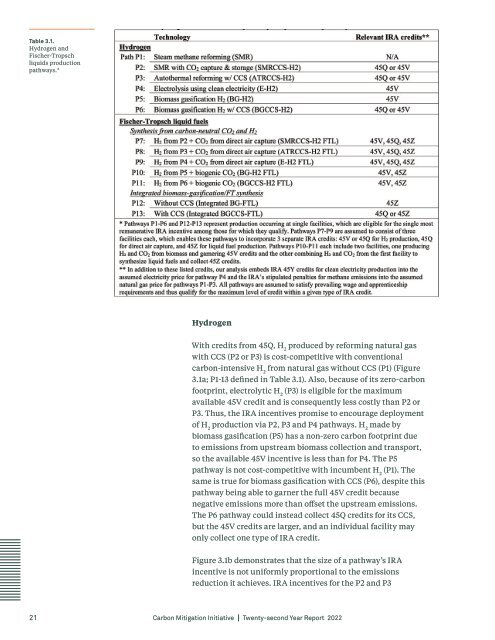

Table 3.1.<br />

Hydrogen and<br />

Fischer-Tropsch<br />

liquids production<br />

pathways.*<br />

Hydrogen<br />

With credits from 45Q, H 2<br />

produced by reforming natural gas<br />

with CCS (P2 or P3) is cost-competitive with conventional<br />

carbon-intensive H 2<br />

from natural gas without CCS (P1) (Figure<br />

3.1a; P1-13 defined in Table 3.1). Also, because of its zero-carbon<br />

footprint, electrolytic H 2<br />

(P3) is eligible for the maximum<br />

available 45V credit and is consequently less costly than P2 or<br />

P3. Thus, the IRA incentives promise to encourage deployment<br />

of H 2<br />

production via P2, P3 and P4 pathways. H 2<br />

made by<br />

biomass gasification (P5) has a non-zero carbon footprint due<br />

to emissions from upstream biomass collection and transport,<br />

so the available 45V incentive is less than for P4. The P5<br />

pathway is not cost-competitive with incumbent H 2<br />

(P1). The<br />

same is true for biomass gasification with CCS (P6), despite this<br />

pathway being able to garner the full 45V credit because<br />

negative emissions more than offset the upstream emissions.<br />

The P6 pathway could instead collect 45Q credits for its CCS,<br />

but the 45V credits are larger, and an individual facility may<br />

only collect one type of IRA credit.<br />

Figure 3.1b demonstrates that the size of a pathway’s IRA<br />

incentive is not uniformly proportional to the emissions<br />

reduction it achieves. IRA incentives for the P2 and P3<br />

21<br />

Carbon Mitigation Initiative Twenty-second Year <strong>Report</strong> <strong>2022</strong>