Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Choosing quality assurance steps that will ensure adherence with applicable auditing<br />

standards, including those for evidence <strong>to</strong> support audit findings. 33<br />

The supervisor also has an important role in determining the staff resources needed for the<br />

engagement <strong>to</strong> ensure the right capacity and quality of skills and expertise are available.<br />

The number, frequency, and nature of review meetings held by the supervisor with the<br />

audi<strong>to</strong>r or audi<strong>to</strong>rs should be decided based on need. Fac<strong>to</strong>rs would include the level of<br />

experience of the audi<strong>to</strong>r, the length and complexity of the audit, and personal preferences<br />

of both parties. Meetings should be structured by focusing on the audit plan, have a clear<br />

purpose, and result in agreed actions that are recorded and shared.<br />

Other Aspects of Quality Control<br />

Quality is essential for the integrity of the audit provider. As referenced above, the role of<br />

supervision plays a key role in quality assurance and is described by the IPPF as part of a<br />

comprehensive quality assurance and improvement program (QAIP). <strong>Audit</strong> policies and<br />

procedures should be designed <strong>to</strong> promote quality, conformance with the Standards, and<br />

continuous improvement. Regular internal and external review of the QAIP is needed <strong>to</strong><br />

ensure it is working. The head of the internal audit function is required <strong>to</strong> keep the governing<br />

body advised on matters relating <strong>to</strong> QAIP and conformance.<br />

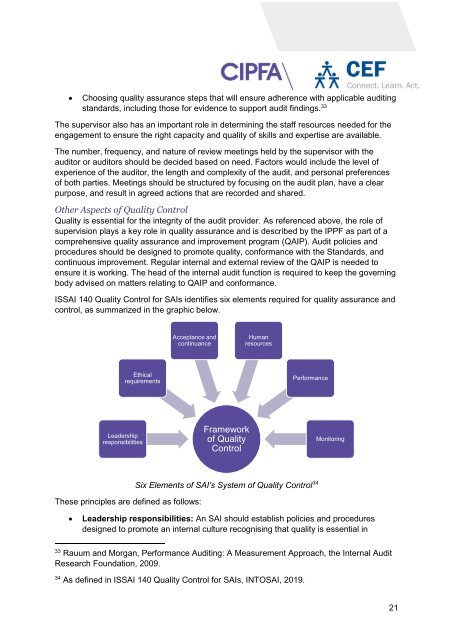

ISSAI 140 Quality Control for SAIs identifies six elements required for quality assurance and<br />

control, as summarized in the graphic below.<br />

Acceptance and<br />

continuance<br />

Human<br />

resources<br />

Ethical<br />

requirements<br />

<strong>Performance</strong><br />

Leadership<br />

responsibilities<br />

Framework<br />

of Quality<br />

Control<br />

Moni<strong>to</strong>ring<br />

These principles are defined as follows:<br />

Six Elements of SAI’s System of Quality Control 34<br />

<br />

Leadership responsibilities: An SAI should establish policies and procedures<br />

designed <strong>to</strong> promote an internal culture recognising that quality is essential in<br />

33<br />

Rauum and Morgan, <strong>Performance</strong> <strong>Audit</strong>ing: A Measurement Approach, the Internal <strong>Audit</strong><br />

Research Foundation, 2009.<br />

34<br />

As defined in ISSAI 140 Quality Control for SAIs, INTOSAI, 2019.<br />

21