eastern district of wisconsin milwaukee county, employee

eastern district of wisconsin milwaukee county, employee

eastern district of wisconsin milwaukee county, employee

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

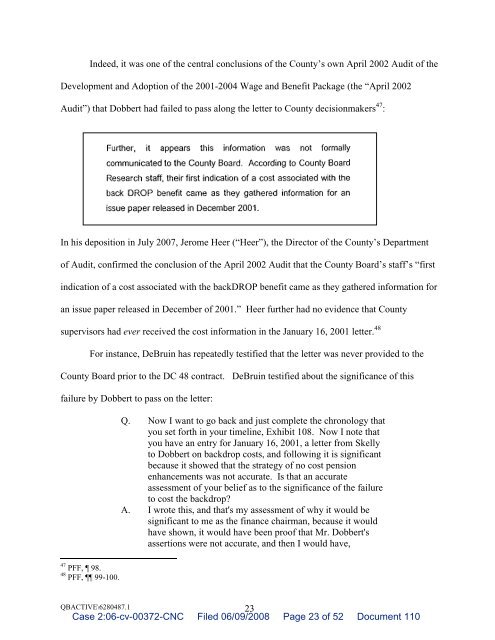

Indeed, it was one <strong>of</strong> the central conclusions <strong>of</strong> the County’s own April 2002 Audit <strong>of</strong> the<br />

Development and Adoption <strong>of</strong> the 2001-2004 Wage and Benefit Package (the “April 2002<br />

Audit”) that Dobbert had failed to pass along the letter to County decisionmakers 47 :<br />

In his deposition in July 2007, Jerome Heer (“Heer”), the Director <strong>of</strong> the County’s Department<br />

<strong>of</strong> Audit, confirmed the conclusion <strong>of</strong> the April 2002 Audit that the County Board’s staff’s “first<br />

indication <strong>of</strong> a cost associated with the backDROP benefit came as they gathered information for<br />

an issue paper released in December <strong>of</strong> 2001.” Heer further had no evidence that County<br />

supervisors had ever received the cost information in the January 16, 2001 letter. 48<br />

For instance, DeBruin has repeatedly testified that the letter was never provided to the<br />

County Board prior to the DC 48 contract. DeBruin testified about the significance <strong>of</strong> this<br />

failure by Dobbert to pass on the letter:<br />

47 PFF, 98.<br />

48 PFF, 99-100.<br />

Q. Now I want to go back and just complete the chronology that<br />

you set forth in your timeline, Exhibit 108. Now I note that<br />

you have an entry for January 16, 2001, a letter from Skelly<br />

to Dobbert on backdrop costs, and following it is significant<br />

because it showed that the strategy <strong>of</strong> no cost pension<br />

enhancements was not accurate. Is that an accurate<br />

assessment <strong>of</strong> your belief as to the significance <strong>of</strong> the failure<br />

to cost the backdrop?<br />

A. I wrote this, and that's my assessment <strong>of</strong> why it would be<br />

significant to me as the finance chairman, because it would<br />

have shown, it would have been pro<strong>of</strong> that Mr. Dobbert's<br />

assertions were not accurate, and then I would have,<br />

QBACTIVE\6280487.1 23<br />

Case 2:06-cv-00372-CNC Filed 06/09/2008 Page 23 <strong>of</strong> 52 Document 110