Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

The first and third of these aspects are consistent with the focus and purpose of<br />

performance auditing. However, performance auditing considers a broad range of subject<br />

matter and can contribute <strong>to</strong> all aspects of the mission of internal auditing. For example:<br />

<br />

<br />

<br />

Operational information relates closely <strong>to</strong> efficiency and effectiveness.<br />

Safeguarding of assets has a strong link with the principle of economy.<br />

Compliance with laws, regulations, policies, and other authorities is often a key<br />

consideration in performance auditing.<br />

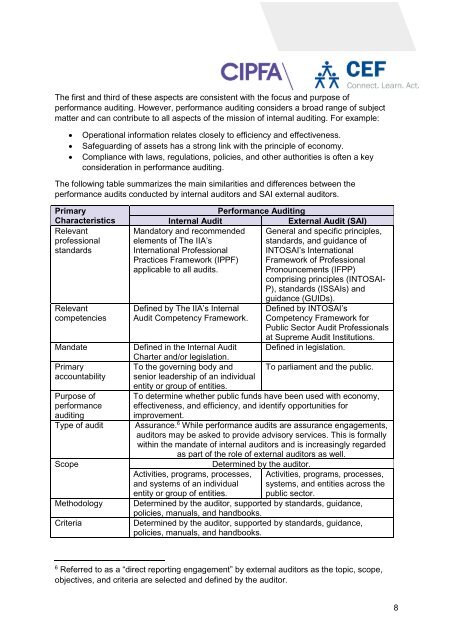

The following table summarizes the main similarities and differences between the<br />

performance audits conducted by internal audi<strong>to</strong>rs and SAI external audi<strong>to</strong>rs.<br />

Primary<br />

Characteristics<br />

Relevant<br />

professional<br />

standards<br />

Relevant<br />

competencies<br />

Mandate<br />

Primary<br />

accountability<br />

Purpose of<br />

performance<br />

auditing<br />

Type of audit<br />

Scope<br />

Methodology<br />

Criteria<br />

<strong>Performance</strong> <strong>Audit</strong>ing<br />

Internal <strong>Audit</strong><br />

External <strong>Audit</strong> (SAI)<br />

Manda<strong>to</strong>ry and recommended General and specific principles,<br />

elements of The IIA’s<br />

standards, and guidance of<br />

International Professional INTOSAI’s International<br />

Practices Framework (IPPF) Framework of Professional<br />

applicable <strong>to</strong> all audits.<br />

Pronouncements (IFPP)<br />

comprising principles (INTOSAI-<br />

P), standards (ISSAIs) and<br />

guidance (GUIDs).<br />

Defined by The IIA’s Internal<br />

<strong>Audit</strong> Competency Framework.<br />

Defined by INTOSAI’s<br />

Competency Framework for<br />

Public Sec<strong>to</strong>r <strong>Audit</strong> Professionals<br />

at Supreme <strong>Audit</strong> Institutions.<br />

Defined in the Internal <strong>Audit</strong> Defined in legislation.<br />

Charter and/or legislation.<br />

To the governing body and To parliament and the public.<br />

senior leadership of an individual<br />

entity or group of entities.<br />

To determine whether public funds have been used with economy,<br />

effectiveness, and efficiency, and identify opportunities for<br />

improvement.<br />

Assurance. 6 While performance audits are assurance engagements,<br />

audi<strong>to</strong>rs may be asked <strong>to</strong> provide advisory services. This is formally<br />

within the mandate of internal audi<strong>to</strong>rs and is increasingly regarded<br />

as part of the role of external audi<strong>to</strong>rs as well.<br />

Activities, programs, processes,<br />

and systems of an individual<br />

entity or group of entities.<br />

Determined by the audi<strong>to</strong>r.<br />

Activities, programs, processes,<br />

systems, and entities across the<br />

public sec<strong>to</strong>r.<br />

Determined by the audi<strong>to</strong>r, supported by standards, guidance,<br />

policies, manuals, and handbooks.<br />

Determined by the audi<strong>to</strong>r, supported by standards, guidance,<br />

policies, manuals, and handbooks.<br />

6<br />

Referred <strong>to</strong> as a “direct reporting engagement” by external audi<strong>to</strong>rs as the <strong>to</strong>pic, scope,<br />

objectives, and criteria are selected and defined by the audi<strong>to</strong>r.<br />

8