WEALTH, DISPOSABLE INCOME AND CONSUMPTION - Economics

WEALTH, DISPOSABLE INCOME AND CONSUMPTION - Economics

WEALTH, DISPOSABLE INCOME AND CONSUMPTION - Economics

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

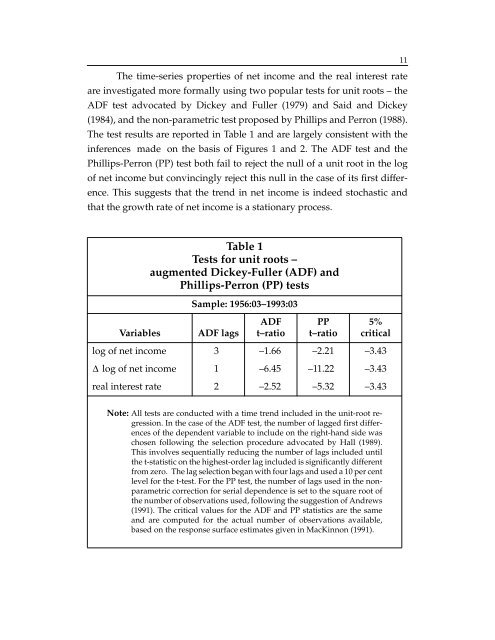

The time-series properties of net income and the real interest rate<br />

are investigated more formally using two popular tests for unit roots – the<br />

ADF test advocated by Dickey and Fuller (1979) and Said and Dickey<br />

(1984), and the non-parametric test proposed by Phillips and Perron (1988).<br />

The test results are reported in Table 1 and are largely consistent with the<br />

inferences made on the basis of Figures 1 and 2. The ADF test and the<br />

Phillips-Perron (PP) test both fail to reject the null of a unit root in the log<br />

of net income but convincingly reject this null in the case of its first difference.<br />

This suggests that the trend in net income is indeed stochastic and<br />

that the growth rate of net income is a stationary process.<br />

Table 1<br />

Tests for unit roots –<br />

augmented Dickey-Fuller (ADF) and<br />

Phillips-Perron (PP) tests<br />

Variables ADF lags<br />

Sample: 1956:03–1993:03<br />

ADF<br />

t–ratio<br />

PP<br />

t–ratio<br />

5%<br />

critical<br />

log of net income 3 –1.66 –2.21 –3.43<br />

Δ<br />

log of net income 1 –6.45 –11.22 –3.43<br />

real interest rate 2 –2.52 –5.32 –3.43<br />

Note: All tests are conducted with a time trend included in the unit-root regression.<br />

In the case of the ADF test, the number of lagged first differences<br />

of the dependent variable to include on the right-hand side was<br />

chosen following the selection procedure advocated by Hall (1989).<br />

This involves sequentially reducing the number of lags included until<br />

the t-statistic on the highest-order lag included is significantly different<br />

from zero. The lag selection began with four lags and used a 10 per cent<br />

level for the t-test. For the PP test, the number of lags used in the nonparametric<br />

correction for serial dependence is set to the square root of<br />

the number of observations used, following the suggestion of Andrews<br />

(1991). The critical values for the ADF and PP statistics are the same<br />

and are computed for the actual number of observations available,<br />

based on the response surface estimates given in MacKinnon (1991).<br />

11