The Evolving Air Transport Industry

The Evolving Air Transport Industry

The Evolving Air Transport Industry

- TAGS

- evolving

- komaristaya.ru

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

CHAPTER 1· THE EVOLVING AIR TRANSPORT INDUSTRY<br />

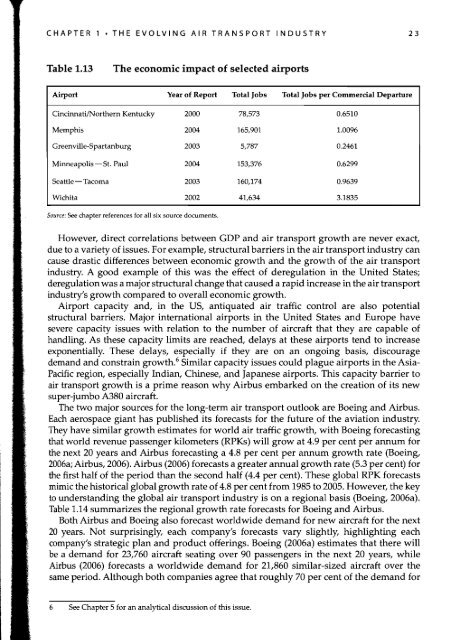

Table 1.13 <strong>The</strong> economic impact of selected airports<br />

<strong>Air</strong>port Year of Report Total Jobs Total Jobs per Commercial Departure<br />

CincinnatilNorthem Kentucky 2000 78,573 0.6510<br />

Memphis 2004 165,901 1.0096<br />

Greenville-Spartanburg 2003 5,787 0.2461<br />

Minneapolis-St. Paul 2004 153,376 0.6299<br />

Seattle - Tacoma 2003 160,174 0.9639<br />

Wichita 2002 41,634 3.1835<br />

Source: See chapter references for all six source documents.<br />

However, direct correlations between GDP and air transport growth are never exact,<br />

due to a variety of issues. For example, structural barriers in the air transport industry can<br />

cause drastic differences between economic growth and the growth of the air transport<br />

industry. A good example of this was the effect of deregulation in the United States;<br />

deregulation was a major structural change that caused a rapid increase in the air transport<br />

industry's growth compared to overall economic growth.<br />

<strong>Air</strong>port capacity and, in the US, antiquated air traffic control are also potential<br />

structural barriers. Major international airports in the United States and Europe have<br />

severe capacity issues with relation to the number of aircraft that they are capable of<br />

handling. As these capacity limits are reached, delays at these airports tend to increase<br />

exponentially. <strong>The</strong>se delays, especially if they are on an ongoing basis, discourage<br />

demand and constrain growth. 6 Similar capacity issues could plague airports in the Asia<br />

Pacific region, especially Indian, Chinese, and Japanese airports. This capacity barrier to<br />

air transport growth is a prime reason why <strong>Air</strong>bus embarked on the creation of its new<br />

super-jumbo A380 aircraft.<br />

<strong>The</strong> two major sources for the long-term air transport outlook are Boeing and <strong>Air</strong>bus.<br />

Each aerospace giant has published its forecasts for the future of the aviation industry.<br />

<strong>The</strong>y have similar growth estimates for world air traffic growth, with Boeing forecasting<br />

that world revenue passenger kilometers (RPKs) will grow at 4.9 per cent per annum for<br />

the next 20 years and <strong>Air</strong>bus forecasting a 4.8 per cent per annum growth rate (Boeing,<br />

2006a; <strong>Air</strong>bus, 2006). <strong>Air</strong>bus (2006) forecasts a greater annual growth rate (5.3 per cent) for<br />

the first half of the period than the second half (4.4 per cent). <strong>The</strong>se global RPK forecasts<br />

mimic the historical global growth rate of 4.8 per cent from 1985 to 2005. However, the key<br />

to understanding the global air transport industry is on a regional basis (Boeing, 2006a).<br />

Table 1.14 summarizes the regional growth rate forecasts for Boeing and <strong>Air</strong>bus.<br />

Both <strong>Air</strong>bus and Boeing also forecast worldwide demand for new aircraft for the next<br />

20 years. Not surprisingly, each company's forecasts vary slightly, highlighting each<br />

company's strategic plan and product offerings. Boeing (2006a) estimates that there will<br />

be a demand for 23,760 aircraft seating over 90 passengers in the next 20 years, while<br />

<strong>Air</strong>bus (2006) forecasts a worldwide demand for 21,860 similar-sized aircraft over the<br />

same period. Although both companies agree that roughly 70 per cent of the demand for<br />

6 See Chapter 5 for an analytical discussion of this issue.<br />

23