Reverse Logistics - Logistics Quarterly

Reverse Logistics - Logistics Quarterly

Reverse Logistics - Logistics Quarterly

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

RETURN ON<br />

ASSETS<br />

%<br />

net profit ( total )<br />

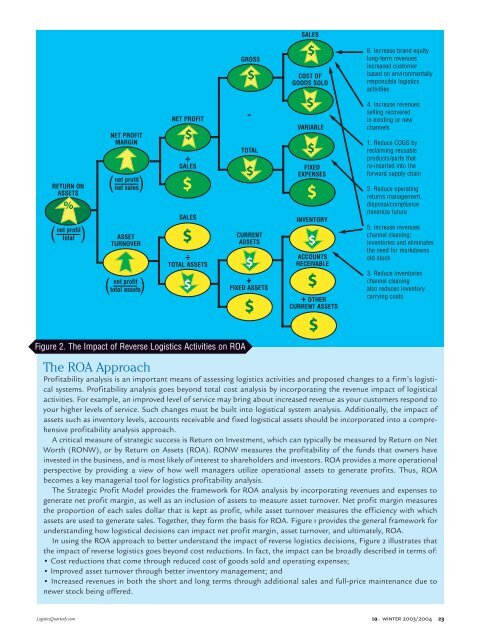

The ROA Approach<br />

Profitability analysis is an important means of assessing logistics activities and proposed changes to a firm’s logistical<br />

systems. Profitability analysis goes beyond total cost analysis by incorporating the revenue impact of logistical<br />

activities. For example, an improved level of service may bring about increased revenue as your customers respond to<br />

your higher levels of service. Such changes must be built into logistical system analysis. Additionally, the impact of<br />

assets such as inventory levels, accounts receivable and fixed logistical assets should be incorporated into a comprehensive<br />

profitability analysis approach.<br />

A critical measure of strategic success is Return on Investment, which can typically be measured by Return on Net<br />

Worth (RONW), or by Return on Assets (ROA). RONW measures the profitability of the funds that owners have<br />

invested in the business, and is most likely of interest to shareholders and investors. ROA provides a more operational<br />

perspective by providing a view of how well managers utilize operational assets to generate profits. Thus, ROA<br />

becomes a key managerial tool for logistics profitability analysis.<br />

The Strategic Profit Model provides the framework for ROA analysis by incorporating revenues and expenses to<br />

generate net profit margin, as well as an inclusion of assets to measure asset turnover. Net profit margin measures<br />

the proportion of each sales dollar that is kept as profit, while asset turnover measures the efficiency with which<br />

assets are used to generate sales. Together, they form the basis for ROA. Figure 1 provides the general framework for<br />

understanding how logistical decisions can impact net profit margin, asset turnover, and ultimately, ROA.<br />

In using the ROA approach to better understand the impact of reverse logistics decisions, Figure 2 illustrates that<br />

the impact of reverse logistics goes beyond cost reductions. In fact, the impact can be broadly described in terms of:<br />

• Cost reductions that come through reduced cost of goods sold and operating expenses;<br />

• Improved asset turnover through better inventory management; and<br />

• Increased revenues in both the short and long terms through additional sales and full-price maintenance due to<br />

newer stock being offered.<br />

<strong>Logistics</strong><strong>Quarterly</strong>.com<br />

NET PROFIT<br />

MARGIN<br />

net profit ( net sales)<br />

ASSET<br />

TURNOVER<br />

net profit ( total assets)<br />

NET PROFIT<br />

$<br />

÷<br />

SALES<br />

$<br />

SALES<br />

$<br />

÷<br />

TOTAL ASSETS<br />

Figure 2. The Impact of <strong>Reverse</strong> <strong>Logistics</strong> Activities on ROA<br />

$<br />

GROSS<br />

$<br />

-<br />

TOTAL<br />

$<br />

CURRENT<br />

ASSETS<br />

$<br />

+<br />

FIXED ASSETS<br />

$<br />

SALES<br />

$<br />

COST OF<br />

GOODS SOLD<br />

$<br />

VARIABLE<br />

$<br />

FIXED<br />

EXPENSES<br />

$<br />

INVENTORY<br />

$<br />

ACCOUNTS<br />

RECEIVABLE<br />

$<br />

+ OTHER<br />

CURRENT ASSETS<br />

$<br />

6. Increase brand equity<br />

long-term revenues<br />

increased customer<br />

based on environmentally<br />

responsible logistics<br />

activities<br />

4. Increase revenues<br />

selling recovered<br />

in existing or new<br />

channels<br />

1. Reduce COGS by<br />

reclaiming reusable<br />

products/parts that<br />

re-inserted into the<br />

forward supply chain<br />

2. Reduce operating<br />

returns management,<br />

disposal/compliance<br />

minimize future<br />

5. Increase revenues<br />

channel cleaning;<br />

inventories and eliminates<br />

the need for markdowns<br />

old stock<br />

3. Reduce inventories<br />

channel cleaning<br />

also reduces inventory<br />

carrying costs<br />

LQ winter 2003/2004<br />

23