You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

The IPPF does not prescribe specific sequential steps an internal audi<strong>to</strong>r must follow when<br />

completing an engagement. The mechanics of such audits follow the usual processes<br />

related <strong>to</strong> planning, performing, and communication and in accordance with the relevant<br />

standards. As for all engagements, prior <strong>to</strong> planning a performance audit, a decision is made<br />

<strong>to</strong> include it in the audit plan, including the area of focus or <strong>to</strong>pic (although this is refined as<br />

part of the audit preparation when the scope and objectives are more fully developed).<br />

Inclusion of performance audits in the internal audit plan and consideration of <strong>to</strong>pics are<br />

covered in section 4B.1.<br />

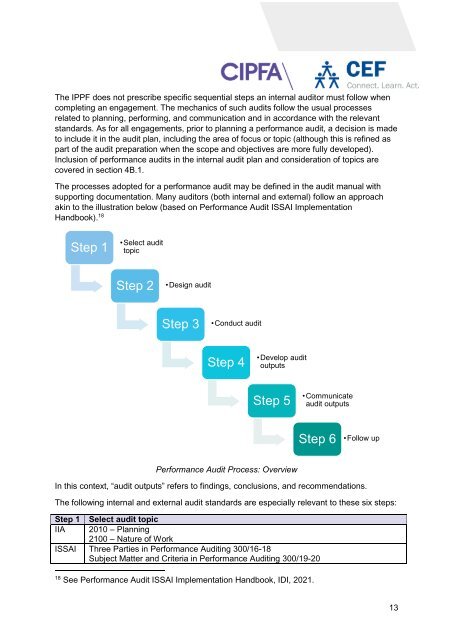

The processes adopted for a performance audit may be defined in the audit manual with<br />

supporting documentation. Many audi<strong>to</strong>rs (both internal and external) follow an approach<br />

akin <strong>to</strong> the illustration below (based on <strong>Performance</strong> <strong>Audit</strong> ISSAI Implementation<br />

Handbook). 18<br />

Step 1<br />

•Select audit<br />

<strong>to</strong>pic<br />

Step 2<br />

•Design audit<br />

Step 3<br />

•Conduct audit<br />

Step 4<br />

•Develop audit<br />

outputs<br />

Step 5<br />

•Communicate<br />

audit outputs<br />

Step 6<br />

•Follow up<br />

<strong>Performance</strong> <strong>Audit</strong> Process: Overview<br />

In this context, “audit outputs” refers <strong>to</strong> findings, conclusions, and recommendations.<br />

The following internal and external audit standards are especially relevant <strong>to</strong> these six steps:<br />

Step 1<br />

IIA<br />

Select audit <strong>to</strong>pic<br />

2010 – Planning<br />

2100 – Nature of Work<br />

ISSAI Three Parties in <strong>Performance</strong> <strong>Audit</strong>ing 300/16-18<br />

Subject Matter and Criteria in <strong>Performance</strong> <strong>Audit</strong>ing 300/19-20<br />

18<br />

See <strong>Performance</strong> <strong>Audit</strong> ISSAI Implementation Handbook, IDI, 2021.<br />

13