General information - Eureko Sigorta

General information - Eureko Sigorta

General information - Eureko Sigorta

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

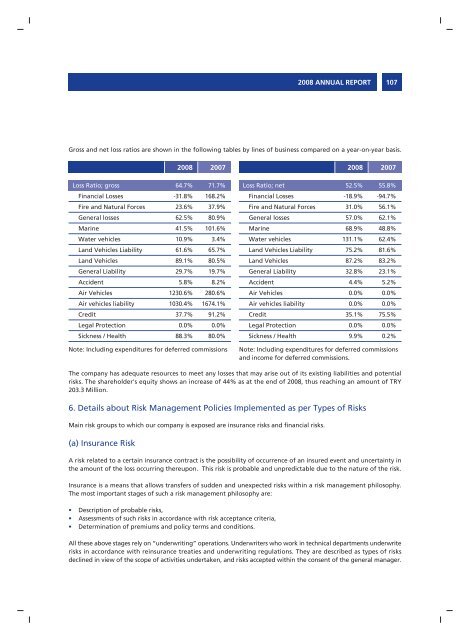

Gross and net loss ratios are shown in the following tables by lines of business compared on a year-on-year basis.<br />

Loss Ratio; gross<br />

Financial Losses<br />

Fire and Natural Forces<br />

<strong>General</strong> losses<br />

Marine<br />

Water vehicles<br />

Land Vehicles Liability<br />

Land Vehicles<br />

<strong>General</strong> Liability<br />

Accident<br />

Air Vehicles<br />

Air vehicles liability<br />

Credit<br />

Legal Protection<br />

Sickness / Health<br />

The company has adequate resources to meet any losses that may arise out of its existing liabilities and potential<br />

risks. The shareholder's equity shows an increase of 44% as at the end of 2008, thus reaching an amount of TRY<br />

203.3 Million.<br />

6. Details about Risk Management Policies Implemented as per Types of Risks<br />

Main risk groups to which our company is exposed are insurance risks and financial risks.<br />

(a) Insurance Risk<br />

2008 2007<br />

64.7%<br />

-31.8%<br />

23.6%<br />

62.5%<br />

41.5%<br />

10.9%<br />

61.6%<br />

89.1%<br />

29.7%<br />

5.8%<br />

1230.6%<br />

1030.4%<br />

37.7%<br />

0.0%<br />

88.3%<br />

71.7%<br />

168.2%<br />

37.9%<br />

80.9%<br />

101.6%<br />

3.4%<br />

65.7%<br />

80.5%<br />

19.7%<br />

8.2%<br />

280.6%<br />

1674.1%<br />

91.2%<br />

0.0%<br />

80.0%<br />

A risk related to a certain insurance contract is the possibility of occurrence of an insured event and uncertainty in<br />

the amount of the loss occurring thereupon. This risk is probable and unpredictable due to the nature of the risk.<br />

Insurance is a means that allows transfers of sudden and unexpected risks within a risk management philosophy.<br />

The most important stages of such a risk management philosophy are:<br />

• Description of probable risks,<br />

• Assessments of such risks in accordance with risk acceptance criteria,<br />

• Determination of premiums and policy terms and conditions.<br />

Loss Ratio; net<br />

Financial Losses<br />

Fire and Natural Forces<br />

<strong>General</strong> losses<br />

Marine<br />

Water vehicles<br />

Land Vehicles Liability<br />

Land Vehicles<br />

<strong>General</strong> Liability<br />

Accident<br />

Air Vehicles<br />

Air vehicles liability<br />

Credit<br />

Legal Protection<br />

Sickness / Health<br />

2008 ANNUAL REPORT<br />

2008 2007<br />

52.5%<br />

-18.9%<br />

31.0%<br />

57.0%<br />

68.9%<br />

131.1%<br />

75.2%<br />

87.2%<br />

32.8%<br />

4.4%<br />

0.0%<br />

0.0%<br />

35.1%<br />

0.0%<br />

9.9%<br />

55.8%<br />

-94.7%<br />

56.1%<br />

62.1%<br />

48.8%<br />

62.4%<br />

81.6%<br />

83.2%<br />

23.1%<br />

5.2%<br />

0.0%<br />

0.0%<br />

75.5%<br />

0.0%<br />

0.2%<br />

Note: Including expenditures for deferred commissions Note: Including expenditures for deferred commissions<br />

and income for deferred commissions.<br />

All these above stages rely on “underwriting” operations. Underwriters who work in technical departments underwrite<br />

risks in accordance with reinsurance treaties and underwriting regulations. They are described as types of risks<br />

declined in view of the scope of activities undertaken, and risks accepted within the consent of the general manager.<br />

107